What is a Red Invoice? How to Issue Red VAT Invoices Correctly

Red invoice is a very familiar concept in sales and purchasing activities, but not everyone clearly understands the nature of this type of invoice and how to issue it correctly according to regulations. If you want to know what a red invoice is and what to note when issuing a VAT invoice, this article will help you quickly grasp the most important points.

Mục lục

- 1. Overview of Red Invoices

- 2. Regulations on Issuing Red VAT Invoices

- 4. Notes on issuing red invoices

- 5. Where to buy red invoices?

- 7. Differentiating red invoices from other invoices

- 8. Frequently Asked Questions about Red Invoices

- 1. What are the penalties for illegally printing and issuing red invoices?

- 2. Do red invoices need to be stamped? Is a hanging seal valid?

- 3. Who must issue red invoices?

- 4. Are red invoices still used in paper form?

- 5. What is the minimum amount for issuing a red invoice?

- 6. When is the time to issue a red invoice?

- 7. How to look up electronic red invoices?

- Conclusion

1. Overview of Red Invoices

Below is the basic information to help you understand what a red invoice is, when it is used, and its legal validity:

1.1. What is a red invoice?

Red invoices are also known by other names such as VAT invoices (value-added tax invoices). This is a type of document issued by the Ministry of Finance or self-printed and issued by businesses according to a template registered with the tax authority.

There are two main types of red invoices:

- Paper red invoices: These are pre-printed invoices on paper issued by the Ministry of Finance or self-printed by businesses after registering the template with the tax authority.

- Electronic red invoices: These are invoices created, processed, and transmitted electronically, stored and managed by information technology systems.

Red invoices are created and issued by the seller to the buyer when selling goods or providing services, to confirm the transaction value and serve as a basis for declaring, accounting for, and paying value-added tax as required by regulations.

From the 2022-2023 period, the printing and ordering of old-style paper invoices have been gradually phased out, and by 2026, they will almost no longer be applicable to businesses and organizations. Currently, businesses, business households, and individual entrepreneurs (especially those with large revenues) are required to use electronic invoices.

A red invoice is also called a VAT invoice (value-added tax invoice)

1.2. What are red invoices used for?

Red invoices (value-added tax invoices) are mandatory legal documents in the sale of goods and provision of services between businesses and organizations as required by law. Issuing invoices is not only the seller’s obligation but also plays a crucial role in the accounting, tax, and financial management of a business.

Specifically, red invoices are used to:

- Serve as a basis for declaring and calculating value-added tax: For the seller, the invoice is the basis for declaring output VAT and recognizing revenue. For the buyer, a valid invoice helps in declaring and deducting input VAT according to regulations.

- Account for costs and determine business results: Red invoices are important documents for businesses to record production and business costs, thereby determining reasonable and valid expenses when calculating corporate income tax.

- Settle payments and conduct financial audits: During inspections and audits by tax authorities or other state management agencies, red invoices serve as the initial basis for cross-referencing and verifying economic transactions.

- Prove the legality of sales transactions: The invoice acts as legal proof confirming that the sale of goods or provision of services has actually occurred between the parties.

- Serve as a basis for value-added tax refunds: When a business is eligible for a VAT refund, a valid red invoice is a mandatory basis for the tax authority to cross-reference and process the refund, while also helping the business protect its rights and reduce risks during explanations.

1.3. What is a red invoice in English?

In English, a red invoice is commonly called a Value Added Tax Invoice, abbreviated as VAT Invoice. This is a popular term and is officially used in accounting, tax documents, and international trade transactions.

Besides the common term above, in some cases, a red invoice can also be expressed using other English terms such as:

- Tax Invoice: Used in accounting and tax contexts

- VAT Bill: An informal term, rarely used in legal documents

- Sales Invoice (with VAT): A sales invoice that includes VAT

However, in accounting records, tax declarations, or transactions with foreign partners, Value Added Tax Invoice (VAT Invoice) remains the most accurate and widely accepted term.

