E-invoice Cancellation Record Template Compliant with Circular 78

During the use of invoices, errors or no longer needing them are unavoidable. To ensure legality and avoid tax-related risks, creating an invoice cancellation record is necessary. The article below will provide the latest e-invoice cancellation record template according to Circular 78/2021/TT-BTC and detailed instructions on how to create the record correctly.

Mục lục

- I. What is invoice cancellation?

- II. What is an invoice cancellation record?

- III. In which cases is an invoice cancellation record required?

- IV. The latest invoice cancellation record templates

- V. Important notes when creating an invoice cancellation record

- VI. How to create an invoice cancellation record in 7 standard steps

- VII. FAQ about invoice cancellation records

- 1. Are there penalties for mistakenly canceling an e-invoice?

- 2. Differentiating between canceling an invoice and destroying an invoice

- 3. Can an invoice that has already been declared for tax purposes be canceled with a record?

- 4. How to notify the tax authority about an invoice cancellation?

- 5. What is the deadline for creating an invoice cancellation record?

- 6. Is it necessary to establish a council for every invoice cancellation case?

- 7. Can an invoice cancellation record be created as an electronic file?

- VIII. Conclusion

I. What is invoice cancellation?

Invoice cancellation is the official process of revoking the legal validity of an invoice that has been issued but not yet used, not yet declared for tax, or has been found to have uncorrectable errors, ensuring that the invoice is no longer legally valid.

II. What is an invoice cancellation record?

An invoice cancellation record is a document that records the agreement between parties to cancel an invoice. It includes complete information such as the invoice number, issue date, reason for cancellation, and confirmation from the relevant parties, ensuring compliance with legal regulations on e-invoices.

III. In which cases is an invoice cancellation record required?

An invoice cancellation record is a document created when two parties (the buyer and the seller) agree to and accept the cancellation of an issued invoice that contains errors or is no longer valid. This type of document serves as a legal record, noting the reason and agreement for the cancellation, to avoid future disputes or tax risks.

An invoice cancellation record is created in the following cases:

- Unused paper invoices: The business no longer needs them and decides to cancel unissued invoices (Clause 3, Article 7, Decree 123/2020/ND-CP)

- Paper or electronic invoices that have been issued but contain errors and have not been declared for tax: Incorrect name, address, tax code, amount, tax rate, or tax content (Clause 1, Article 19, Decree 123/2020/ND-CP)

- Invoices issued by mistake or duplicated/redundant invoices: In this case, the business needs to create a record to eliminate the invalid invoices.

An e-invoice cancellation record is created in the following cases:

- E-invoices that have been issued but not yet sent to the buyer: When an error is discovered before sending, the seller must cancel that invoice and issue a new one (Clause 1, Article 19, Decree 123/2020/ND-CP).

- E-invoices that have been sent but not yet declared for tax: If an error is discovered after sending but before tax declaration, the business needs to create a mutual agreement record to cancel the invoice. Only then can the seller issue a new invoice.

- E-invoices that are no longer valid due to expiration or system shutdown: In this case, the seller needs to coordinate with the tax authority or the e-invoice provider to cancel the invoice according to regulations.

