Fixed Asset Disposal Process for Corporate Accountants

Fixed asset liquidation is a crucial step that helps businesses optimize resources and minimize financial risks. However, to comply with legal regulations and avoid errors, the person in charge must clearly understand the steps, documentation, and important considerations. In this article, 1Office will provide you with a detailed fixed asset liquidation process, helping you implement it effectively, quickly, and in the most cost-efficient way!

Mục lục

- 1. Introduction to Fixed Asset Liquidation

- 2. The 8-step process for liquidating fixed assets

- 3. Required documents for fixed asset liquidation

- 3.1. Decision on Fixed Asset Liquidation

- 3.2. Fixed Asset Inventory Record

- 3.3. Fixed Asset Valuation Record

- 3.4. Invoices and Vouchers for Asset Sale (if sold for liquidation)

- 3.5. Asset Destruction Record (if destruction is performed)

- 3.6. Fixed Asset Write-Down Record

- 3.7. Accompanying Legal Documents (if any)

- 3.8. Related Financial Statements and Tax Records

- 4. Considerations When Performing Liquidation

- 5. Risk Management in the Fixed Asset Liquidation Process

- 6. Frequently Asked Questions (FAQ)

- 7. Tools & Solutions for Effective Asset Management

1. Introduction to Fixed Asset Liquidation

1.1. Definition

- Concept of fixed asset liquidation

Fixed asset liquidation is the process by which a business or organization terminates ownership and use of a fixed asset through methods such as selling, destroying, or converting its purpose of use.

This process typically occurs when an asset no longer has use value, is fully depreciated, damaged, irreparable, or no longer suitable for the company’s current production and business needs.

Fixed asset liquidation requires businesses to comply with legal regulations, including important steps such as inventorying, assessing the asset’s value, preparing liquidation documents, and recording the asset write-off in the books. This not only helps businesses optimize their finances but also ensures compliance with legal regulations, avoiding risks related to taxes and audits.

>>> See more: What are Fixed Assets? A Detailed Classification Guide

1.2. Why Businesses Need to Liquidate Fixed Assets

Fixed asset liquidation is one of the important operations for any business. This not only helps businesses manage assets effectively and optimally but also plays a crucial role in:

Optimizing financial resources

- When an asset no longer has use value or fails to meet production and business requirements, liquidation helps the company recover part of the asset’s value through sale or conversion. This money can then be reinvested in new projects or added to working capital.

Reducing maintenance costs and storage space

- Reducing maintenance costs and storage space

- Fixed assets that are no longer in use often incur costs for the business, including expenses related to maintenance, storage space, or operation. Liquidation helps the company eliminate unnecessary costs, optimizing its operational and running budget.

Meeting legal and tax requirements

- Liquidating fixed assets is a mandatory requirement when a business needs to write off an asset from its accounting books. Following the correct procedure helps the company comply with legal regulations, avoiding risks related to audits, taxes, and administrative penalties.

Updating and modernizing facilities

- By liquidating old, outdated assets to invest in new, modern equipment, businesses can enhance work efficiency and competitiveness in the market.

1.3. Cases Requiring Fixed Asset Liquidation

Fixed asset liquidation is a necessary and important task when an asset is no longer suitable or capable of serving production and business activities. The following are some common cases where a business needs to liquidate fixed assets:

- Cases requiring fixed asset liquidation

Assets are damaged and irreparable

- When a fixed asset is severely damaged and the repair cost exceeds its remaining actual value, the business needs to liquidate it to minimize losses.

Fully depreciated assets

- When fixed assets are fully depreciated and no longer in use, they are often liquidated to free up space, reduce storage costs, and optimize asset management.

Assets that are no longer suitable for use

- When production or business needs change, unsuitable assets such as outdated machinery and equipment will need to be liquidated to make way for more suitable, modern equipment.

Business restructuring or dissolution

- In cases such as business dissolution, merger, or restructuring, assets that are no longer in use will be liquidated to handle finances and allocate resources appropriately.

Assets repossessed by state authorities

- In certain specific cases, fixed assets may be repossessed or forced to be liquidated at the request of competent authorities, such as assets that are hazardous or violate the law.

- If an asset poses a danger to employees or affects the environment, the business must liquidate it to ensure safety and comply with environmental protection regulations.

