What is a Balance Sheet? How to Prepare the Latest Balance Sheet for 2026

The balance sheet is one of the most important financial statements, reflecting a company’s entire financial position in terms of assets and capital sources at a specific point in time. Although familiar to accountants, many business owners and managers still find it challenging to read, analyze, or prepare this report themselves. In the article below, let’s join 1Office to explore what a balance sheet is, how to prepare and read it in detail, and get updated on new points applicable from 2026.

Mục lục

- 1. Overview of the Balance Sheet

- 2. What does a balance sheet consist of?

- 4. Steps to prepare a balance sheet according to Circular 200

- 5. Latest Balance Sheet Templates

- 6. How to Read a Balance Sheet & Analysis Guide

- 7. Example of how to prepare a balance sheet

- 8. Major changes to the balance sheet under Circular 99/2025/TT-BTC from 2026

- 9. Frequently Asked Questions

- Conclusion

1. Overview of the Balance Sheet

Below is an overview to help you understand the nature, role, and significance of the balance sheet within a company’s financial reporting system.

1.1. What is a Balance Sheet?

According to the definition in Circular 200/2014/TT-BTC, the balance sheet is a comprehensive financial report that shows all the assets a company owns and the capital sources that formed those assets at a specific point in time. Simply put, the balance sheet indicates what a company owns, how much it owes, and the amount of capital invested by shareholders at a given moment.

Through this statement, a company can clearly see:

- The scale and structure of its existing assets

- The structure of its capital sources (owner’s equity and liabilities)

Based on the figures in the Balance Sheet, managers and stakeholders can assess the company’s overall financial situation, capital safety level, and financial autonomy.

The balance sheet is one of the three core financial statements of a business, alongside the Income Statement and the Cash Flow Statement. It serves as a crucial basis for tracking changes in assets and capital sources over time, and also provides a foundation for analyzing and preparing the other financial statements.

A balance sheet reflects the assets a company has and the capital sources that formed those assets at a specific point in time

1.2. Significance for the Business

The balance sheet plays a key role in reflecting and assessing a company’s financial health. Specifically, this report offers several practical values:

- Reflects the overall financial picture: Through the balance sheet, a company can get a comprehensive view of its short-term & long-term solvency, liquidity level, and financial stability at any given time.

- Tracks changes in assets and capital sources: Comparing balance sheets from different periods helps a company clearly identify fluctuations in assets, capital structure, and financial trends over time.

- Provides a basis for business decisions: Data from the balance sheet, combined with other financial reports, helps management make decisions such as expanding or scaling back operations, investing, raising capital, or allocating funds.

- Meets legal requirements: This is a mandatory report in the set of financial statements required by the Accounting Law, helping to ensure compliance, transparency, and legality in the company’s operations.

- Provides information for stakeholders: Investors, creditors, and partners rely on the balance sheet to assess the company’s financial capacity, risk level, and ability to repay capital before making decisions to cooperate, invest, or lend.

1.3. The Balance Sheet in English

In English, the balance sheet is called the Balance Sheet, also known as the Statement of Financial Position. This is a comprehensive financial report that reflects a company’s financial picture at a specific point in time through three core elements: assets, liabilities, and owner’s equity.

- Balance Sheet: The most common and widely used term.

- Statement of Financial Position: An alternative term, often found in international accounting standards.

When studying or working with financial statements in English, businesses will often encounter the following basic terms:

| English | Vietnamese |

| Assets | Assets |

| Liabilities | Liabilities |

| Owners’ Equity | Owners’ Equity |

| Fixed Assets | Fixed Assets |

The English term for a balance sheet is Balance Sheet

2. What does a balance sheet consist of?

Below is the structure and main categories of items that make up a balance sheet according to current regulations:

2.1. Assets Section

Assets on the balance sheet reflect all the resources that the business holds and controls, which are capable of bringing future economic benefits. Asset items are arranged in order of liquidity, meaning how easily they can be converted into cash.

Based on this convertibility, assets are divided into current assets and non-current assets.

(1) Current assets: These are assets that can be recovered, sold, or used within 12 months or within a normal business operating cycle. This group includes:

- Cash and cash equivalents: These are the most liquid assets, including cash on hand, non-term bank deposits, cash in transit, and cash equivalents.

