Business Dissolution Decision Template & Detailed A–Z Procedures (Updated 2026)

Business dissolution is an important legal procedure, marking the complete termination of a business’s legal existence within the state management system. Properly understanding the nature, conditions, documents, and process of dissolution will help businesses avoid legal risks, tax issues, and joint liability in the future.

The article below provides a complete guide – updated for 2026 – on business dissolution, along with a standard Business Dissolution Resolution Template and important practical notes.

Mục lục

- 1. General Introduction to Business Dissolution

- 2. Cases of Business Dissolution According to Law

- 3. Conditions for Business Dissolution

- 4. Enterprise Dissolution Decision Template (Updated 2026)

- 5. Detailed A–Z Process and Procedures for Business Dissolution

- 6. Detailed Sample Business Dissolution Dossier

- 7. Special Cases and Important Notes When Dissolving a Business

- 8. Common Mistakes and Practical Experience

- 9. Frequently Asked Questions (FAQs)

1. General Introduction to Business Dissolution

1.1. What is Business Dissolution?

Business dissolution is a legal procedure to completely terminate the legal entity status of a business when it no longer has the need or fails to meet the conditions to continue its business operations.

After dissolution is complete:

- The business no longer has legal rights and obligations

- The business registration number is permanently invalidated

- No business activities can be carried out

1.2. The Legal Nature of Dissolution

In terms of legal nature, business dissolution is not simply ceasing operations, but a process of settling all legal rights and obligations that have arisen throughout the business’s existence.

A business is only considered legally dissolved when it simultaneously meets all of the following conditions:

- Has paid off all debts

- Has completed all tax obligations

- Has ensured employee benefits

- Has had its status updated to “Dissolved” by the business registration authority

1.3. Distinguishing Between Dissolution and Bankruptcy

In practice, many businesses often confuse dissolution and bankruptcy. However, these are two legal procedures that are completely different in terms of nature, conditions, and handling authority.

| Criteria | Dissolution | Bankruptcy |

| Voluntary Nature | Can be voluntary | Mandatory |

| Solvency | Able to pay debts | Unable to pay debts |

| Handling Authority | Department of Planning & Investment | Court |

| Nature | Administrative – Legal | Judicial |

In other words, dissolution applies to businesses that are still able to handle their financial obligations, while bankruptcy is the final measure when a business is no longer able to pay its debts.

2. Cases of Business Dissolution According to Law

2.1. Voluntary Dissolution

A business may be voluntarily dissolved in one of the following cases:

- The operating period specified in the company’s charter has ended without a decision to extend it

- By decision of the owner, the Members’ Council, or the General Meeting of Shareholders (depending on the type of business)

- There is no longer a need to continue business operations, a change in investment strategy, or a shift in development direction

In these cases, the business proactively carries out the dissolution procedures, provided that it fully meets the dissolution conditions as prescribed by law.

2.2. Compulsory Dissolution

A business is subject to compulsory dissolution when:

- It fails to maintain the minimum number of members as required by the Law on Enterprises for a statutory period without converting its business type

- Its Certificate of Business Registration is revoked due to serious violations of the law

In the case of compulsory dissolution, the business must still fulfill all financial, tax, and labor obligations before its dissolution status is recognized by the state authorities.

3. Conditions for Business Dissolution

According to current enterprise law, a business will only be approved for dissolution by state authorities if it simultaneously meets all of the mandatory conditions below. Failure to meet or complete any of these conditions may result in the dissolution application being suspended, returned, or delayed.

3.1. The Business Has Paid All Debts and Property Obligations

The business must prove that it has fully paid all debts and property obligations arising during its operation, including but not limited to:

- Debts to partners, suppliers, and credit institutions

- Other financial obligations under signed contracts

- Debts arising from compensation or penalties for breach of contract (if any)

The payment of debts must comply with the order of priority as prescribed by law, in which:

- The rights of employees

- Tax and financial obligations to the State

are always prioritized over other debts.

A business cannot be dissolved if it still has outstanding debts, even a small amount or one that is under negotiation.