IV. The latest invoice cancellation record templates

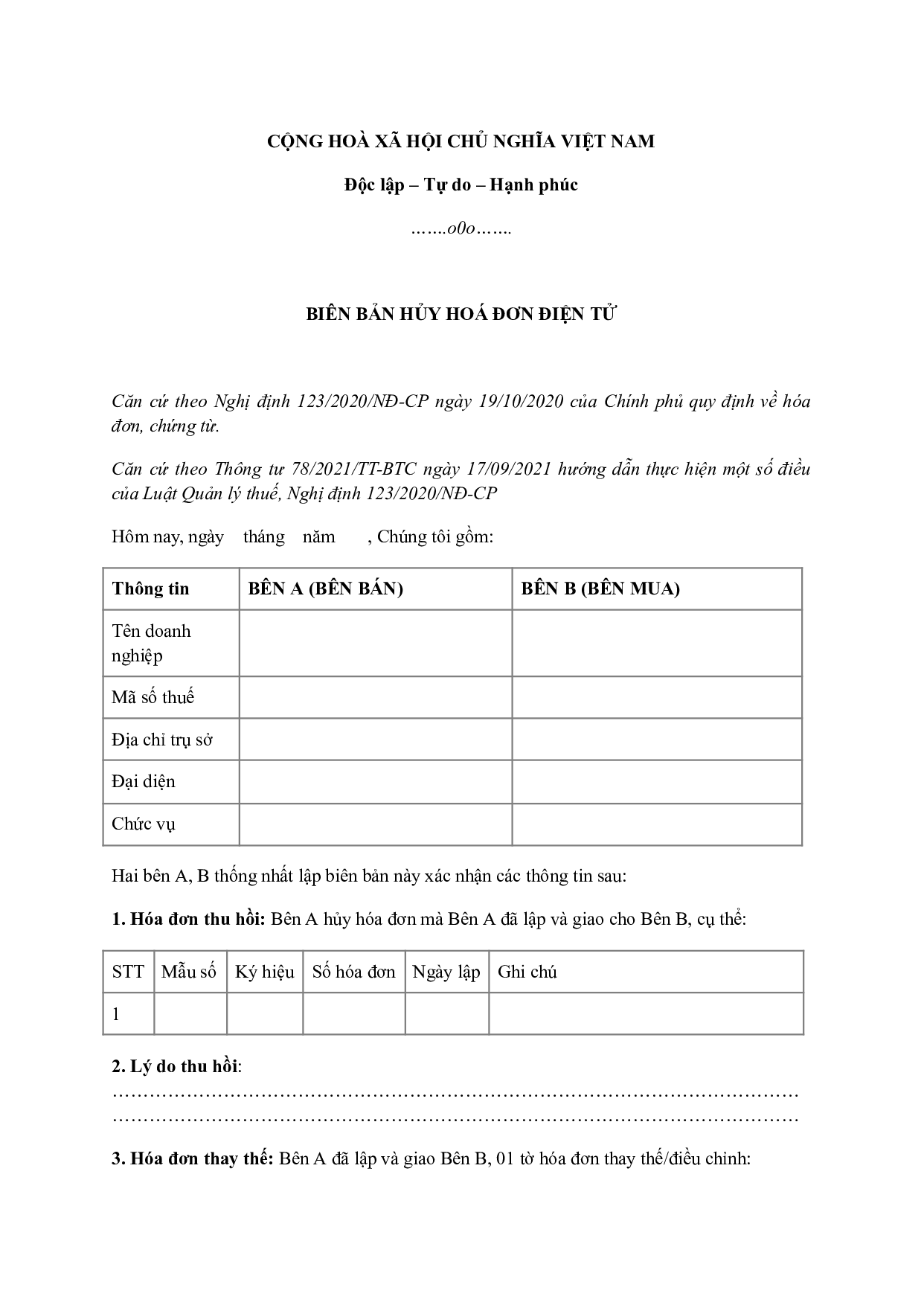

1. Invoice cancellation record template according to Circular 78

Based on Decree 123/2020/ND-CP and Circular 78/2021/TT-BTC, the invoice cancellation record must include the following basic information:

- Name, tax code, and address of both parties.

- Information about the invoice to be canceled (invoice number, series, issue date).

- Reason for invoice cancellation.

- Signature of the legal representative or authorized person.

