What is a budget? How to create and manage an effective budget plan

Budget – A familiar term in business and marketing strategies and campaigns, but understanding it correctly and applying it effectively is not simple. So, what exactly is a budget? How do you create a budget plan to maximize efficiency? Let’s explore the details with 1Office in the article below.

Mục lục

- 1. What is a budget?

- 2. Types of budgets

- 3. Why do businesses need to plan a budget?

- 3. 5 Important Principles to Master Before Creating an Effective Budget

- 4. Top 5 Common and Effective Budgeting Techniques for Businesses

- 5. Guide to an Effective Budgeting Process for Businesses

- 5. Guide to Budget Management in a Business

- 6. 1CRM – An Effective Solution for Managing Project Budgets and Cash Flow

1. What is a budget?

A budget is a financial plan for estimating, calculating, and managing the income and expenses of an individual or organization over a specific period.

In a business, a basic budget plan identifies financial goals and forecasts revenue, expenses, and profits. A budget can be created for a short-term cycle (a few months to 1 year) or a long-term one (from 3 to 10 years).

Typically, a business will create an annual budget that coincides with its fiscal year and is allocated monthly or quarterly. This makes it easier to prepare the budget and compare actual results with the initial plan.

2. Types of budgets

In a business, various types of budgets are established to manage and control finances, including the sales budget, production budget, direct labor budget, and advertising and marketing budget, among others.

To better understand what a budget is in a business context, this article will focus solely on the master budget – the highest-level objective of the budgeting process, which consolidates all budgets from departments, branches, segments, or other significant units within the company.

The master budget includes:

- Operating budget: Identifies the resources needed to carry out planned activities such as production, sales, services, purchasing, marketing, etc. A company’s operating budgets are consolidated into a pro forma income statement, showing total revenue, total expenses, and profit.

- Financial budget: Determines the sources of funds and how they will be used for planned activities, including plans for income, expenses, cash flow, investments, and long-term financial strategy. The financial budget includes the cash budget, pro forma cash flow statement, pro forma balance sheet, and capital expenditure budget.

To optimize value, the master budget must include overall company-wide metrics and metrics allocated to each department. Ideally, each department will be deeply involved in the budgeting process according to the guidelines described in the following section.

3. Why do businesses need to plan a budget?

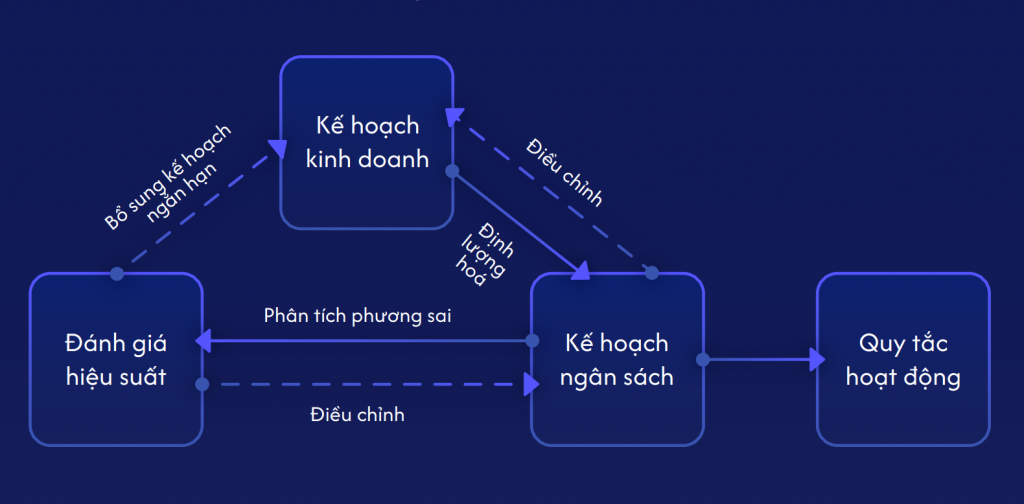

A budget is created to quantify the elements of a business plan and measure the financial resources needed for the company to achieve its goals. Based on the proposed budget, management will adjust the business plan, and then readjust the budget.

Based on the projected revenue and expenses in the budget plan, the business will establish a set of operating rules for employees to follow throughout the year.

The budget also serves as a tool for measuring and evaluating the performance of the business and its individual departments. Regularly comparing the initial plan with actual revenue and expenses helps the company understand its operational status and its ability to achieve its stated goals. Management can then further adjust the budget or create a new short-term business plan to address any issues.

