How does the historical cost principle work? Applying the historical cost principle in accounting

The cost principle is one of the preferred principles for accountants when determining costs and preparing financial statements for a business. In this article, we will explore the cost principle.

Mục lục

I. General Overview of the Cost Principle

1. What is the cost principle?

In accounting, the original cost of an asset is its purchase price or initial monetary value.

In practice, a business’s transactions tend to be recorded at their original cost. This concept, combined with the cost principle, emphasizes that: assets, equity investments, and liabilities must be recorded at their respective acquisition costs.

Retrieving the original cost of an asset is relatively easy, provided that records have been kept. Transaction, sales, or purchase documents are used to determine the original cost of an asset. However, it is important to know that the original cost may not necessarily reflect the asset’s true fair value.

The value of an asset is likely to deviate from its original purchase price over time. An example is the acquisition of an office block worth $5,000,000. The acquisition was made 15 years ago; however, in the current market, the building is worth over $12,000,000.

2. Why is the cost principle important?

This cost principle is one of the four basic financial reporting principles used by all accounting professionals and businesses. It stipulates that all goods and services a business purchases must be recorded at their original cost, not their fair market value.

The original cost is very important for those who read a company’s balance sheet or analyze its books (records). The original cost is:

- Reliable: The process of showing the original cost on a company’s balance sheet is always the same. It does not change; it is reliable. This is important because anyone looking at the balance sheet can get a reliable picture of the company’s assets.

- Comparable: It is easy to compare the original cost of one asset with another using the cost principle. This is important when making decisions about assets.

- Verifiable: It is also easy to verify the original cost because there are records that substantiate what is shown on the balance sheet.

See more: What is corporate financial management? Principles of effective corporate financial management

II. How does the cost principle work?

1. How is the cost principle used in accounting?

According to VAS standards, the cost principle is stipulated as follows:

A company’s assets must be recorded at their original cost.

The original cost of an asset will be calculated based on the amount of cash or cash equivalents paid, payable, or the amount recognized by accounting at the time of purchase according to the payment voucher.

The original cost of an asset cannot be changed unless otherwise specified in a specific accounting standard.

The cost principle stipulates that: For transactions involving the purchase of fixed assets, tools, and raw materials recorded on the balance sheet, the value recorded on the balance sheet is the original cost, not the price at the time the sale or purchase occurred.

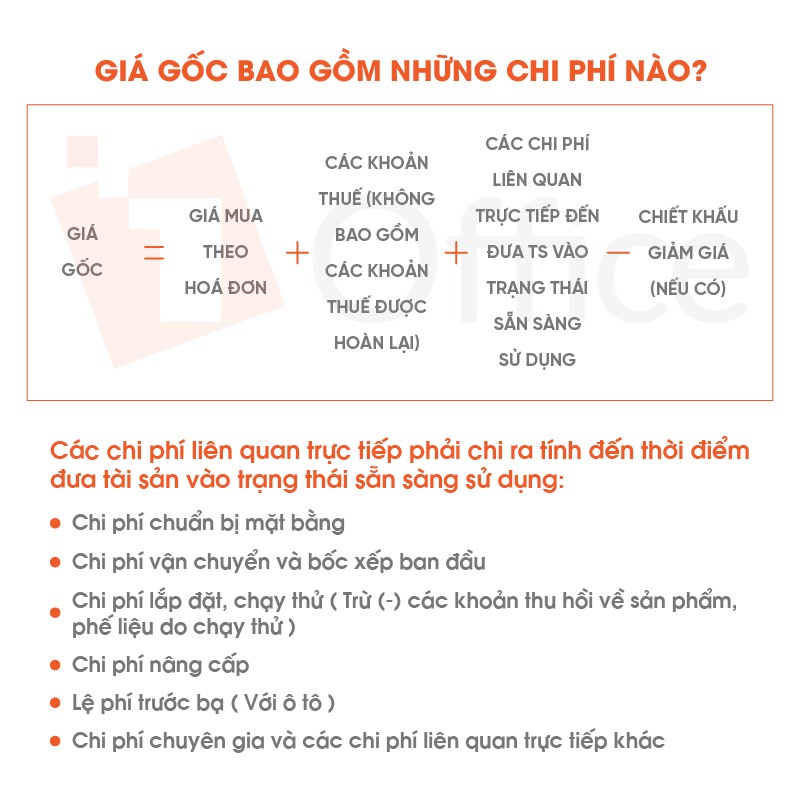

2. What costs are included in the original cost?

3. Common challenges with the cost principle

The cost principle is widely used, but it is not accurate in all cases. Some challenges that accountants face when using it include:

- It does not provide an indication of the current value of assets;

- It does not account for inflation or deflation; and

- It is misleading as an indicator of a company’s ability to continue operating at a specific level because its assets are undervalued.

Like all accounting principles, the original cost has its place on the balance sheet and is useful for the finance team when used correctly. However, it also has its own limitations and is not always useful for a company’s balance sheet. Although it is not a controversial principle by any means, there is currently a debate about the benefits of using fair market value more often than the current value used in place of historical cost.

| Learn more: A company’s core values and 5 steps to define core values for your organization |

III. Example of the Cost Principle

Julius owns an investment company that has acquired various properties across the southern United States. Assuming that inflation across the region has doubled in recent years, the real estate investments are not worth the amount Julius paid to acquire them.

The cost principle does not account for adjustments due to currency fluctuations; therefore, the financial statements will still record the value of the assets at their purchase price.

IV. Frequently Asked Questions about the Cost Principle

What is the difference between historical cost and fair market value?

Historical cost is the cash or cash equivalent value of an asset at the time of purchase. Fair market value is the current value of that asset.

For example: Imagine if someone bought a plot of land 10 years ago for $10,000, and that land is now worth $20,000. The historical cost is $10,000, and the fair market value is $20,000.

How is historical cost calculated?

Historical cost is typically calculated as the cash or cash equivalent cost at the time of purchase. This includes the purchase price and any additional costs incurred to bring the asset to its proper location and prepare it for use.

Through the article above, we have provided readers with the most general information about the Cost Principle. If you have any questions that need answering, please contact us for a free consultation.

For more detailed information, please see:

Hotline: 083 483 8888

Fanpage: https://www.facebook.com/1officevn/

Youtube: https://www.youtube.com/channel/UCeTIRNqxaTwk0_kcTw6SxmA