A red invoice in English is a VAT Invoice

See more: Listing the benefits of electronic invoices for businesses

2. Regulations on Issuing Red VAT Invoices

Below are the important regulations regarding the subjects, timing, and principles for issuing red VAT invoices according to current laws:

2.1. Cases where issuing a red invoice is mandatory

Businesses are required to issue red invoices in the following cases:

| Mandatory red invoice issuance cases | Application details | Important notes |

| Selling goods, providing services | According to legal regulations, the seller of goods and services is required to create and issue a red invoice to the buyer |

For invoices valued over 200,000 VND, the buyer must pay an additional 10% VAT so the seller can fulfill their tax declaration obligations |

| Businesses eligible to use red invoices | Businesses that have registered for the VAT deduction method and have a legal lease agreement or business premises | Ordering or self-printing invoices must fully meet the conditions for invoice issuance and management as prescribed by law |

| Investment and asset procurement | Businesses paying VAT by the deduction method that have transactions involving investment, procurement, or receiving capital contributions in the form of fixed assets, machinery, equipment, tools, or instruments | The invoice serves as the basis for accounting records and for declaring and deducting VAT |

2.2. When can a red invoice be issued?

Pursuant to Article 9 of Decree 123/2020/ND-CP, the time of invoice issuance is determined for each specific type of transaction:

| When to issue a red invoice | Example |

| For the sale of goods: The invoice must be issued at the time of transferring ownership or right to use the goods to the buyer, regardless of whether payment has been received. |

The red invoice must be issued on March 10, at the time the machinery is handed over, not when the payment is received. |

| For the provision of services: The invoice is issued at the time the service provision is completed, even if payment has not yet been received. | Company C provides website design services to a client.

The red invoice must be issued on April 20, at the time the service is completed, regardless of the payment date. |

| In case of delivering goods or providing services in multiple installments or stages: The invoice must be issued at the time of delivery or handover of each corresponding stage or item. | Company D signs an interior construction contract consisting of 3 stages:

An invoice corresponding to the value of that stage must be issued upon each handover, not accumulated until the entire project is completed. |

Issuing red invoices (whether in electronic or paper form) is only applicable to entities that fully meet the conditions for tax registration, business type, and declaration obligations as prescribed by law. Below are the groups of entities authorized to issue red invoices:

Group 1 – Enterprises (organizations with legal entity status)

Enterprises can proactively create and issue red invoices when they meet the following conditions:

- Have a tax

Some important notes

- A single invoice is for a specific transaction only and cannot be reused.

- If business activities occur regularly, you should switch to using electronic invoices to save time and procedures.

- When creating a purchase list without input invoices (e.g., buying from farmers, individuals, etc.), you must clearly record the seller’s information, quantity, and unit price as a valid basis for requesting an output invoice.

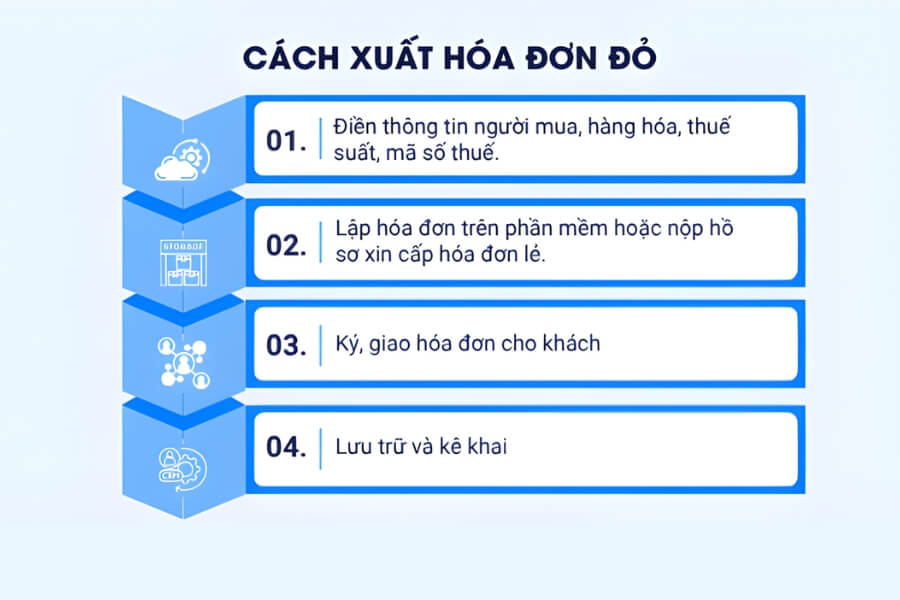

Guide on the steps to issue a red invoice

See more: Answers to all common questions about e-invoices and digital signatures today

