Cash Count Report Template according to Circular 133 and 107

A cash fund count minutes is a document that records the results of checking the quantity and value of cash on hand in an organization’s or business’s fund. The main objective of the minutes is to ensure accuracy and reconciliation between the cash balance in the books and the actual cash amount. Let’s explore with 1Office the important considerations when conducting a count and download 03 free standard cash fund count minutes templates according to Circulars 107 and 133.

Mục lục

Cases requiring the use of cash fund count minutes

When conducting financial transactions, there are many cases that require the creation of cash fund count minutes. Below are the most common situations you may encounter.

1. At the end of an accounting period

At the end of each accounting period, checking and re-evaluating the cash fund is extremely necessary for reconciliation and preparing financial statements. This helps determine whether the reported figures match the actual amounts.

Creating cash fund count minutes at this time helps to detect errors in the recording and accounting process early. If there is a discrepancy between the actual data and the report, the business can make timely adjustments to ensure accuracy.

2. When there is a change in the fund manager or responsible employee

Personnel changes, especially for those who directly manage the cash fund, are also an important situation for conducting a count. When an employee resigns or transfers, creating count minutes will help the business review the entire cash fund and confirm the responsibilities of each individual.

This is also an appropriate time to ensure that all transactions have been recorded and no shortages have occurred. This helps the business avoid future risks.

3. When there is suspicion of fraud or discovery of discrepancies

When there are any signs that suggest possible fraud or financial manipulation, a cash fund count must be conducted immediately. This situation requires more seriousness and caution than ever before.

Creating count minutes will not only help determine the fund’s status but also create clear evidence to handle any issues that arise later. Therefore, a detailed and accurate execution is essential.

Common errors when using cash fund count minutes

Although creating cash fund count minutes is very important, in practice, many errors still occur. Below are some common mistakes that businesses often make.

- Discrepancy between the books and actual figures: This discrepancy often occurs when comparing the actual cash in the fund with the balance recorded in the accounting books. The main causes are incomplete or incorrect recording during cash deposits and withdrawals, failure to promptly update transactions, or confusion in classifying revenue and expenditure items. This is common when the transaction volume is large or the inspection process is not strictly implemented.

- Lack of detail in the minutes: Common errors include omitting important information such as the date, specific figures, confirmation signatures, or not clearly stating the reason for any discrepancies. The cause is often a lack of care or not using a standard minutes template, leading to errors in information recording.

- Lack of full participation from relevant parties: This error occurs when the participation of representatives from relevant departments such as accounting, the cashier, or the control board is not ensured, or the inventory committee is not properly established according to regulations. The main cause is subjectivity or a lack of understanding of the regulatory requirements for the count.

- Errors in identifying and handling discrepancies: This error often appears when summarizing the count results and handling discrepancies. Common mistakes include not clearly analyzing the cause of the discrepancy, errors in adjusting the books, or inappropriate disciplinary actions.

Standard Cash Fund Count Process

A cash fund count is a mandatory activity in every business to ensure the transparency and accuracy of cash flow and compliance with accounting regulations. A standard process is typically implemented in the 4 main steps below:

1. Prepare for the fund count

Before proceeding, the business needs to fully prepare personnel and documents:

-

Establish a count committee including: the cashier, chief accountant (or accountant in charge of the fund), and a management representative.

-

Seal the cash box to ensure no transactions occur during the count.

-

Prepare documents: cash fund ledger, receipt and payment vouchers, list of supporting documents.

-

Notify relevant parties of the time to ensure full attendance.

The goal of this step is to create transparency and an accurate foundation for the count process.

2. Conducting the cash count

When starting the count, the inventory committee performs the following:

-

Physical cash count: count each denomination in detail and create a clear breakdown.

-

Data reconciliation: compare the actual balance with the balance in the cash book and accounting system.

-

Identify discrepancies: if there are differences, clarify the cause (incorrect recording, not updated, or signs of loss).

3. Preparing the cash count report

After completing the count and reconciliation, the business needs to prepare a cash count report. This report is a mandatory document and includes the following main contents:

-

Time and location of the count.

-

Members of the inventory committee.

-

Book balance, actual balance, and discrepancy (if any).

-

Conclusion and proposed actions.

-

Full signatures of the cashier, accountant, inventory committee, and management representative.

This is an important legal basis and must be stored carefully according to accounting law regulations.

4. Post-count procedures

Finally, the business needs to implement the following post-count steps:

-

Report the count results to management.

-

Adjust the books if there are data discrepancies.

-

Determine responsibility and handle related individuals in case of loss.

-

Record keeping: reports and inventory documents must be fully retained (for a minimum of 5–10 years).

Following the correct cash fund inventory process not only helps businesses manage cash flow effectively but also protects their reputation and ensures legal compliance.