1.4. Legal regulations on fixed asset liquidation

The liquidation of fixed assets must comply with specific legal regulations to ensure legality and transparency throughout the process. Below are some legal regulations on asset liquidation that businesses should note:

Regulations on fixed assets in businesses

-

- According to Circular 45/2013/TT-BTC of the Ministry of Finance, fixed assets are defined as assets with a value of 30 million VND or more and a useful life of over 1 year. When liquidating fixed assets, businesses must record the asset write-down and follow procedures in accordance with the law.

Tax regulations for fixed asset liquidation

- According to the Law on Tax Administration 38/2019/QH14, businesses must fully declare value-added tax (VAT) and corporate income tax (CIT) on the income from selling liquidated assets.

- VAT applies to fixed assets subject to value-added tax upon liquidation.

- For CIT, the income from asset liquidation is included in the business’s taxable income.

Regulations on auctioning liquidated assets (if applicable)

- If the liquidated asset has a high value or is state-owned, the business must comply with regulations on asset auctions according to the Law on Property Auction 2016. This process includes: publicizing auction information, organizing the auction, and handing over the asset according to the auction results.

Environmental protection regulations

- For assets with special characteristics, such as machinery and equipment that affect the environment, liquidation must comply with the regulations in the Law on Environmental Protection 2020. Specifically, businesses must process the assets according to environmental standards before selling or destroying them.

2. The 8-step process for liquidating fixed assets

Liquidating fixed assets is a crucial process that requires businesses to strictly follow steps to ensure legality, transparency, and efficiency. This process is typically divided into the following main steps:

Step 1: Inspect and identify assets for liquidation

First, the business needs to conduct a fixed asset inventory to identify assets that are no longer usable, damaged, or no longer suitable for current production and business requirements.

At this step, the business can also assess the remaining value and depreciation level of the assets to avoid wasting resources or losing assets.

Step 2: Establish a fixed asset liquidation council

After identifying the assets to be liquidated, the business needs to establish a dedicated council. This council typically includes representatives from management, accounting, and other relevant departments. The council will be responsible for appraising the asset’s value and proposing a suitable liquidation plan to ensure transparency and objectivity throughout the process.

Step 3: Prepare inventory and appraisal reports

The liquidation council will prepare a detailed inventory report on the condition, remaining value, and reason for liquidating each asset. At the same time, an asset appraisal report is also created to ensure the accuracy of the value and the legality of the liquidation.

Step 4: Create the fixed asset liquidation decision

Next, the business needs to draft and approve the fixed asset liquidation decision. This decision is signed and confirmed by the legal representative. The document must clearly state the reason for liquidation, the asset’s value, and the specific disposal method (sale, destruction, or reuse).

Step 5: Execute the fixed asset liquidation

The business and the person in charge will carry out the liquidation according to the approved plan. If the asset is sold, a sales contract must be signed and an invoice issued. If the asset is destroyed, the destruction must comply with legal regulations, especially environmental protection requirements.

Step 6: Write down the asset in the accounting books

- Writing down assets in the accounting books after liquidation

After completing the liquidation, the company’s accountant must update the books. This includes writing down the original cost, accumulated depreciation, and remaining value of the asset. Revenue and expenses related to the liquidation must also be fully recorded to ensure accuracy and transparency in the financial statements.

Step 7: Fulfill tax obligations and complete financial reporting

In addition to keeping complete records in the books, the business must declare value-added tax (if any) and include the income from asset liquidation in its corporate income tax return. This ensures compliance with legal regulations and avoids risks from tax authorities or auditors.

Step 8: Archive asset liquidation records

Finally, after completing all the above steps, all documents related to the liquidation process, such as inventory reports, liquidation decisions, and invoices, must be fully archived. These records serve as an important legal basis for reference in case of inspection by authorities or if disputes arise.