4. Notes on issuing red invoices

Typically, a paper red invoice is made in 3 copies (white – red – blue), with each copy serving a different storage purpose. When creating an invoice, the following points should be noted to ensure its validity:

- Create all 3 invoice copies simultaneously: The copies must be written at the same time to ensure consistent content. Do not separate each copy to write different information.

- Record the buyer’s information completely and accurately: This includes name, address, and tax code (if any). Incorrect information can render the invoice invalid for use.

- No erasures or corrections: The entire content of the invoice must be written in one ink color, without any corrections or overwriting.

- Content must be continuous and clear: Do not leave breaks or blank lines; any unused spaces must be crossed out to prevent unintended content from being added.

- Invoice numbers must be issued in sequential order: Invoices must be issued in sequence from the smallest to the largest number, without skipping or omitting numbers.

- Record the correct time of issuance: The date on the invoice is the time the transaction occurred or the time the provision of goods or services was completed.

- Clearly state the payment method: Valid payment methods include cash or bank transfer, and it must be recorded according to the actual transaction.

5. Where to buy red invoices?

In reality, red invoices are not a commodity that can be freely bought and sold. The phrase “buying red invoices” is often misleading. According to legal regulations, sellers of goods and services are only allowed to use invoices issued or authorized by the tax authority, and these must be associated with a real economic transaction.

Depending on the specific case, businesses can be issued or use legal invoices in the following ways:

Case 1: Purchasing invoice books issued by the tax authority

<p style

Penalties are applied in the following cases:

- Losing, burning, or damaging a VAT invoice (copy 2) used for accounting, tax declaration, or state budget payment: fine from 4 – 8 million VND

- If the tax authority has grounds to determine that multiple invoices were reported lost at the same time → a penalty will be applied for each invoice

- In cases where there is a record of the incident, the seller has declared and paid taxes, and there are contracts and documents proving the transaction: With 1 mitigating factor → the lowest penalty rate will be applied OR With 2 mitigating factors → a warning will be issued

Recommendation

To mitigate the risks of losing, burning, or damaging input invoices, many businesses now opt for software to manage and process electronic input invoices. This helps with centralized storage, quick lookups, and minimizing errors during accounting and tax finalization.

6.6. Case 6: Penalty for not issuing invoices when selling goods or services

According to Decree 310/2025/NĐ-CP (effective from January 16, 2026), the act of not issuing invoices as prescribed will be penalized depending on the nature and number of violating invoices, specifically:

- Warning: Not issuing invoices for promotional goods, samples, gifts, internal consumption, etc., in very small quantities (01 invoice).

- Fine from 1 – 2 million VND: Not issuing 01 invoice when selling goods or providing services, or from 02 to under 10 invoices for cases of promotions, gifts, or internal consumption.

- Fine from 2 – 10 million VND: Not issuing from 02 to under 10 invoices when selling goods or providing services; or from 10 to under 50 invoices for cases of promotions or gifts.

- Fine from 10 – 30 million VND: Not issuing from 10 to under 20 invoices when selling goods or providing services; or from 50 to under 100 invoices for other cases.

- Fine from 30 – 50 million VND: Not issuing from 20 to under 50 invoices when selling goods or providing services.

- Fine from 60 – 80 million VND: Not issuing 50 or more invoices when selling goods or providing services.