03 Standard Cash Fund Inventory Report Templates according to Circular 107

Cash fund inventory is a crucial part of a business’s financial management, helping to ensure the actual balance matches the accounting records and to promptly detect errors or losses. According to Circular 107/2017/TT-BTC, preparing an inventory report must follow a standard template to ensure legality and transparency. Below are 03 commonly used cash fund inventory report templates in businesses:

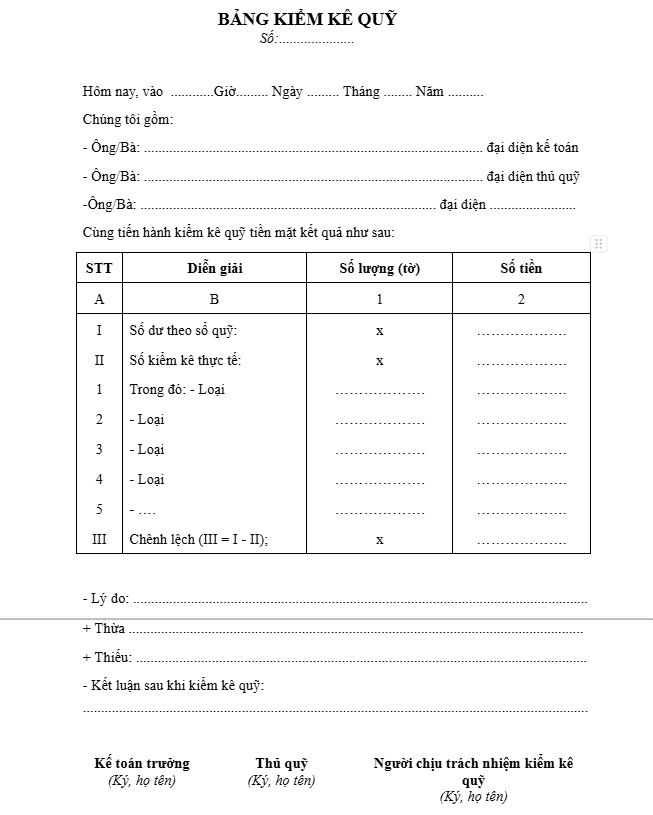

Cash Fund Inventory Report according to Circular 133

Free Download: Cash Fund Inventory Report according to Circular 133

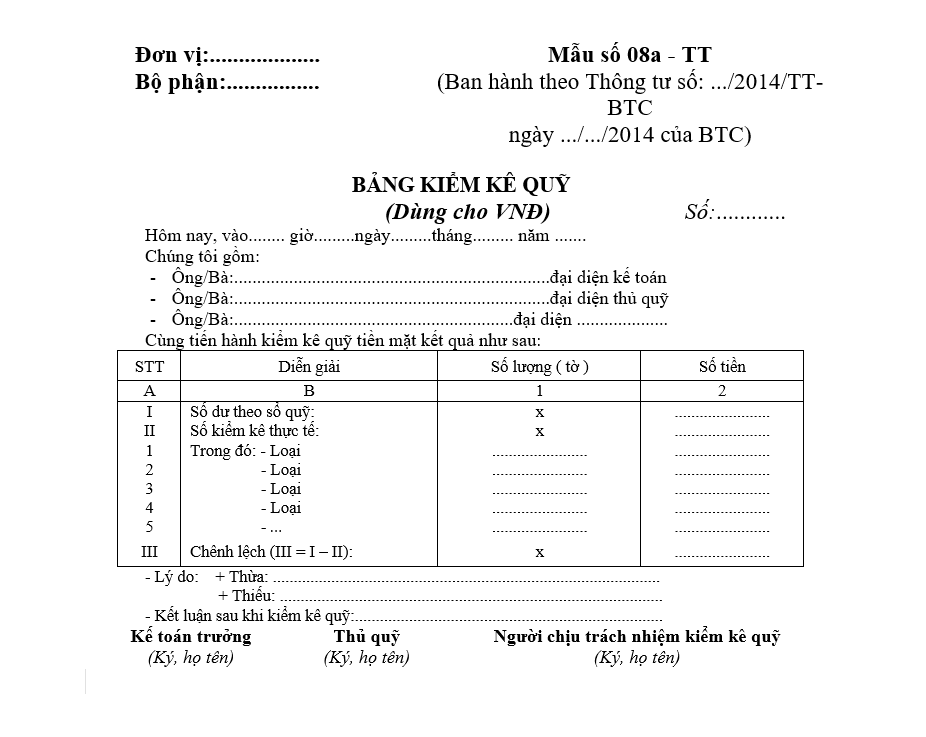

Cash Fund Inventory Report Template according to Circular 107 (for VND)

Cash Fund Inventory Report Template according to Circular 200 (for foreign currency, gold, etc.)

<img class="alignnone size-full wp-image-48348" src="https://1office.vn/wp-content/uploads/2024/12/Mau-bien-ban-kiem-ke-quyAfter creating the report, record-keeping is also very important. You need to store the inventory report along with related documents and vouchers to create a complete file.

This not only facilitates future inspections but also serves as a basis for financial audits.

Periodic Inventory Schedule

Reports shouldn’t only be created when an incident occurs; conducting periodic cash fund inventory reports is also a good practice. There should be a clear inventory schedule to ensure everything is always tightly managed.

Conducting periodic inventories will help promptly detect errors or irregularities in cash fund management.

————————————

Creating a cash fund inventory report is an indispensable task in corporate financial management. Through standard report templates according to Circulars 107 and 133, as well as important notes during the inventory process, we hope that businesses will gain a clearer view of their cash funds.