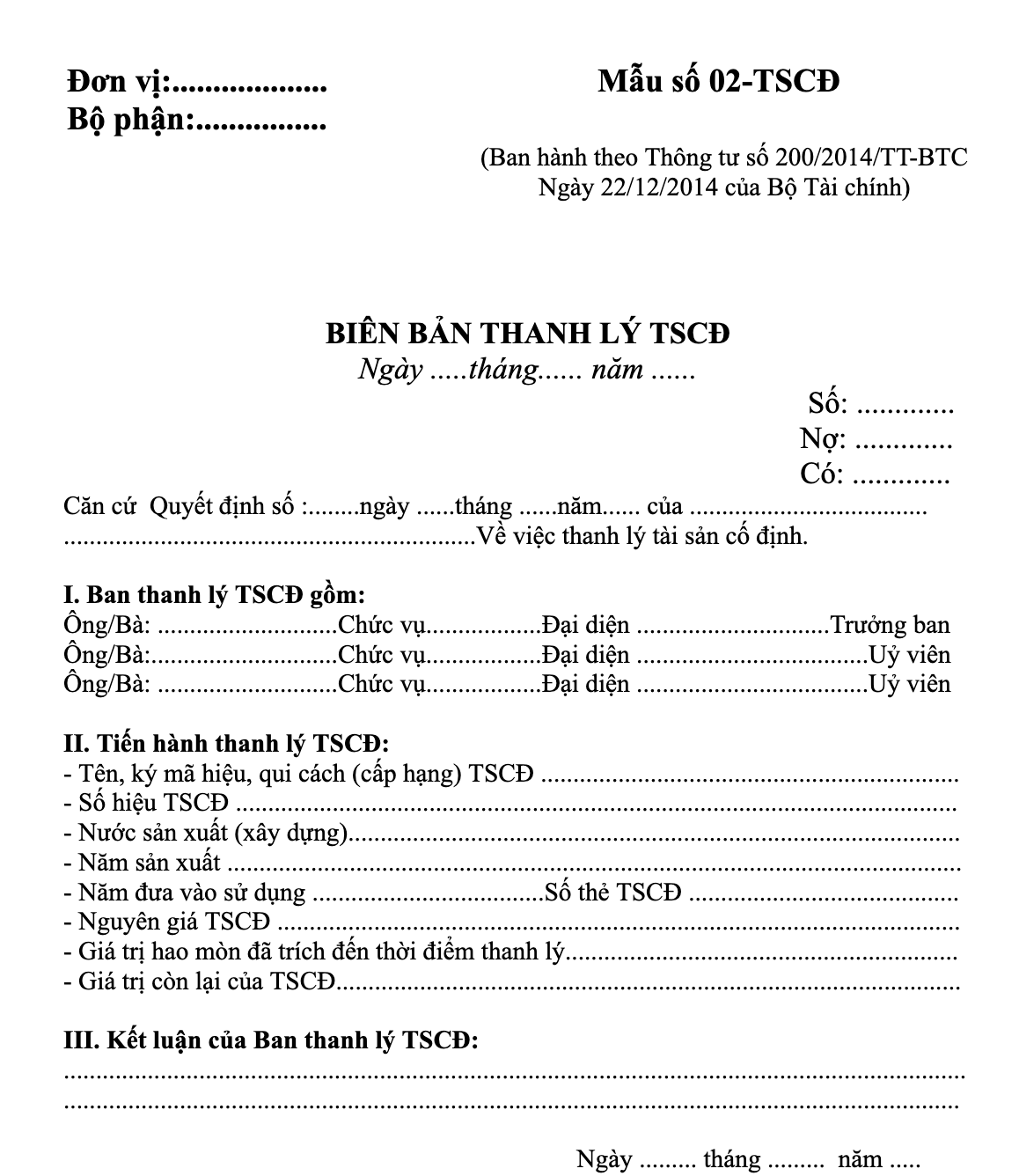

3. Required documents for fixed asset liquidation

3.1. Decision on Fixed Asset Liquidation

This decision will be issued by the legal representative or an authorized management level.

- Information about the asset being liquidated (name, asset code, original cost, remaining value).

- Reason for liquidation.

- Asset disposal plan (sale, destruction, or reuse).

3.2. Fixed Asset Inventory Record

This record is prepared by the inventory committee to confirm the condition and remaining value of the asset to be liquidated.

- List of fixed assets.

- Detailed information on the asset’s condition.

- Inventory results and proposed disposal plan.

3.3. Fixed Asset Valuation Record

- Fixed asset liquidation record

This document helps determine the asset’s value at the time of liquidation. The valuation record can be prepared by an internal committee or an independent valuation organization, and includes:

- Accumulated depreciation value.

- Remaining value on the accounting books.

- Market value (if necessary).

3.4. Invoices and Vouchers for Asset Sale (if sold for liquidation)

In cases where the asset is sold, the business needs to prepare:

- Asset sales invoice (value-added tax invoice or sales invoice).

- Fixed asset purchase and sale contract (if applicable).

3.5. Asset Destruction Record (if destruction is performed)

If the asset is destroyed, a record must be created to document the destruction process, with the main contents including:

- Time and location of destruction.

- Method of destruction (ensuring compliance with environmental protection regulations).

- Representatives witnessing the destruction process.