In addition, a budget plays other roles in a business, such as:

- Effective resource allocation: A budget plan helps specify the resources needed for each department, such as the number of employees and the volume of raw materials. This ensures a rational and balanced allocation of resources among departments.

- Cost control: A budget helps a business be more proactive and disciplined in its spending decisions. Regularly comparing actual and projected costs helps to quickly identify issues and make necessary adjustments.

- Cash flow management: Planning income and expenses in a budget helps a business manage its cash flow effectively, ensuring sufficient resources to maintain daily operations and invest in future opportunities.

- Motivating personnel: A budget helps all personnel understand the company’s goals and plans, thereby motivating them to contribute to its overall success. A challenging budget can also stimulate employees’ efforts.

- Connecting departments: The budgeting process helps departments within the company understand and coordinate with each other to make the best decisions. For example, the sales department can use feedback from the customer service department to forecast sales and share this information with the production department.

3. 5 Important Principles to Master Before Creating an Effective Budget

Principle 1: An effective budget plan must originate from the business plan

If it lacks a connection to strategic goals, the budget will merely replicate the previous year’s results with minor changes, offering no practical value for the future.

Principle 2: The budget needs to be balanced across departments.

For example, the sales department may tend to allow customers to buy on credit to increase sales, while the accounting department wants to limit bad debt. The business needs to establish common financial standards to harmonize departments.

Principle 3: All levels of management need to participate in the budgeting process.

It shouldn’t just happen in high-level leadership meetings; it requires the involvement of lower-level managers, as they best understand what can and cannot be achieved, along with the necessary resources.

Principle 4: Personnel need to feel a sense of ownership over the budget

All levels of personnel should contribute their opinions to the budget creation and adjustment process, rather than having it imposed on them. The budget should be seen as a tool to support effective work, not just for control and accountability assessment.

Principle 5: The budget plan must be flexible and transparent

The budget needs to be monitored and adjusted in a timely manner, rather than relying on a fixed plan that is no longer relevant to reality. The items in the budget must have clear justifications and specific explanations, and the approval process must follow a standard procedure.

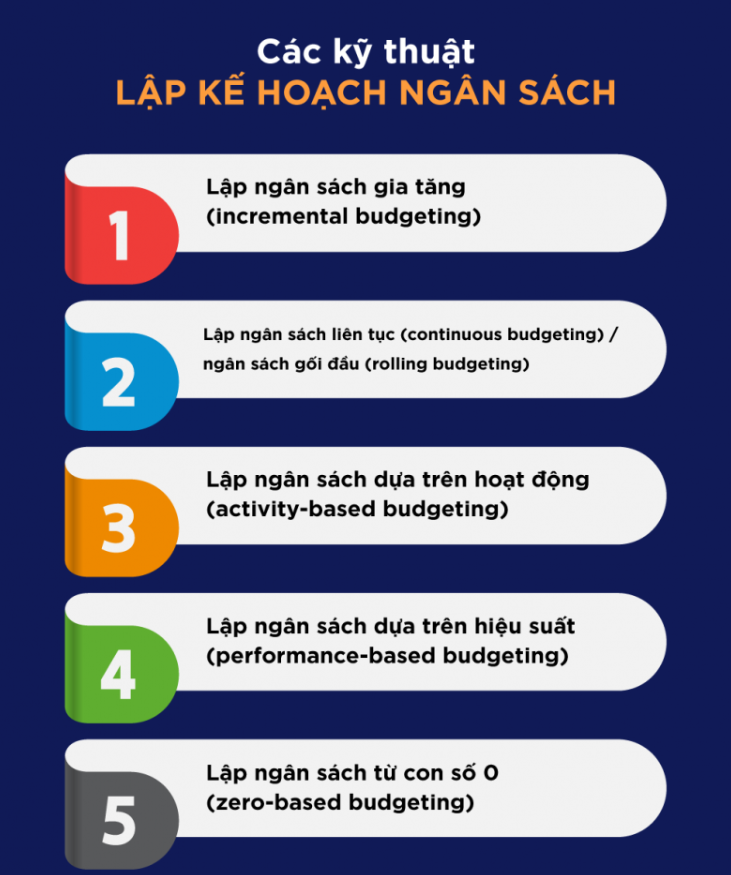

4. Top 5 Common and Effective Budgeting Techniques for Businesses

Each budgeting technique has its own advantages and disadvantages. The choice of the appropriate technique will depend on many factors such as the type of business, industry, business model, strategic goals, and the implementation capacity of each company. Sometimes, a flexible combination of different techniques will yield the best results.