- Short-term receivables: Includes accounts receivable from customers, prepayments to suppliers, internal receivables, receivables based on construction contract progress, short-term loans, and other receivables.

- Short-term financial investments: These are investments with a recovery period of no more than 12 months, such as trading securities, held-to-maturity investments, or other short-term financial investments.

- Inventories: Includes raw materials, work-in-progress, finished goods, and merchandise for production and business activities.

- Other current assets: These are items with a recovery or usage period of no more than 12 months, such as short-term prepaid expenses, deductible VAT, taxes receivable, and other current assets.

(2) Non-current assets: These are assets that are difficult to convert into cash and are used in business operations for more than 12 months, including:

- Long-term receivables: These are items with a recovery period of more than 12 months, such as long-term customer receivables, internal receivables, long-term loans, and business capital in subsidiary units.

- Fixed assets: Includes tangible fixed assets (factories, machinery, etc.), intangible fixed assets, and finance lease fixed assets at the reporting date.

- Long-term financial investments: Includes investments in subsidiaries, associates, joint ventures, or capital contributions to other entities.

- Investment properties: Reflects the remaining value of properties held for rental purposes or for capital appreciation.

- Long-term assets in progress: Includes production, business, and basic construction costs that are in progress.

- Other non-current assets: Includes long-term prepaid expenses, deferred tax assets, and other non-current assets with a recovery period of more than 12 months.

2.2. Equity and Liabilities Section

The equity and liabilities section on the Balance Sheet reflects the sources that form all of the company’s assets, comprising two main groups: liabilities and owner’s equity.

(1) <a href="https://1office.vn/no-phai-tra" target="_

(1) General presentation principles

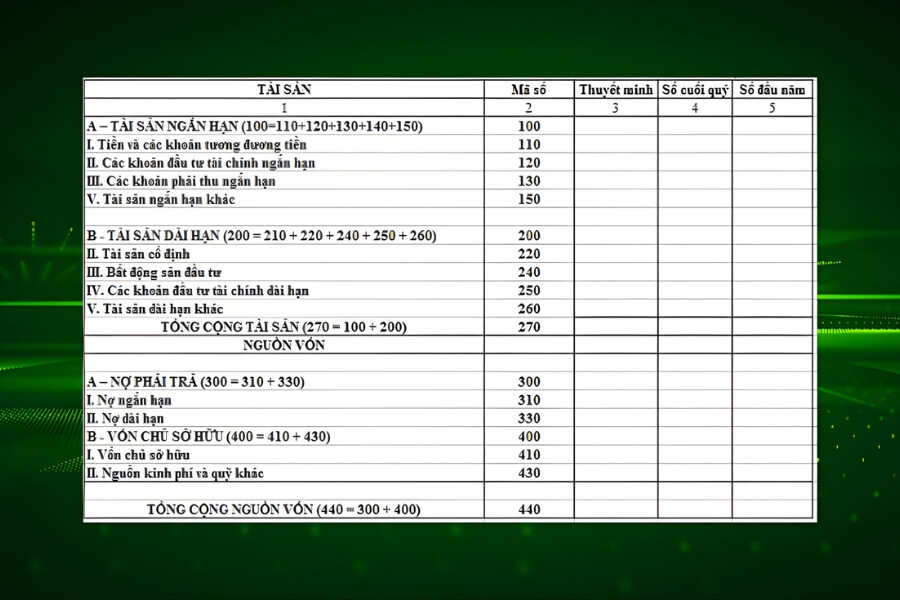

- Do not classify items as current and non-current.

- Do not present provisions on the balance sheet.

(2) Specific items with special preparation methods to note: In this case, some items are identified and presented using a different method compared to a going concern, including:

- Code 121: Trading securities

- Code 140: Inventories

(3) Presentation of remaining items: For other items, the enterprise combines the content and figures of the corresponding current and non-current items, instead of presenting them separately as a going concern would.

Principles of preparing a balance sheet

4. Steps to prepare a balance sheet according to Circular 200

Below are the steps to prepare a balance sheet according to Circular 200, helping businesses compile data accurately and ensure the report is always balanced and clear:

Step 1: Preparations before creating the balance sheet

Here are the tasks to be completed before preparing the balance sheet to ensure accurate and consistent data:

- Reconcile opening balances: Check the opening balances of all accounts to ensure they fully match the figures on the previous period’s Balance Sheet.