Regulations on penalties for violations related to red invoices

7. Differentiating red invoices from other invoices

Below is a comparison table to help distinguish red invoices from other common types of invoices, to avoid confusion during use and tax declaration:

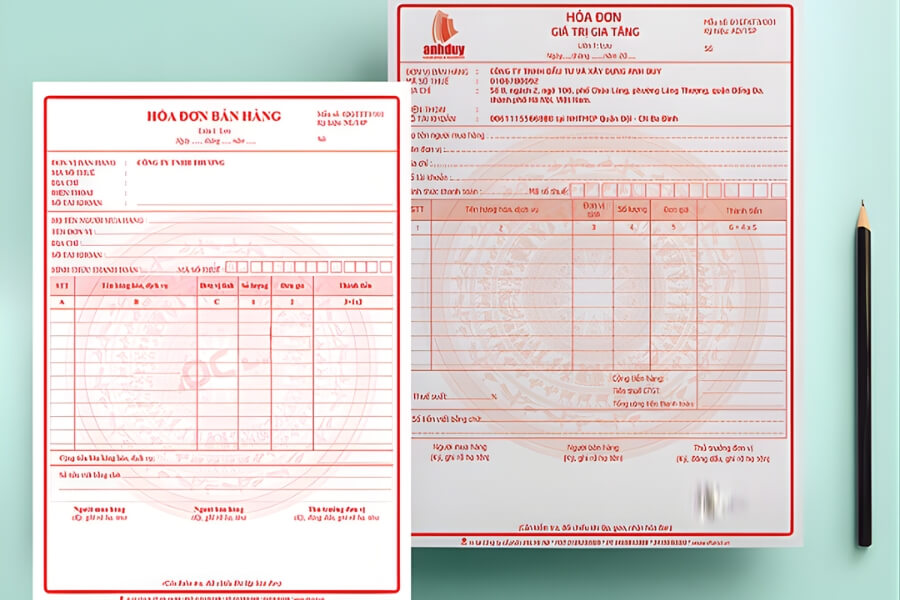

7.1. Differentiating red invoices from sales invoices

Below are the key differences to help distinguish red invoices (VAT invoices) from sales invoices, based on the user, tax calculation method, and declaration purpose:

Distinguishing Criteria Red Invoice (VAT Invoice) Sales Invoice Legal Name Value Added Tax (VAT) Invoice Sales Invoice Entities authorized to issue invoices Applicable to organizations and businesses that declare VAT using the deduction method, used for: – Selling goods and providing services domestically;

– International transport activities;

– Exporting to non-tariff zones and cases considered as exports;

– Exporting goods and providing services abroad.

Applicable to organizations and individuals that declare VAT using the direct method, including: – Selling goods and providing services domestically;

– International transport activities;

– Exporting to non-tariff zones and cases considered as exports;

– Exporting goods and providing services abroad;

– Organizations and individuals in non-tariff zones when selling goods domestically, conducting internal transactions within the non-tariff zone, or exporting abroad (the invoice must clearly state “For organizations and individuals in non-tariff zones”).

Signatures on the invoice Requires the signature of the seller and the signature of the organization’s legal representative (or a legally authorized person) Requires the signature of the seller VAT application method Applies the VAT deduction method; the tax rate and VAT amount are shown separately on the invoice Applies the direct VAT calculation method; VAT is not separated and is included in the value of the goods or services Illustration comparing red invoices & sales invoices

7.2. Differentiating Between Red Invoices and E-invoices

Since 2022, according to Decree 123/2020/ND-CP and now Decree 70/2025/ND-CP, e-invoices have become mandatory, gradually replacing traditional red invoices (paper invoices) in the sale of goods and provision of services.

Comparison of red invoices and e-invoices

Criteria Red invoice (paper) E-invoice Format Paper copy with red border, handwritten or printed Issued online, digitally signed Storage Stored as a hard copy Stored electronically for a minimum of 10 years Tax declaration Manual compilation and data entry Electronic declaration, connects to accounting software Risks Prone to tearing, loss, and errors More secure, easy to look up, fewer errors Actual usage Limited, only used in specific cases Mandatory for most households and businesses Red invoices have not been completely abolished, but are now only applicable in certain specific cases, such as:

- Businesses and business households that have not yet met the conditions for implementing electronic invoices

- Newly established entities that are in the process of completing initial procedures

- Some specific transactions approved in writing by the tax authorities

However, electronic invoices are the primary, mandatory, and widely encouraged form, helping to make transactions transparent, reduce risks, and facilitate tax management and declaration.