3.2. The Business Is Not Involved in Dispute Resolution at a Court or Arbitration

One of the mandatory conditions for dissolution is that the business is not a party to any dispute currently being resolved at:

- A competent People’s Court

- A Commercial Arbitration Center

Disputes may include:

- Economic contract disputes

- Labor disputes

- Disputes among members/shareholders within the business

The business can only proceed with the dissolution procedure after the dispute has been resolved and the resolution is legally effective. Intentionally submitting a dissolution application while a dispute is ongoing may result in the application being rejected or penalties for violation.

Fulfilling Obligations to Employees

The business must ensure:

- Full payment of outstanding wages

- Payment of severance allowance, job loss allowance (if any)

- Completion of social insurance, health insurance, and unemployment insurance contributions

- Proper implementation of the labor utilization and contract termination plan as required by law

All employee benefits must be settled before submitting the dissolution application.

Fulfill Obligations to the Tax Authority

The enterprise must:

- Finalize all incurred taxes (Corporate Income Tax, Personal Income Tax, VAT, etc.)

- Submit all outstanding tax declarations

- Have no outstanding tax debts, penalties, or late payment fees

- Receive confirmation from the tax authority of completed tax obligations and the termination of the tax identification number’s validity

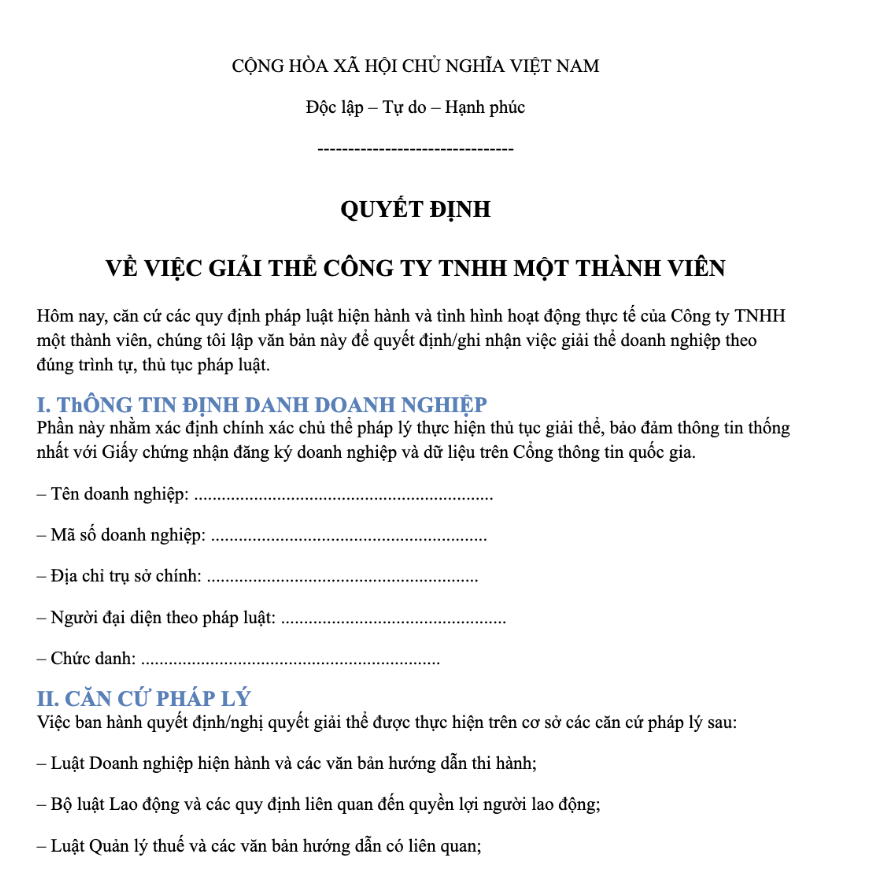

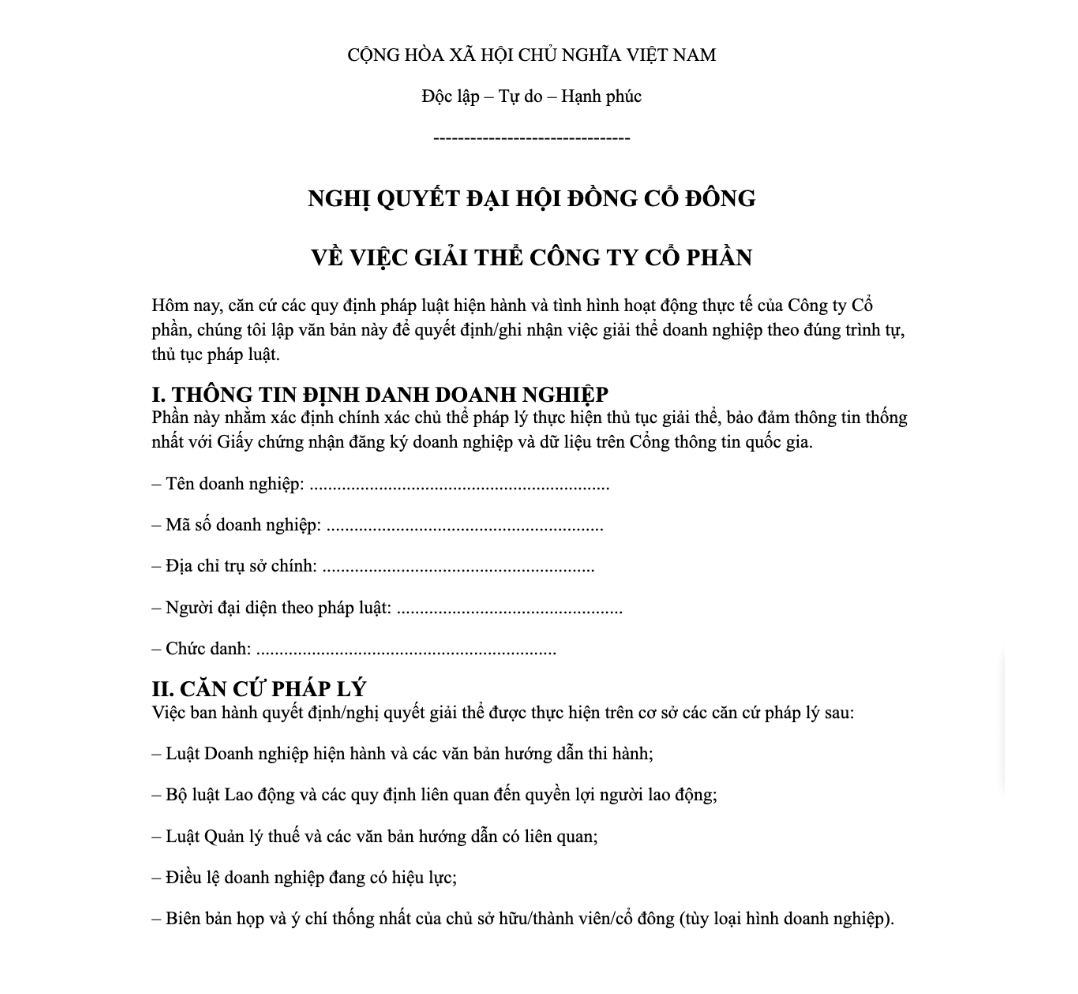

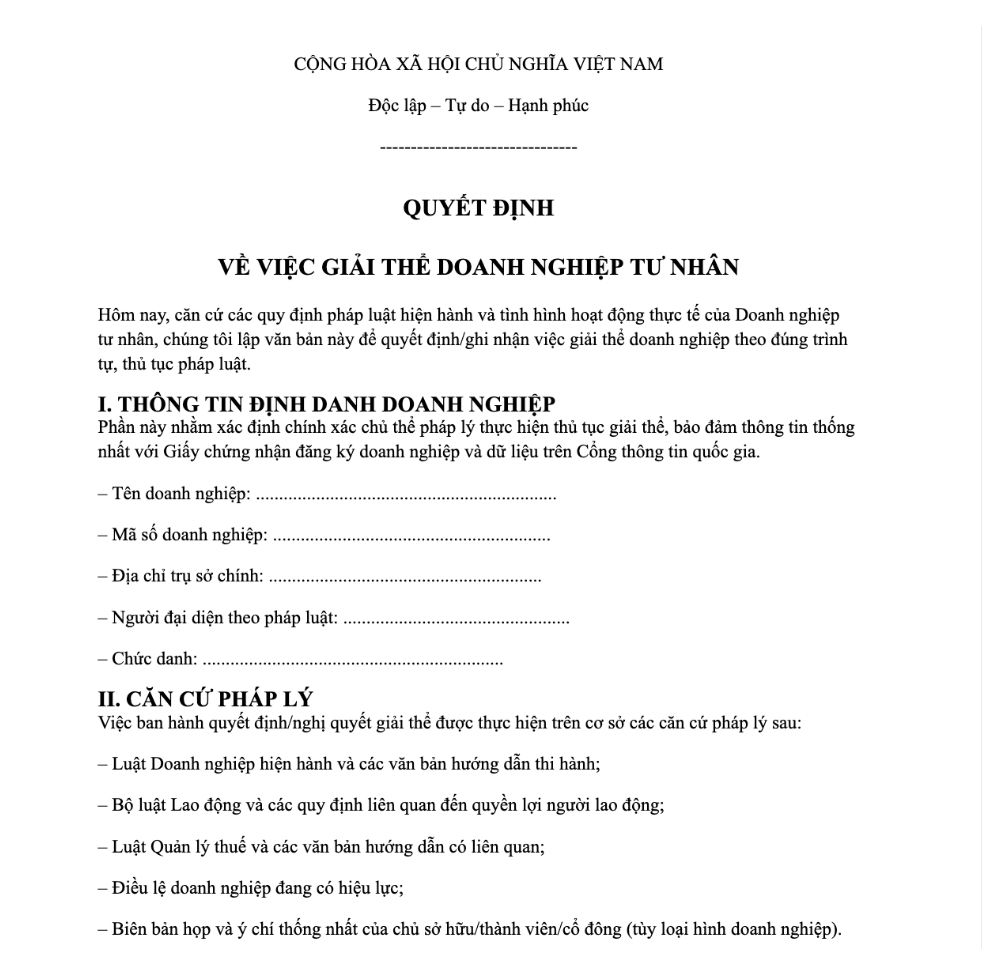

4. Enterprise Dissolution Decision Template (Updated 2026)

The enterprise dissolution decision is the most critical legal document in the entire dissolution process. Drafting it correctly, completely, and accurately from the beginning will help the enterprise avoid having its application rejected, shorten processing times, and mitigate future legal risks.

4.1. The Importance of the Enterprise Dissolution Decision Template

The dissolution decision (or resolution) serves to:

- Serve as the initial legal document for the entire dissolution process

From the moment the dissolution decision is issued, the enterprise officially enters the phase of ceasing operations and has many of its business rights restricted.

- Provide the basis for state agencies to process the application

The Tax Authority, the Business Registration Office (Department of Planning & Investment), and other relevant agencies rely on this decision to:

- Accept the dissolution application

- Conduct tax obligation audits

- Update the enterprise’s legal status

- Form the basis for settling the rights of employees and creditors

The content of the dissolution decision clearly outlines the enterprise’s responsibility for debt payment and handling labor contracts.

4.2. Mandatory Content in the Dissolution Decision Template

According to legal regulations and practical application processing, a valid dissolution decision must include all of the following content:

Enterprise Identification Information

- Enterprise name (exactly as on the Certificate of Business Registration)

- Enterprise code

Head office address

Legal Basis

- Based on the current Law on Enterprises

Based on the company’s charter - Based on the meeting minutes (if any)

Reason for Dissolution

- State clearly, specifically, and in accordance with the actual situation

Avoid general, vague reasons that may cause difficulties when state agencies review the application

Deadline and Plan for Debt Payment

- Debt payment deadline (not exceeding the period permitted by law)

- Plan for handling assets and liabilities

- Commitment to have paid or to pay all financial obligations in full

Plan for Settling Employee Benefits

- Termination of labor contracts

- Payment of salaries and allowances

- Fulfillment of social insurance and health insurance obligations

- Owner / Chairman of the Members’ Council / Chairman of the Board of Directors or the legal representative

Sign with the correct title as per the company’s charter

4.3. Free Download: Enterprise Dissolution Decision Template (Ready to Use)

5. Detailed A–Z Process and Procedures for Business Dissolution

The business dissolution process is carried out in a strict sequence, directly involving many state management agencies. Businesses need to follow the correct order to avoid having their applications returned or prolonging the processing time.

