Is an Advance an Asset or a Liability? A Detailed Explanation for Businesses

Cash advances are a very common transaction in business but are often misclassified in accounting. If you’re wondering whether a cash advance is an asset or a source of capital, this article will help you understand its true nature and how to view it correctly.

Mục lục

- What is a Cash Advance?

- The Role of Cash Advances for Businesses

- Distinguishing Between Assets and Sources of Capital – The Foundation for Understanding Cash Advances

- Is a Cash Advance an Asset or a Source of Capital? A Detailed Explanation

- The Advance Management Process in a Real Business

- How to Account for Advances? A Detailed Guide

- Common Mistakes in Advance Management and How to Avoid Them

- FAQ – Frequently Asked Questions about Advances

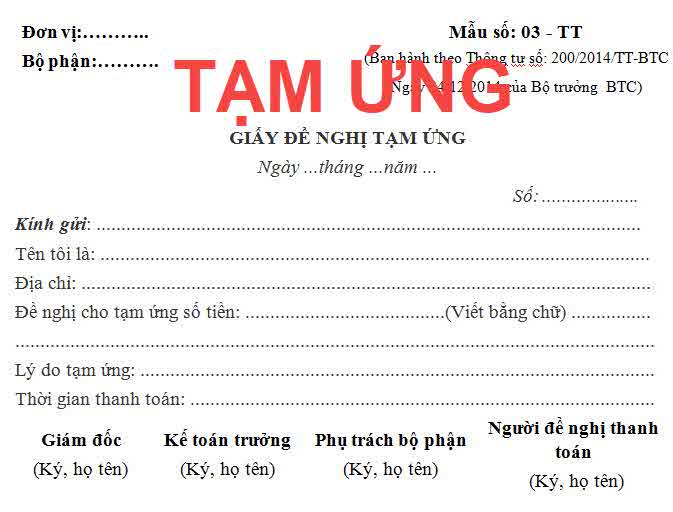

What is a Cash Advance?

A cash advance is an amount of money or supplies that a business temporarily disburses to an employee or partner to perform required tasks or duties. The recipient of the advance is responsible for using it for the intended purpose and settling the full amount after completing the work.

In business practice, cash advances are typically used for:

- Business trip and travel expenses

- Purchasing office supplies and materials

- Payments to suppliers

- Event organization costs

- Salary or bonus advances

Real-world example: Company A sends an employee on a business trip to Da Nang. Before the trip, the accountant gives the employee a cash advance of 10 million VND. Upon return, the employee settles the actual expenses (airfare, hotel, meals) with the accountant, returning any surplus amount or receiving more if there was a shortfall.

The Role of Cash Advances for Businesses

Before answering the question of whether a cash advance is an asset or a source of capital, you need to understand that properly managing cash advances brings many practical benefits to a business:

- Effective cash flow control:

- Clearly track cash usage

- Prevent loss and waste of assets

- Forecast capital needs more accurately

- Transparency in financial management:

- Easy reconciliation and verification

- Facilitates audits and tax finalization

- Minimizes the risk of fraud

- Optimization of internal processes:

- Reduces document processing time

- Enhances employee accountability

- Improves management efficiency

According to a survey of 50 small and medium-sized enterprises in Vietnam, businesses with a standardized cash advance management process reduced unnecessary expenses by 15-20% and saved an average of 8-10 working hours per week for the accounting department.

Distinguishing Between Assets and Sources of Capital – The Foundation for Understanding Cash Advances

To fully understand cash advances, you need to grasp two fundamental accounting concepts: assets and sources of capital.

Assets are economic resources owned by the business that can be measured in monetary terms and are expected to provide future benefits. Assets include:

- Current assets: cash, bank deposits, inventory, accounts receivable…

- Long-term assets: factories, machinery, equipment, copyrights…

Sources of Capital are the sources that finance the assets, indicating where the business’s assets come from. Sources of capital include:

- Liabilities: loans, accounts payable, salaries payable…

- Owner’s Equity: contributed capital, retained earnings…

The accounting equation is always: Assets = Sources of Capital

Is a Cash Advance an Asset or a Source of Capital? A Detailed Explanation

In accounting, a cash advance is classified as an asset of the business, specifically a current asset, not a source of capital. Why is that?

When a business gives a cash advance to an employee, it is essentially “lending” an asset (money) to the employee to perform their work. The employee is obligated to settle the advance and return any unused portion. This is an internal receivable, recorded in account 141 – “Advances to Employees” according to Vietnamese accounting standards.

A simple way to distinguish:

- Cash advance increases → Assets increase

- Settling a cash advance → Assets (the advance) decrease, converting into another asset or an expense

In business practice, understanding that advances are assets helps accountants record them correctly, avoiding confusion with liabilities or expenses.

The Advance Management Process in a Real Business

A standard advance management process in a business typically consists of 3 main steps:

Step 1: Create an Advance Request

The process begins when an employee needs to use money for work. The advance request form should include:

- Requester’s information

- Advance amount

- Purpose of use

- Expected settlement date

- Requester’s signature

Note: Businesses should create a standard form and clearly define the deadline for submitting advance requests (usually 1-3 days in advance) to give the accounting department time to prepare.