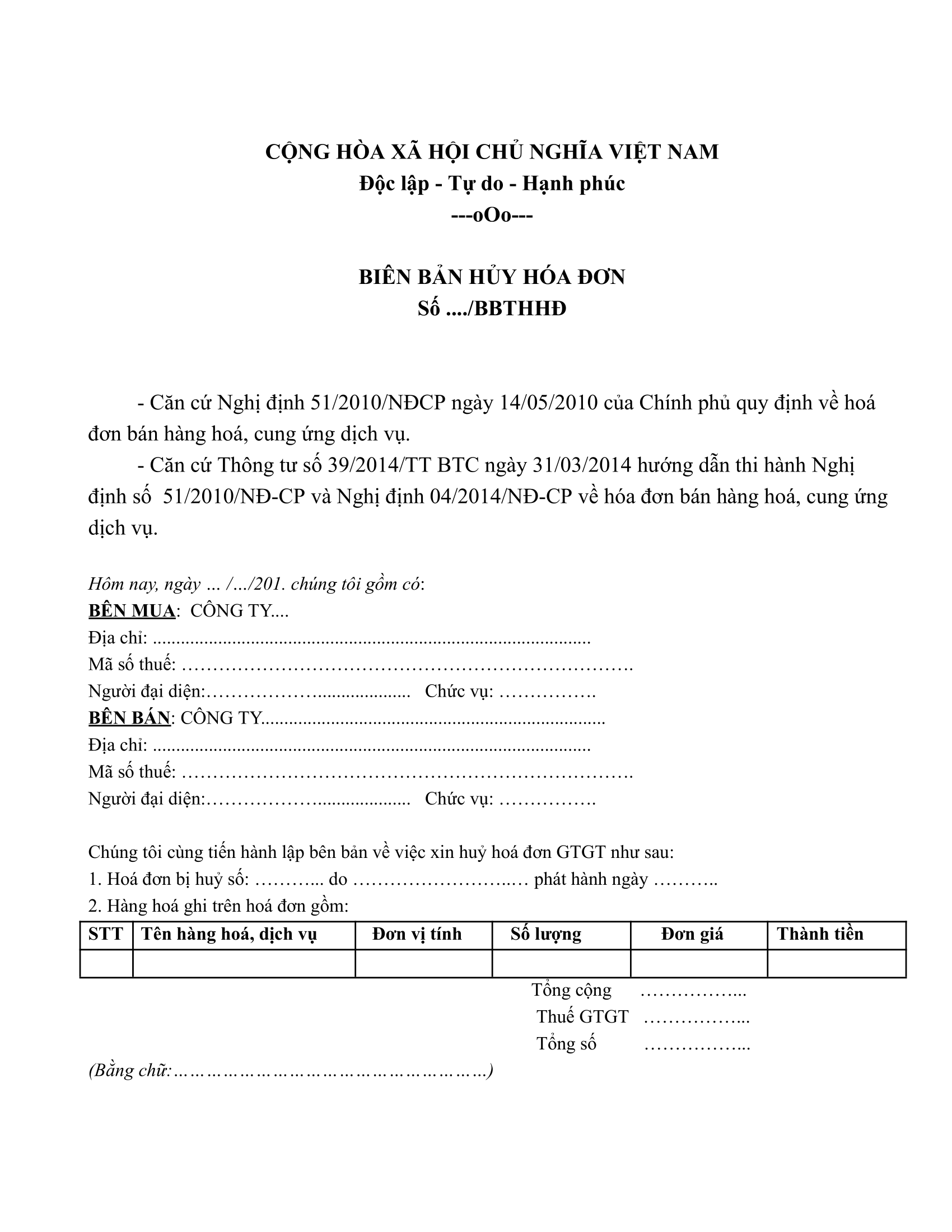

2. VAT invoice cancellation record template

A VAT invoice cancellation record is a document created when a value-added tax (VAT) invoice that has been issued needs to be canceled because it is no longer valid or contains errors that need to be addressed. This document records the consensus between the relevant parties (usually the seller and the buyer) to ensure legality, transparency, and compliance with legal regulations on invoices.

The VAT invoice cancellation record template also requires the following key information:

- Information of the relevant parties: address, tax code, representative, etc.

- Information about the invoice to be canceled: invoice number, reason for cancellation, etc.

- Content of the agreement between the parties

- Confirmation signatures

V. Important notes when creating an invoice cancellation record

Accurate and complete information

- The record must be created with detailed and correct information about the invoice number, issue date, and reason for cancellation to avoid errors during tax declaration.

Ensure timely processing

- The business must cancel the invoice and create the record within the specified time frame, avoiding delays that could affect tax declaration.

- For incorrect or duplicate invoices, they must be processed immediately upon discovery to protect the rights of the business and related parties.

Signatures and seals

- The record must have the signature of the invoice issuer’s representative. In some cases, the invoice cancellation record requires the agreement and confirmatory signatures of both the buyer and the seller.

>>> See more: What you need to know about digital signatures and e-invoices

Compliance with legal regulations

- Invoice cancellation must comply with current regulations such as Decree 123/2020/ND-CP and Circular 78/2021/TT-BTC, as well as specific guidance from tax authorities.

Storage process

- The business must store the invoice cancellation record along with related documents (cancelled invoice, accompanying files) systematically for easy inspection and comparison when needed.

Notify tax authorities (if necessary)

- In some cases, especially for unused paper invoices, the business will need to notify and follow the correct invoice cancellation procedure as required by the tax authorities.

VI. How to create an invoice cancellation record in 7 standard steps

Invoice cancellation must be carried out in accordance with legal regulations to ensure validity and avoid potential legal risks. Below is the standard invoice cancellation process, based on Decree 123/2023/ND-CP and Circular 78/2021/TT-BTC.

Step 1: Accurately identify the case requiring invoice cancellation

- Paper invoices: Incorrect information, printing errors, invoices no longer valid for use, etc.

- E-invoices: Sent with incorrect information, not yet sent to the buyer, or not yet declared for tax, etc.

Step 2: Agreement between related parties

- If the invoice has already been sent to the buyer, cancellation requires the agreement of both the seller and the buyer.