5.1. Step 1: Issue the Dissolution Decision and Notification

First, the business must hold a meeting and pass a dissolution decision (or resolution) in accordance with the authority stipulated in the company’s charter:

- The owner (for a single-member LLC)

- The Members’ Council (for a multi-member LLC with two or more members)

- The General Meeting of Shareholders (for a joint stock company)

After the dissolution decision is issued, the business is responsible for:

- Sending the Dissolution Notification and Dissolution Decision to:

- The Business Registration Office (Department of Planning & Investment)

- The direct tax management authority

- Employees within the business

- Creditors and relevant partners

- The Business Registration Office (Department of Planning & Investment)

- Publishing the dissolution information on the National Business Registration Portal as required

5.2. Step 2: Liquidate Assets and Settle Debts

The business proceeds to liquidate all remaining assets to fulfill its financial obligations. If necessary, the business can establish an Asset Liquidation Council according to the dissolution decision.

The payment of debts must comply with the order of priority according to the Law on Enterprises, specifically:

- Salaries, severance pay, social insurance, health insurance, and other benefits for employees

- Taxes and financial obligations to the State

- Other debts (debts to partners, suppliers, credit institutions, etc.)

The business can only complete the dissolution process after all debts have been fully paid.

This is usually the most time-consuming step in the dissolution process. The business needs to perform the following:

- Submit a written request to terminate the tax code’s validity (Form 24-DK-TCT)

- Perform tax finalization: Corporate income tax (CIT) / Personal income tax (PIT) / Other arising taxes (if any)

- Complete the submission of any outstanding tax declarations

- Request confirmation of no tax debt and no customs obligations (if the business has import/export activities)

- Return the seal and the Seal Sample Registration Certificate (applicable to businesses using seals issued by the police authority)

Only when the tax authority confirms that the business has fulfilled its tax obligations can the business proceed to the next step.

5.4. Step 4: Submit the Dissolution Dossier at the Department of Planning and Investment

After completing tax obligations, the business submits the dissolution dossier to the Business Registration Office – Department of Planning and Investment where the business is headquartered.

Submission methods:

- Submit online via the National Portal

- Or submit in person (depending on the locality)

The business needs to:

- Track the dossier processing status

Promptly supplement or amend the dossier if requested by the business registration authority

5.5. Step 5: Update the Status to “Dissolved”

When the dossier is valid:

- The Business Registration Office will update the business’s legal status to “Dissolved”

- The information is published on the National Business Registration Portal

From this point on, the business’s legal entity status is officially terminated.

6. Detailed Sample Business Dissolution Dossier

The dossier for terminating the tax code’s validity includes:

- Written request to terminate the tax code’s validity (Form 24-DK-TCT)

- Meeting minutes and the Decision/Resolution on dissolution

- Power of attorney for the person carrying out the procedure (if not the legal representative)

- Written confirmation of no tax debt and no customs debt (if any)

6.2. Dossier to be Submitted to the Department of Planning and Investment

The business dissolution dossier includes:

- Notice of business dissolution

- Dissolution decision and corresponding meeting minutes

- Report on the liquidation of business assets

- List of employees and their resolved benefits

- List of creditors and debts that have been paid

- Confirmation of seal return (if any)

- Power of attorney (if the dossier is submitted by an authorized person)

7. Special Cases and Important Notes When Dissolving a Business

In reality, not all businesses dissolve under “ideal” conditions. For some specific cases, not fully understanding the regulations can easily lead to complications with taxes, dossiers, or extended legal liabilities after dissolution.