Step 2: Approve and Disburse Funds/Supplies

After receiving the advance request, the approval process is typically as follows:

- The department head confirms the reasonableness of the request

- The accountant checks the budget and the status of previous advances

- The director/authorized person approves

- The accountant disburses the funds and records the transaction

Many businesses have a policy of not issuing further advances if an employee has an outstanding unsettled advance, except in special cases approved by management.

Step 3: Settle the Advance

This is the most important step in advance management:

- The advance recipient submits original documents (invoices, receipts…)

- The accountant verifies the validity of the documents

- Prepare a settlement statement comparing the advance amount and actual expenses

- Handle discrepancies:

- Spent more than the advance: The accountant disburses the additional amount

- Spent less than the advance: The recipient returns the excess cash

The settlement deadline is usually 3-7 days after the work is completed. Businesses should set up an alert system for when employees are late with their settlements.

How to Account for Advances? A Detailed Guide

Accounting for advances must comply with accounting standards and be carried out according to regulations. Below is a detailed guide:

When disbursing an advance:

Debit Acct 141 – Advances xx

Credit Acct 111/112 – Cash/Cash in bank xx

When settling an advance:

a) Case of spending for the intended purpose (purchasing goods, paying for services…):

Debit Acct 152/153/156/641/642… (depending on the purpose of expenditure) xx

Credit Acct 141 – Advances xx

b) Case of returning excess cash:

Debit Acct 111/112 – Cash/Cash in bank xx

Credit Acct 141 – Advances xx

c) Case of spending more than the advance:

Debit Acct 152/153/156/641/642… (depending on the purpose of expenditure) xx

Credit Acct 141 – Advances xx

Credit Acct 111/112 – Cash/Cash in bank xx

Practical example: A company gives employee A an advance of 5 million VND to buy office supplies. After the purchase, the total actual cost is 4.8 million VND. The accounting entries are:

When advancing:

Debit Acct 141 5,000,000

Credit Acct 111 5,000,000

When settling:

Debit Acct 642 4,800,000

Credit Acct 141 4,800,000

When receiving the excess cash back:

Debit Acct 111 200,000

Credit Acct 141 200,000

Common Mistakes in Advance Management and How to Avoid Them

Mistake 1: Not Requiring Settlement

This is the most serious mistake in advance management. Many businesses neglect to urge employees to settle their advances, leading to:

- Loss of control over the purpose of use

- A large outstanding balance of advances

- Difficulties during reconciliation and auditing

- It may be considered employee income, subject to Personal Income Tax (PIT)

A real business case: A manufacturing company in Hanoi had over 500 million VND in unsettled advances for 2 years, causing difficulties during tax finalization and audits.

Mistake 2: Incorrectly recording advances as capital sources

Many new accountants often make mistakes when booking advances, treating them as accounts payable (part of capital sources) instead of accounts receivable (part of assets). This leads to:

- Inaccurate financial statements

- Incorrect financial ratios

- Errors in tax finalization

How to avoid mistakes in advance management

- Establish a strict process:

- Clearly define the settlement deadline (usually 3-7 days)

- Set up an alert system for overdue advances

- Do not issue new advances until old ones are settled

- Strictly control supporting documents:

- Require valid original invoices and documents

- Check the reasonableness of expenses

- Compare against spending limits (if any)

- Apply technology:

- Use accounting software to manage advances

- Automate settlement reminders

- Generate periodic reports on the status of advances

Many modern businesses have adopted software like 1Care and 1Office to automate the advance management process, helping to reduce processing time by 70% and nearly eliminate errors entirely.

FAQ – Frequently Asked Questions about Advances

Is an advance an expense?

No. An advance is not an expense but an internal receivable (an asset). Only when the advance is settled with valid supporting documents is the amount recognized as an expense, depending on its purpose.

Real-world example: When an employee receives a 10 million VND advance for a business trip, this amount is only recognized as a travel expense after the employee settles it with valid invoices and documents.

What happens if an advance is not settled?

If an employee does not settle an advance by the specified deadline, the company can:

- Send reminders and request immediate settlement (standard procedure)

- Deduct from salary or other payables (requires an internal policy)

- Take disciplinary action according to company regulations

- In special cases (employee resignation, inability to repay), the advance may be treated as employee income and subject to Personal Income Tax (PIT) as regulated.

Do small businesses need to manage advances?

Absolutely essential. In reality, small businesses are often more significantly impacted by poor advance management because:

- Limited financial resources

- Staff often have multiple roles, leading to oversights

- Incomplete internal control systems

Advice for small businesses:

- Establish a simple yet strict process

- Use simple tools (Excel) or basic accounting software

- Train employees on the importance of advance management

—————————–

Effective advance management is not just a simple accounting issue but a crucial part of corporate governance. Understanding that an advance is an asset, not a capital source or an expense, combined with a strict management process, will help businesses better control cash flow, ensure financial transparency, and optimize operational efficiency.