4.1. Incremental Budgeting

Incremental budgeting: In this technique, the budget for the next period (usually a fiscal year) is built based on the previous period’s budget, with adjustments to reflect expected changes in business operations such as increases or decreases in sales, production costs, personnel costs, etc. This approach is based on the principle of increasing or decreasing by a fixed amount (e.g., 5%, 10%) compared to the previous period’s budget.

- Advantages:

- Simpler and more time-efficient than creating a budget from scratch.

- Stable because it is based on the previous period, making it easy to track, manage, and evaluate performance.

- Disadvantages:

- Can lack necessary flexibility and may not fully reflect fluctuations or changes in the business environment.

- Encourages maintaining the status quo, limiting creativity and the drive for improvement.

- Risks missing new business opportunities.

4.2. Continuous Budgeting

Continuous budgeting, also known as rolling budgeting: The business continuously updates the budget. At the end of a short period (usually a month or a quarter), the company adds a new month’s or quarter’s budget to the plan.

- Advantages:

- Emphasizes flexibility, allowing for continuous adjustments, which helps in adapting quickly to market changes and business conditions.

- Provides a more accurate view of the near future, based on continuously updated forecasts.

- Creates motivation to improve performance, maintaining or exceeding previous budget targets.

- Disadvantages:

- Requires significant resources (manpower, time, management costs) to carry out continuous planning, monitoring, and adjustment.

- Not stable for long-term forecasting.

4.3. Activity-Based Budgeting

Activity-based budgeting: This technique is based on analyzing the specific activities a business performs to achieve its business goals. The business collects data to assess the costs and resources required for each activity. The budget is then allocated based on cost standards.

- Advantages:

- Identifies detailed costs, helping management understand the cost structure and allocate resources effectively.

- Focuses on value-creating activities and cuts unnecessary costs.

- Provides specific information to evaluate performance and optimize work processes.

- Allows for continuous business improvement.

- Disadvantages:

- Requires significant resources (personnel, time, management costs) to plan, monitor, and analyze activities.

- Involves a detailed and complex process that can be difficult for some businesses to implement and manage.

4.4. Performance-Based Budgeting

Performance-based budgeting: This is a technique for allocating financial resources based on performance (goals, targets) and results achieved in the past or projected for the future. High-performing departments receive more resources, while low-performing departments may receive less and need to improve to be allocated more budget.

- Advantages:

- Enhances transparency in budget allocation.

- Promotes a sense of responsibility for individuals and departments.

- Encourages creativity and innovation to improve performance and optimize business results.

- Disadvantages:

- Budget allocation priorities may be inaccurate if performance measurement is flawed or if some activities cannot be measured with visual indicators.

- Creates significant pressure and internal competition among departments.

- Can lead to incorrect decisions or unintended consequences, such as excessively cutting resources for low-performing activities.

4.5. Zero-Based Budgeting

Zero-based budgeting: In this technique, every expense must be identified and justified from scratch, without relying on previous budget usage. Departments need to determine projected costs, provide detailed explanations, and defend their budget plans. Each expense is carefully reviewed, and the budget is only approved with a compelling reason.

- Advantages:

- Encourages resource savings, eliminates waste, and optimizes budget allocation and use.

- Promotes transparency and clarity in budget use and management.

- Encourages creativity and innovation to save costs and improve performance.

- Disadvantages:

- Requires significant resources (personnel, time, costs) to build a completely new plan and defend it multiple times before finalizing.

- Budget allocation priorities can be influenced by subjective factors, such as the department representative’s ability to argue their case.

- Can cause stress and resistance from departments due to the detailed and complex process.