3.6. Fixed Asset Write-Down Record

After completing the liquidation, the company’s accountant prepares a record to write down the asset in the accounting books.

- Information on the asset being written down.

- Original cost, accumulated depreciation, remaining value.

- Write-down date and related attached documents.

3.7. Accompanying Legal Documents (if any)

In some special cases, the business needs to add:

- Documents proving ownership of the asset.

- Permits from competent authorities (if the asset requires approval for liquidation).

The accountant needs to ensure that tax-related documents are updated:

- Reporting income from asset liquidation for corporate income tax.

- Value-added tax declaration records (if any).

>>> DOWNLOAD THE COMPLETE SET OF FIXED ASSET LIQUIDATION RECORD TEMPLATES

4. Considerations When Performing Liquidation

Correctly Identify the Reason and Purpose of Liquidation

- The business needs to carefully assess the condition and role of the fixed asset before deciding to liquidate it. Some common reasons include the asset being damaged or fully depreciated. The liquidation objective must be clearly defined to avoid waste or loss of assets.

Accurate Accounting Records

The liquidation process must be fully recorded in the accounting books, including:

- Writing down the value of the fixed asset (original cost, accumulated depreciation, remaining value).

- Recording revenue or expenses related to the liquidation.

- Fully declaring all taxes (if any), including value-added tax and corporate income tax.

Complete Management of Records and Documents

After liquidating the asset, the fixed asset liquidation records need to be carefully stored, including some important documents such as:

- Liquidation decision.

- Inventory record, valuation record.

- Contract, liquidation sales invoice (if any).

This helps the business easily cross-reference in case of an audit or dispute.

Notes on Taxes and Financial Reporting

- Fixed asset liquidation can give rise to tax obligations. The business needs to ensure full declaration and payment of related taxes to avoid legal violations or penalties from tax authorities.

5. Risk Management in the Fixed Asset Liquidation Process

The fixed asset liquidation process is not merely about selling or disposing of a fully depreciated asset; it is an activity that directly affects the company’s financial, legal, and reputational standing. Therefore, managing risks at each step of the liquidation is a key factor in ensuring transparency, efficiency, and sustainability.

5.1. Legal Risks

One of the biggest risks during the liquidation process is non-compliance with legal regulations. This can happen when the business:

-

Liquidates without an approved decision from the management or board of directors.

-

Fails to prepare complete records, inventory reports, valuations, or related documents.

-

Liquidating assets without the involvement of state management agencies (if the assets require registration, such as cars, heavy machinery, etc.).

The consequences can lead to disallowed expenses by tax authorities or auditors, tax arrears collection, or even administrative penalties.

Solution: Businesses need to build a strict legal process, clearly assign responsibilities to each department (accounting, legal, asset management), and promptly update on state regulations regarding asset liquidation.

5.2. Financial Risks

The most common mistake is inaccurate asset valuation. If the valuation is lower than the market value, the business can suffer significant losses. Conversely, if the valuation is too high, the liquidation process will be prolonged, causing cash flow stagnation and increasing storage and maintenance costs.

Solution: It is necessary to use an independent valuation unit to ensure objectivity, while also comparing multiple reference sources (market price, previous liquidation prices, public auction platforms).

5.3. Operational Risks

In practice, many businesses face loss or fraud during liquidation: employees arbitrarily dismantle components, swap asset parts, or record incorrect data. Additionally, unscientific storage of liquidation records makes it difficult for businesses to control and can easily lead to internal disputes.

Solution: Implement fixed asset management software to track the status, value, depreciation history, and the entire liquidation process. Every step needs to have clear records and signed confirmations from multiple relevant departments to prevent fraud.

5.4. Reputational Risks

Asset liquidation is a public activity within a business. A lack of transparency can easily create negative public opinion from employees, shareholders, or partners. For example, if there are suspicions that assets are being “sold cheaply” to acquaintances, the business not only suffers financial losses but also loses market trust.

Solution: Make the entire process transparent by publishing internal information, choosing public auctions instead of direct sales, and periodically reporting liquidation results to the board of management.

Risk management in fixed asset liquidation is a multi-layered process, including: ensuring legal compliance, financial control, operational management, and protecting the business’s reputation. Proactively identifying risks and applying preventive measures helps businesses not only avoid losses but also optimize recovery value, building a professional and transparent image in the eyes of partners and shareholders.

