What is KYC? Benefits, risks, and how to perform KYC for beginners

KYC is a familiar process in banking, fintech, exchanges, and many digital financial activities, but not everyone fully understands what KYC is and why it is important. If you want to quickly grasp the concept, identity verification process, benefits, and risks of non-compliance, this article will help you understand it from start to finish.

Mục lục

- What is KYC?

- The role of KYC in identity verification and identification

- Who needs to perform the KYC process?

- The KYC process for beginners

- Benefits of KYC in payment management

- Risks of non-compliance with KYC regulations

- KYC regulations and standards in Vietnam

- Real-world Examples of KYC in Vietnamese Businesses

- Frequently Asked Questions about KYC

- 1. Is KYC mandatory for all businesses?

- 2. What is the cost of implementing a KYC system?

- 3. Should we develop a KYC system in-house or use a ready-made solution?

- 4. How can we balance user experience with KYC compliance?

- 5. How can we update customer KYC information?

- 6. Is KYC suitable for small startups?

What is KYC?

KYC (Know Your Customer) is a customer identity verification process used by financial institutions, exchanges, and businesses to identify and authenticate customers’ personal information.

This process is designed to prevent fraudulent activities, money laundering, terrorist financing, and other illegal financial activities.

The KYC process typically involves collecting, verifying, and evaluating a customer’s personal information such as name, address, date of birth, phone number, and email, and in many cases, requires providing identification documents like a national ID card, passport, or driver’s license.

What is KYC in investing?

In the investment sector, KYC is a mandatory process when customers open accounts at securities firms, investment funds, or online investment platforms. This process helps investment organizations:

- Better understand the customer’s financial profile and investment goals

- Assess the customer’s risk tolerance and level of investment knowledge

- Recommend suitable investment products based on KYC information

- Ensure compliance with legal regulations on anti-money laundering and counter-terrorist financing

What is KYC on exchanges?

For cryptocurrency, foreign exchange, or other asset exchanges, KYC is a mandatory process aimed at:

- Verifying user identity before allowing them to conduct transactions

- Establishing transaction limits based on the level of KYC verification

- Monitoring suspicious transactions and reporting them to the authorities

- Protecting users from fraudulent activities and ensuring transparency on the exchange

Many exchanges apply different KYC levels, with each level allowing users to perform transactions with different limits. For example, KYC level 1 may allow low-value transactions, while KYC level 2 or 3 will require additional verification documents and permit higher-value transactions.

The role of KYC in identity verification and identification

The KYC process plays a crucial role in ensuring transparency and security in financial activities. Here are the main roles of KYC:

Verifying customer information

KYC helps financial institutions and businesses verify the identity of their customers, ensuring they are dealing with real individuals with clear identities. This helps prevent cases of identity theft and fraud.

The customer information verification process often includes cross-referencing personal information with identification documents, verifying addresses through utility bills, and in some cases, may require biometric verification such as facial recognition.

Through the KYC process, organizations can assess the level of risk associated with each customer. This includes determining whether a customer is at high risk for money laundering, terrorist financing, or is involved in other illegal activities.

Risk assessment is often based on various factors such as nationality, occupation, source of income, transaction purpose, and the customer’s transaction history. Based on the assessment results, organizations will apply appropriate monitoring measures for each customer.

Increasing security in transactions

KYC helps enhance security in financial transactions by:

- Preventing suspicious and unusual transactions

- Minimizing the risk of fraud and scams

- Protecting customer assets from criminal activities

- Creating a safe and trustworthy transaction environment

Who needs to perform the KYC process?

The KYC process applies to many different entities, including:

- Financial institutions: Banks, securities companies, insurance companies, investment funds

- Exchanges: Cryptocurrency, foreign exchange, and stock exchanges

- Fintech companies: E-wallets, online payment platforms, financial applications

- Businesses with financial transaction activities: Real estate, precious metals, and gemstone businesses

- Startups: Especially startups in the finance, payment, and investment sectors

For CEOs, business owners, and especially those building startups, understanding and complying with KYC regulations is crucial to ensure the business operates legally and builds trust with customers from the very beginning.

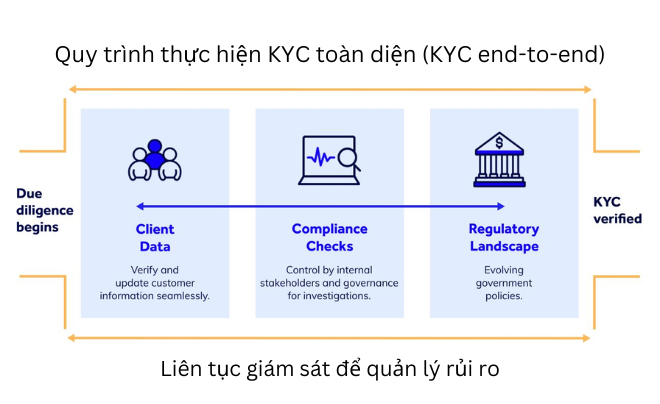

The KYC process for beginners

The KYC process in the financial sector typically includes the following steps:

- Collect basic information: Including the customer’s name, date of birth, address, phone number, email, and other personal information.

- Verify identity: Request customers to provide identification documents such as National ID/Citizen ID, passport, or driver’s license to verify their identity.

- Verify address: Through utility bills (electricity, water, phone) or other documents that can verify the customer’s residential address.