5. Guide to an Effective Budgeting Process for Businesses

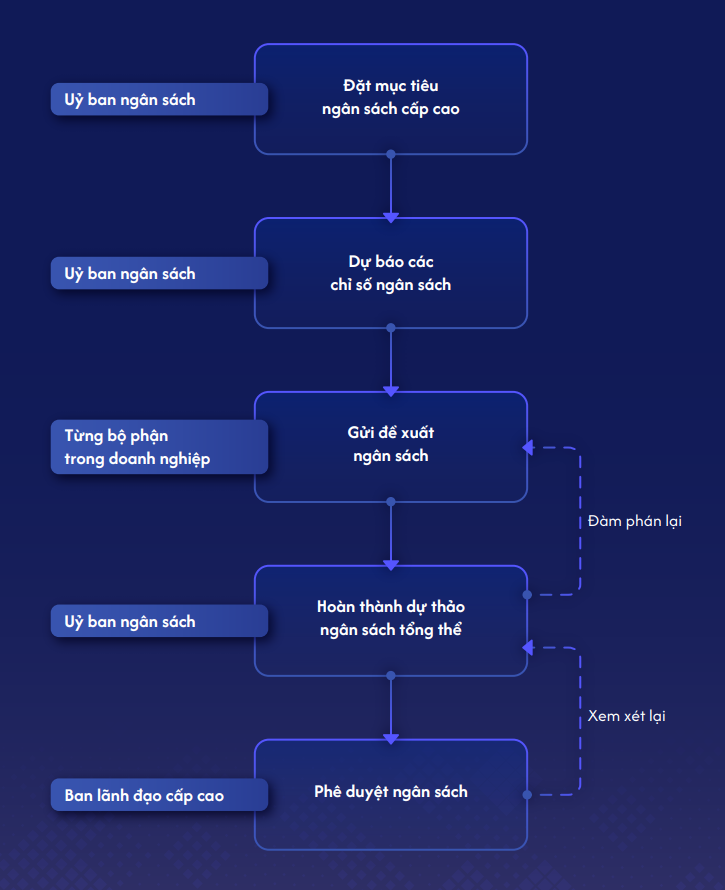

Step 1: Establish a budget committee & set high-level budget goals

The budget planning process in a business begins with establishing a budget committee, which includes members from various departments with different roles such as CEO, CFO, finance and accounting specialists, business strategy experts, and department representatives.

The committee’s responsibilities include:

- Establishing the budget planning process and providing guidance to relevant individuals and departments.

- Collecting and reviewing information for budgeting purposes.

- Evaluating and determining cost and investment priorities.

- Forecasting and estimating revenue, costs, and financial indicators.

- Finalizing the overall budget plan and approval steps.

- Monitoring and evaluating budget implementation, and making adjustments as needed.

Based on the business plan, the committee will set high-level budget goals, such as revenue growth, profitability, cost reduction, market share expansion, and increasing stock value.

Step 2: Forecast Budget Indicators

Forecasting budget indicators includes sales volume, profit, operating costs, revenue streams, and other financial metrics. This process is based on the business plan, past and present performance indicators, and a PESTEL analysis of the business environment.

Common forecasting methods:

- Time series analysis: Predicting future values based on past observations.

- Causal forecasting: Identifying the cause-and-effect relationship between budget indicators and other variables.

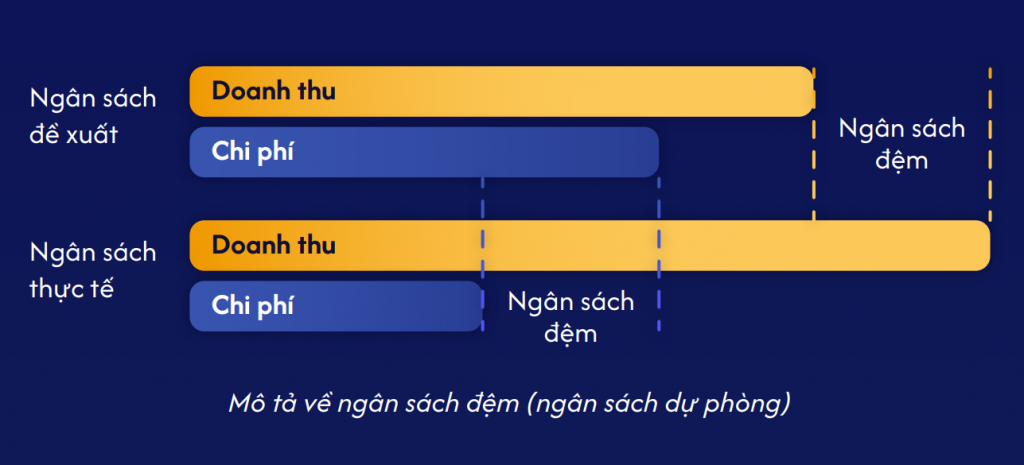

Step 3: Submit Budget Proposals (for bottom-up budgeting)

In the bottom-up budgeting method, each department prepares an initial budget proposal based on guidance from the budget committee. The proposal is submitted to higher management and may be revised to align with overall goals. When expenditures exceed revenue, the business can use budgetary slack to avoid a budget deficit.