6. Frequently Asked Questions (FAQ)

6.1. Do fully depreciated fixed assets still require liquidation records?

Even if a fixed asset is fully depreciated, the business still needs to create liquidation records to ensure transparency and legal compliance. These records help document that the asset is no longer in use in the accounting books and avoid disputes or inspections from tax authorities.

6.2. When is it necessary to hire an asset valuation organization?

A business needs to hire an asset valuation organization in cases such as:

- The asset has a high value and requires accurate valuation for sale or auction.

- There is not enough internal expertise to appraise the asset’s value.

- Tax authorities or the law require a valuation to ensure transparency.

Hiring a valuation organization helps the business mitigate the risk of price disputes and comply with legal regulations.

6.3. Who should be on the liquidation committee?

A liquidation committee is usually established to ensure objectivity and transparency during the process. The committee members typically include:

- The legal representative or director of the business.

- A representative from the accounting and finance department.

- A representative from the asset management department.

- Other relevant parties depending on the scale and internal regulations of the business.

6.4. What to do if an asset needs to be destroyed instead of sold?

In cases where an asset has no remaining useful value or would be harmful if reused, the business must destroy it. The destruction process must be carried out correctly and be certified with a record to ensure safety and compliance with environmental regulations.

7. Tools & Solutions for Effective Asset Management

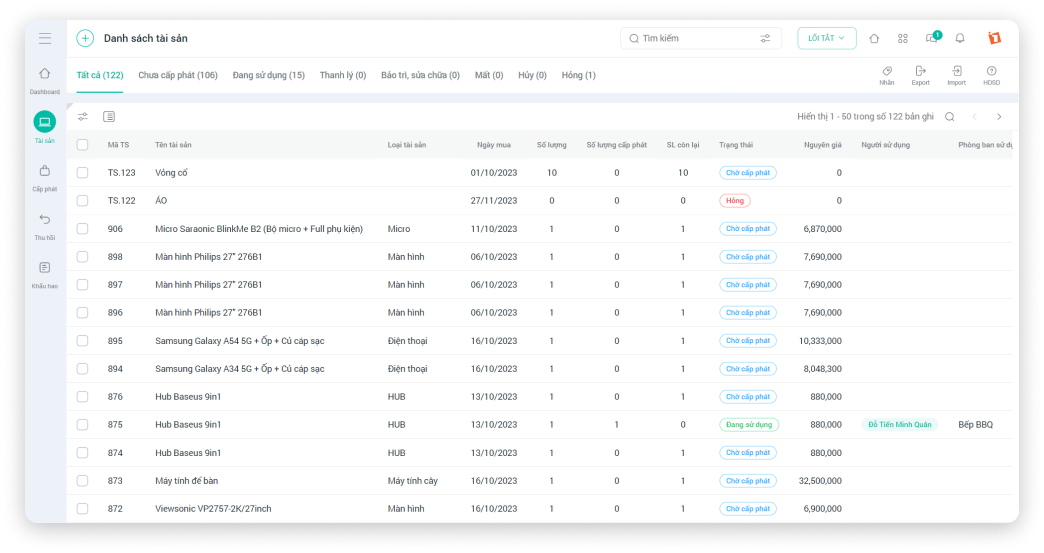

Effective asset management is one of the key factors in optimizing resources and improving a business’s operational efficiency. To achieve this, many businesses have gradually shifted from manual management to using modern asset management software solutions. One of the outstanding solutions is 1Office with its superior Asset Management feature:

- Professional asset management software 1HRM

Register for a free feature Demo

Comprehensive asset lifecycle management

From procurement, operation, and maintenance to liquidation, the software helps businesses control the entire asset lifecycle. This makes it easy for businesses to track the status of assets at each stage.

Track status and usage history

1Office allows for real-time updates of asset status, recording usage history and any incidents that arise, thereby helping to optimize maintenance and minimize the risk of damage.

- Quickly declare asset increases and decreases

- Easily categorize assets for better management

- Update detailed asset status: allocation, retrieval, liquidation, damage, repair, etc.

Tightly integrated with other management processes

1Office’s asset management module seamlessly integrates with other functions such as human resource management, finance, and work. This provides businesses with a more comprehensive and accurate overview of their operations.

Intelligent data reporting and analysis

The system automatically generates detailed reports on asset value, depreciation status, and related costs, helping businesses make timely and effective decisions.

- Search and retrieve assets with smart filters

- Comprehensive, detailed, and multi-dimensional reporting dashboard

- Store the entire history of asset allocation, retrieval, and liquidation