7.1. Dissolving a Business That Has Not Generated Revenue

A business is considered to have not generated revenue when:

- It has not issued invoices for selling goods or providing services

- It has not recorded revenue in its accounting books

- It may have registered for tax but has not actually operated

Procedural characteristics:

- The dissolution process is often simpler as no output invoices are generated

- No need to handle invoice cancellation or revenue adjustments

However, the business is still required to:

- Perform a full tax finalization in accordance with regulations

- Submit any missing tax declarations (including “no activity” declarations)

- Complete the application to terminate the tax identification number

7.2. Dissolution of Branches, Representative Offices, and Business Locations

If the business has:

- Branches

- Representative offices

- Business locations

It is mandatory to dissolve these dependent units first, in accordance with legal procedures.

Handling principles:

- Dissolve each dependent unit at its place of registered operation

- Fulfill the tax, seal, and labor obligations of each unit

- Only after all dependent units have been validly dissolved can the business proceed with the dissolution of the parent company. Note: If even one dependent unit has not been dissolved, the business dissolution application will not be accepted.

7.3. Prohibited Activities from the Date of the Dissolution Decision

From the moment the business issues a decision (or resolution) for dissolution, its business activities are strictly restricted. Specifically, it is not allowed to:

- Raise capital in any form

- Sign new business contracts

- Incur new financial obligations

- Expand operations or hire additional employees

The business is only allowed to perform activities aimed at:

- Liquidating assets

- Collecting debts

- Fulfilling obligations to the State, employees, and creditors

Violating these regulations can lead to legal liability for the business’s managers.

7.4. Responsibilities of Business Managers During Dissolution

Business managers (owners, members of the Members’ Council, Board of Directors, directors, etc.) are responsible for:

- Ensuring the truthfulness and accuracy of the entire dissolution file

- Bearing joint responsibility for any errors, fraud, or concealment of financial obligations

- Cooperating fully with tax authorities and business registration agencies

Responsibility is particularly strict in cases where:

- The business’s Certificate of Business Registration is revoked

- There are signs of tax evasion, asset dissipation, or absconding from obligations

In these cases, managers may face civil, administrative, or even criminal liability for serious violations.

8. Common Mistakes and Practical Experience

8.1. Common Mistakes in Business Dissolution

In practice, many businesses experience prolonged dissolution times due to the following errors:

- Drafting a dissolution decision that lacks mandatory content or is not issued by the proper authority

- Incomplete tax finalization, missing tax declarations, or outstanding tax debts

- Liquidating assets without following the priority order stipulated by law

- Submitting applications that are not in the correct format, have missing documents, or contain inconsistent information

8.2. Practical Experience for a Smooth Dissolution

To ensure the dissolution process is quick and legally compliant, businesses should:

- Review all financial, tax, and labor obligations before starting

- Prepare a complete, consistent, and correctly formatted set of documents

- Proactively monitor the processing progress with the tax authority and the Department of Planning & Investment

- Seek professional legal and accounting advice for complex cases or when encountering difficulties

9. Frequently Asked Questions (FAQs)

How long does it take to complete the business dissolution procedure?

Typically, the time to complete the business dissolution procedure ranges from 30 to 90 days, depending on the tax status, issuance of invoices, debts, and the completeness and accuracy of the documents. The processing time at the tax authority usually accounts for the largest part of the dissolution timeline.

Does the dissolution decision need to be notarized or authenticated?

According to current regulations, the decision or resolution for business dissolution does not require notarization or authentication, as long as the document is issued by the proper authority, has all valid signatures, and its content complies with legal provisions.

How is a business with multiple branches dissolved?

If a business has branches, representative offices, or business locations, it must first dissolve all dependent units, complete the tax and labor obligations for each unit, and only then can it proceed with the dissolution procedure for the parent company.

Can the dissolution decision be canceled?

A business can cancel or suspend the dissolution decision if the complete dissolution application has not yet been submitted and the Department of Planning & Investment has not updated the status to “Dissolved”. Once this status is recorded, the dissolution decision can no longer be canceled.

What benefits are employees entitled to when a business is dissolved

When a business is dissolved, employees are given priority for payment of outstanding wages, severance or job loss allowances, social insurance, health insurance, unemployment insurance, and other benefits as stipulated in their labor contracts and by law.