See more: Things to know about digital signatures and electronic invoices in businesses

8. Frequently Asked Questions about Red Invoices

1. What are the penalties for illegally printing and issuing red invoices?

The act of illegally printing, issuing, buying, or selling red invoices is a violation of the law and may result in heavy administrative fines or criminal prosecution, depending on the severity of the violation.

- For individuals:: Fines from 50 – 500 million VND, or non-custodial reform for up to 3 years, or imprisonment from 6 months to 5 years. Additionally, there may be a supplementary fine of 10 – 50 million VND, accompanied by a ban on holding certain positions or practicing certain professions for 1 – 5 years.

- For commercial legal entities: Fines from 100 million – 1 billion VND, or even permanent suspension of operations. Additionally, there may be a supplementary fine of 50 – 200 million VND, a ban on business activities, a ban on operating in certain fields, or a ban on capital mobilization for 1 – 3 years.

2. Do red invoices need to be stamped? Is a hanging seal valid?

According to current regulations, the law does not require red invoices to be stamped with the company seal. Therefore, a VAT invoice is still considered valid even without a seal, as long as other mandatory information is fully and correctly stated.

In cases where the invoice has already been given to the customer, using a hanging seal is appropriate and accepted. Therefore, a red invoice with a hanging seal still ensures legal validity according to current regulations.

3. Who must issue red invoices?

The entities required to issue invoices include:

- Businesses and business organizations (declaring VAT using the deduction or direct method).

- Business households and individuals who reach the prescribed revenue threshold (e.g., from 1 billion VND/year or more; some sectors must use electronic invoices from cash registers).

- Specific activities such as exports, e-commerce, and foreign suppliers.

Note: Some cases not subject to VAT or below the revenue threshold may not be required to issue invoices, but if the buyer requests one, it must be issued.

4. Are red invoices still used in paper form?

Since 2022, electronic invoices have been mandatory nationwide. By the 2025-2026 period (after Decree 70/2025/ND-CP takes effect from June 1, 2025), paper-based red invoices will almost no longer be used.

Paper invoices are only approved in some specific, temporary cases (for a maximum of 12 months), such as:

- Businesses and business households in remote, isolated, or island areas that do not have adequate internet infrastructure.

- Special cases permitted by the tax authorities.

After June 30, 2026, paper invoices will essentially become invalid (except for transitional provisions). Businesses that have adopted electronic invoices are not allowed to revert to using paper invoices.

5. What is the minimum amount for issuing a red invoice?

Since July 1, 2022 (and continuing to apply in the 2025-2026 period under the amended Decree 123/2020/ND-CP), there is no longer a minimum value threshold for issuing invoices. Accordingly, an invoice must be issued for every transaction of selling goods or providing services, regardless of the value (even if under 200,000 VND), except for some specific cases where a consolidated list is permitted.

The previous threshold of 200,000 VND per transaction has been officially abolished to align with the implementation of electronic invoices.

6. When is the time to issue a red invoice?

According to Article 9 of Decree 123/2020/ND-CP (amended by Decree 70/2025/ND-CP, effective from June 1, 2025), the time of invoice issuance is determined as follows:

- Sale of goods: When transferring ownership or the right to use to the buyer, regardless of whether payment has been received. For exports, it is no later than the next working day after customs clearance.

- Provision of services: The time to issue a red invoice is upon completion of the service. If payment is collected before or during the provision of the service, an invoice must be issued at the time of payment collection.

7. How to look up electronic red invoices?

Currently, you can look up electronic invoices (red invoices) to check their validity in the following ways:

- Look up on the General Department of Taxation’s portal (the most common and accurate method)

- Look up on the website of the electronic invoice provider

- Look up via the eTax Mobile application or accounting software

Answers to frequently asked questions about red invoices

Conclusion

In summary, red invoices still exist, but their scope of use is narrowing and they are subject to stricter management than before. Understanding the concept, issuance time, and new regulations regarding red invoices will help businesses and business households proactively comply with the law, avoiding errors and unnecessary tax risks from 2026 onwards.

To follow and quickly update the latest regulations on invoices, taxes, and accounting-finance, as well as to find solutions for more effective document management and operations, you can refer to more in-depth articles from 1Office – a platform that supports businesses with centralized, transparent, and legally compliant administration.