Step 4: Negotiate and Finalize the Budget

Budget proposals are reviewed and analyzed for compliance and alignment with business objectives. Negotiations take place between department managers and senior management to finalize the proposals. After consolidating proposals from all departments, the budget committee will conduct technical and strategic analysis, updating and revising to complete the overall budget.

Step 5: Review and Approve the Final Budget

The overall budget is presented to senior leadership for approval. The budget committee may need to justify its approval decisions. Once approved, the budget plan is announced and implemented throughout the company.

5. Guide to Budget Management in a Business

Step 1: Track and Record the Budget

The main goal of this step is to establish a comprehensive database system for the financial situation, covering processes, tools, and personnel, creating a solid foundation for evaluating and adjusting the budget in later stages.

The budget tracking and recording process should be implemented synchronously across departments and specialized responsibility centers:

- Cost Center: C&B department, accounting, procurement…

- Revenue Center: Business locations, retail department, customer care…

- Profit Center: Customer segments, product lines…

- Investment Center: Business strategy department, R&D…

Budget data must be accurately updated in financial reporting tools at the end of the period. Throughout the financial period, the business should use financial management tools to automatically record and continuously monitor this data.

Step 2: Evaluate Budget Utilization Results

Budget evaluation can be conducted from two main perspectives, depending on the company’s strategy and operating environment:

- Perspective 1 – Achieving Goals: Actual costs may exceed the budget, but if it helps achieve priority objectives (with a clear explanatory report), it is still acceptable.

- Perspective 2 – Strict Control: All cost norms are detailed, and spending beyond the initial plan is not permitted.

Analysis of variance (ANOVA) is a tool for comparing actual costs and revenues with budget targets over the same period. If the analysis takes place after the end of the reporting period, it is an evaluation of the final results. Conversely, if the analysis is performed during the implementation period, it is an assessment of budget progress.

Departments need to report periodically (weekly, monthly, etc.) on budget usage and explain any unusual factors. This allows the business to promptly identify issues and make appropriate adjustments.

Step 3: Adjust the budget

A budget plan, even after approval, may still need to be adjusted when circumstances change beyond control. This is the focus of the rolling budgeting technique.

However, budget adjustments should not be made too frequently to avoid undermining the seriousness of the planning process. Businesses should limit adjustments to a maximum of twice a year, and only make changes when absolutely necessary.

When adjustments are needed, two options can be considered:

- Postpone activities to wait for new financial resources in the next cycle.

- Continue implementation, while reallocating unused or surplus budget items to cover shortfalls, ensuring the total budget value remains unchanged.

6. 1CRM – An Effective Solution for Managing Project Budgets and Cash Flow

1CRM can aggregate and display data from various sources on a single dashboard system. This system allows for in-depth customization of visualizations, metric analysis, and forecasting. Notably, all transaction, operational, and financial management activities are connected in real-time.

With 1CRM, managers can:

- Forecast budgets accurately and quickly: 1CRM integrates business data on sales, revenue, etc., into a single system, recorded over the long term and updated automatically in real-time. This creates a comprehensive and accurate database for budget forecasting. The dashboard system is designed to be intuitive and allows for customization from various perspectives, significantly speeding up the analysis and forecasting process.

- Visualize the overall budget picture: In 1CRM, the overall budget for each project is visualized like an organizational chart or a business goal tree. When budget changes occur, the business doesn’t need to send new document files but can update directly on this system. Data access is strictly controlled through permissions, ensuring security.

- Quickly detect emerging issues: With pre-standardized processes, any unusual signs during budget implementation are detected quickly. Information about the causes, consequences, and involved parties is also clearly recorded.

Register for a free 1CRM feature Demo account!

——————————

We hope that through this article, managers have gained a clear understanding of the concept of a budget and a detailed, systematic view of creating and managing budgets for their business. This not only helps businesses maintain tight financial control during years of economic volatility but also serves as a solid foundation for sustainable future growth. We wish your business continued ease and success!