- Review transactions incurred during the period: Review all journal entries recorded up to the reporting date; reconcile account balances with relevant parties such as Tax authorities, Insurance, Customers, suppliers, etc.

- Check year-end allocations and closing entries: Review allocation and closing entries; ensure that accounts of type 5, 6, 7, 8, and 9 have no balance at the reporting date. Proceed to close the accounting books.

- Check detailed ledgers and account classification: Reconcile detailed ledgers by each account and object; classify assets and liabilities into current and non-current categories as regulated.

- Prepare the trial balance: Prepare the trial balance for the period; check and reconcile Debit – Credit balances to ensure they match the figures in each accounting account.

Step 2: Determine the reporting date for the balance sheet

The balance sheet reflects the financial position of a business at a specific point in time, not over a period of activity. Therefore, the report’s header must always clearly state the reporting date.

In practice, the balance sheet is usually prepared at the end of the fiscal year. However, depending on management requirements or reporting obligations, businesses can also prepare quarterly or semi-annual reports for analysis and decision-making purposes.

Step 3: Consolidate and classify the company’s assets

In this step, the business compiles all accounts in the asset group, including current and non-current assets, then calculates the total value of each group and the total assets at the reporting date.

Asset items are arranged in descending order of liquidity, from cash and cash equivalents to assets with lower convertibility, in compliance with the structure and criteria specified in Article 112 – Circular 200/2014/TT-BTC.

Specifically:

- Current assets reflect resources that can be recovered, used, or converted into cash within 12 months or one business cycle.

- Non-current assets include assets used for production and business activities for more than 12 months, such as fixed assets, long-term investments, and long-term receivables.

|

Item |

Code | Formula | Ending Balance (Debit) | Ending Balance (Credit) | ||||||

| A. CURRENT ASSETS | 100 | |||||||||

| I. Cash and cash equivalents | 110 | 110 = 111 + 112 | ||||||||

| 1. Cash | 111 | 111, 112, 113 | ||||||||

| 2. Cash equivalents | 112 | 1281, 1288 (investments < 3 months) | ||||||||

| II. Short-term financial investments | 120 | 120 = 121 + 122 + 123 | ||||||||

| 1. Trading securities | 121 | 121 | ||||||||

| 2. Provision for diminution in value of trading securities | 122 | 2291 | ||||||||

| 3. Held-to-maturity investments | 123 | <span style="font-weight:

Step 4: Compile the business’s liabilities and owner’s equityIn this step, the business needs to perform the following tasks:

Next, the business calculates the total capital on the balance sheet using the formula:

Once all the above steps are completed, the company’s balance sheet will be fully and consistently prepared. Note: If Assets ≠ Liabilities + Owner’s Equity, the company needs to re-check the figures and related entries to ensure accuracy.