- Create an invoice cancellation record, clearly stating the reason, invoice details, and commitments of the parties.

Step 3: Create the invoice cancellation record

- Ensure the record is created with accurate and complete information and confirmation from all related parties, including: reason, commitments, representative signatures of the parties, etc.

Step 4: Cancel the invoice as per regulations

- Paper invoices: Cancel directly by destroying the invalid invoice, creating a paper invoice cancellation record, and storing it according to the correct procedure.

- E-invoices: Cancel the invoice on the e-invoice software system, ensuring a log (history) of the cancellation process is recorded for storage and comparison.

Step 5: Notify the tax authorities (if necessary)

- For unused paper invoices, the business must submit an invoice cancellation notice to the tax authorities along with the cancellation record. For e-invoices, notification is not required, but the business must still store all related documents for inspection when needed.

Step 6: Issue a replacement invoice

- If the transaction still proceeds, the seller must issue a new invoice to replace the cancelled one. The business must ensure the new invoice is created according to regulations and fully declared for tax.

Step 7: Store the records

- The business must store the invoice cancellation record, cancellation notice (if any), and related documents in its accounting records for at least 10 years.

The above process ensures that the business cancels invoices in compliance with the law and avoids risks in current accounting and tax activities.

VII. FAQ about invoice cancellation records

1. Are there penalties for mistakenly canceling an e-invoice?

If an e-invoice is mistakenly canceled improperly, businesses and individuals may face administrative penalties. According to Article 26 of Decree 125/2020/ND-CP, the act of losing, burning, or damaging unissued invoices or invoices that have been issued but not yet delivered to the buyer can result in a fine from 4,000,000 to 8,000,000 VND.

If the mistaken cancellation affects tax declarations, the business may face additional penalties for incorrect or incomplete declarations under Article 16 of Decree 125/2020/ND-CP.

2. Differentiating between canceling an invoice and destroying an invoice

- Canceling an invoice: Based on Article 7 of Decree 123/2020/ND-CP, canceling an invoice (electronic or paper) renders it invalid for use. Invoice cancellation is typically applied to invoices with incorrect information or those that are no longer in use, and it is accompanied by an invoice cancellation record.

- Destroying an invoice: According to Article 11 of Circular 39/2014/TT-BTC, destroying an invoice involves disposing of unused or incorrect paper invoices through physical destruction (tearing, burning, shredding, etc.). This action must ensure the invoice cannot be restored for reuse.

3. Can an invoice that has already been declared for tax purposes be canceled with a record?

An invoice that has been declared for tax cannot be canceled; it can only be adjusted or replaced. According to Article 19 of Circular 78/2021/TT-BTC, an e-invoice with incorrect declared information must be adjusted with a new invoice or replaced with a replacement invoice; cancellation is not applicable.

To notify the tax authority of an invoice cancellation, a business needs to follow these steps:

- Create an invoice cancellation record (applicable for unused or incorrect paper invoices).

- Submit the invoice cancellation notice (Form TB03/AC) to the tax authority through the electronic tax declaration system (Based on Article 29, Decree 123/2020/ND-CP).

5. What is the deadline for creating an invoice cancellation record?

Based on Articles 7 and 11 of Decree 123/2020/ND-CP, the deadline for creating an invoice cancellation record depends on the type of invoice:

- For unused paper invoices: The business must cancel them within 30 days from the date of notifying the tax authority.

- For e-invoices: A record must be created immediately upon discovering the error, and the cancellation must be carried out according to the procedure.

6. Is it necessary to establish a council for every invoice cancellation case?

Based on Article 29, Decree 123/2020/ND-CP, it is not necessary to establish a council for every invoice cancellation case.

- For unused invoices that need to be canceled in large quantities, a council must be established to supervise the destruction.

- For e-invoices: A council is not required; the process is carried out according to the procedures of the software and the invoice issuing entity.

7. Can an invoice cancellation record be created as an electronic file?

An invoice cancellation record can be created as an electronic file for convenience in transactions and storage, but the business must ensure the record has the valid electronic signatures of all relevant parties. This complies with the regulations on electronic document management in Decree 123/2020/ND-CP and Decree 119/2018/ND-CP.

VIII. Conclusion

Creating an invoice cancellation record in accordance with regulations not only helps businesses comply with the law but also avoids tax and financial risks. We hope the sample record and detailed instructions in this article have provided you with useful information. If you need further assistance with e-invoice management or related issues, do not hesitate to contact the expert team at 1Office for timely advice.