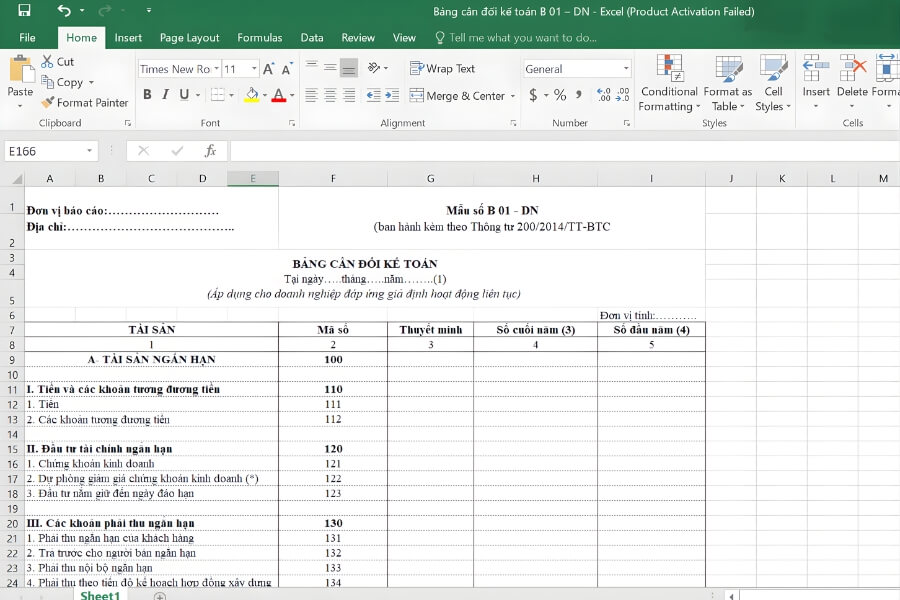

Steps to prepare a balance sheet according to Circular 200 5. Latest Balance Sheet TemplatesBelow are the latest balance sheet templates according to current regulations, with application guidelines suitable for businesses: 5.1. Balance Sheet Template according to Circular 200For businesses that meet the going concern assumption (i.e., the business is operating stably with no signs of interruption or cessation in the near future), the Balance Sheet must be prepared according to Form B 01 – DN, issued with Circular 200/2014/TT-BTC. >>>> Download Balance Sheet Form B 01 – DN HERE

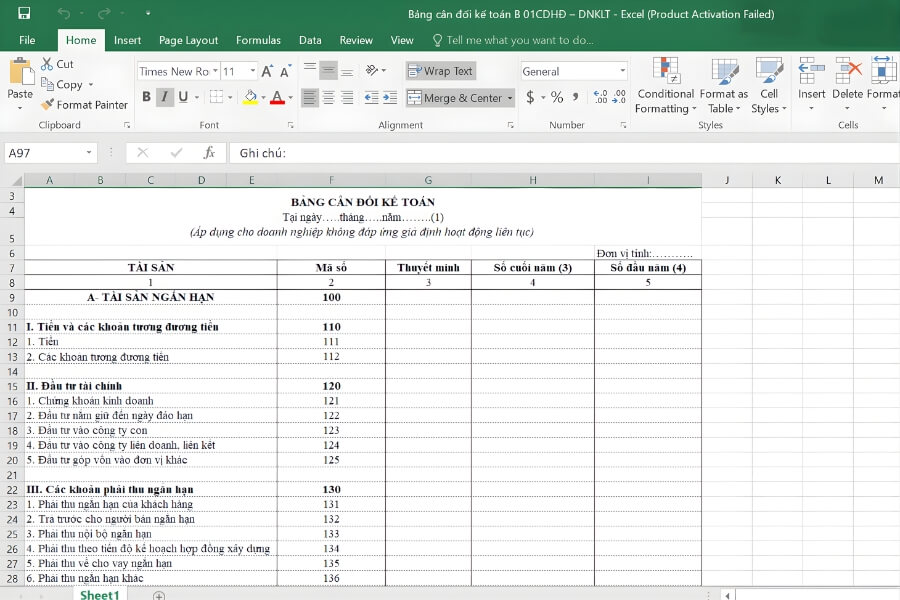

Balance sheet template according to Circular 200 5.2. Balance Sheet Template according to Circular 133If a business does not meet the going concern assumption (i.e., it is undergoing dissolution, bankruptcy, downsizing, or shows signs of not continuing operations in the future), the Balance Sheet must be prepared according to Form B 01/CDHĐ – DNKLT, also issued with Circular 200/2014/TT-BTC. >>>> Download Balance Sheet Form B 01/CDHĐ – DNKLT HERE

Balance sheet template according to Circular 133 6. How to Read a Balance Sheet & Analysis GuideHere’s how to read and analyze a balance sheet to assess asset size, capital structure, and the financial health of a business: Step 1: Determine the Business Context and Basic InformationBefore diving into the numbers on the balance sheet, it’s essential to understand the overall picture of the business, including its industry, scale, development strategy, and operational goals. This information provides a crucial foundation for conducting financial analysis in the proper context, avoiding one-sided or inaccurate assessments. Step 2: Understand Balance Sheet Analysis MethodsWhen analyzing a balance sheet, you can apply one of the following two methods:

Step 3: Read the Overview FiguresIn this step, the goal is to help you visualize the scale of the business and how assets and capital are allocated on the balance sheet. The key indicators to focus on include:

Step 4: Analyze Each Group of Indicators in DetailAfter grasping the overall picture, you need to delve into specific indicators to clearly understand the company’s financial quality, including:

|