- Biometric verification (optional): Some organizations require biometric verification such as facial recognition or fingerprints to enhance security.

- Check customer information: Cross-reference the provided information with blacklists, sanction lists, and lists of high-risk individuals.

- Assess risk: Classify customers based on their risk level and apply appropriate monitoring measures.

- Continuous monitoring: Monitor customer activities and update information periodically to ensure the accuracy and currency of KYC data.

Depending on the specific sector, the KYC process may be adjusted and supplemented with specific steps. For example, in the banking sector, KYC is often accompanied by AML (Anti-Money Laundering) and CDD (Customer Due Diligence) processes.

Benefits of KYC in payment management

Implementing KYC brings significant benefits to financial institutions and businesses:

Prevent and minimize fraud

KYC helps prevent and minimize fraudulent activities by:

- Verifying the identity of customers before allowing them to perform transactions

- Detecting suspicious and unusual transaction patterns

- Preventing cases of identity theft and account hijacking

- Protecting customers from financial crime activities

Compliance with regulations and legal obligations

Implementing KYC helps organizations comply with legal regulations regarding:

- Anti-Money Laundering (AML)

- Countering Financing of Terrorism (CFT)

- Personal data protection (such as GDPR in Europe)

- Other legal regulations related to financial activities

Complying with these regulations not only helps avoid fines and legal penalties but also enhances the organization’s reputation and image.

Manage and mitigate risk

KYC helps organizations manage and mitigate risk by:

- Assessing the risk level of each customer

- Classifying customers based on their risk profiles

- Applying appropriate monitoring measures for each customer group

- Detecting early signs of risk and taking timely preventive measures

Building customer trust

Implementing KYC transparently and professionally helps build customer trust by:

- Demonstrating that the organization values customer protection and legal compliance

- Creating a safe and reliable transaction environment

- Strictly protecting customers’ personal information

- Building long-term relationships based on trust and transparency

Reducing operational costs

Although implementing KYC requires an initial investment, in the long run, it helps reduce operational costs by:

- Minimizing cases of fraud and scams

- Optimizing transaction processing workflows

- Reducing costs for handling legal issues and disputes

- Automating identity verification processes through technology

For startups, building an effective KYC system from the beginning can help save time and costs in the future as operations scale.

Risks of non-compliance with KYC regulations

Failure to comply with KYC regulations can lead to many serious consequences:

- Fines and legal penalties: Organizations that violate KYC regulations may face large fines from regulatory authorities. These fines can amount to millions of dollars depending on the severity of the violation and the country.

- Damage to reputation and brand: Violating KYC regulations and being publicly penalized can seriously damage a company’s reputation and brand, leading to a loss of trust from customers and partners.

- Increased risk of fraud and money laundering: Improperly implementing KYC increases the risk of the business becoming a target for fraud, money laundering, and terrorist financing activities.

- Loss of business opportunities: Many major partners and customers will only work with businesses that strictly comply with KYC regulations. Non-compliance can lead to the loss of important business opportunities.

- Difficulties in market expansion: Non-compliance with KYC can create difficulties when a business wants to expand its operations into new markets, especially those with strict KYC regulations.

- Personal legal risks: In many cases, executives and business leaders can be held personally responsible for non-compliance with KYC regulations, leading to administrative or even criminal penalties.

For startups and CEOs, understanding and complying with KYC regulations from the outset is crucial to avoid unnecessary risks and build a solid foundation for the company’s sustainable growth.

KYC regulations and standards in Vietnam

In Vietnam, the KYC (Know Your Customer) process is strictly regulated in many legal documents, especially in the banking, securities, insurance, and fintech sectors. The main objectives are to prevent money laundering, financial fraud, and protect personal data.

Some important regulations and standards:

-

Law on Anti-Money Laundering 2022:

This is the foundational legal framework requiring financial institutions, banks, insurance companies, etc., to verify customer identity before establishing a business relationship or conducting large transactions. -

Decree 13/2023/ND-CP on Personal Data Protection:

This clearly defines the responsibilities of businesses when collecting, processing, and storing personal information during the KYC process. Businesses must obtain explicit user consent and apply appropriate security measures to prevent data leakage. -

Circular 09/2023/TT-NHNN guiding eKYC in the banking sector:

This allows banks and credit institutions to perform electronic customer identification (eKYC) without a face-to-face meeting, provided they comply with the identification and data storage procedures stipulated by the State Bank of Vietnam. -

eIDAS and ISO/IEC 27001 Standards:

Some technology companies in Vietnam also apply these international standards to ensure the security, integrity, and safety of information when implementing eKYC systems.

Overall, the KYC legal framework in Vietnam is continuously being improved, creating favorable conditions for digital transformation in the financial sector while ensuring compliance and consumer protection.

Real-world Examples of KYC in Vietnamese Businesses

Currently, many organizations in Vietnam have successfully implemented KYC and eKYC, helping to accelerate customer identification, reduce operational costs, and mitigate fraud.

Some notable examples:

-

TPBank and MB Bank:

These are pioneering banks in implementing fully online eKYC verification, allowing account opening in just a few minutes with an ID card/Citizen ID card and a facial scan.

This helps reduce customer onboarding time by over 60% compared to traditional processes.

See details here

-

Viettel Money and MoMo:

They use AI facial recognition technology and match it with national population data, ensuring accurate and fast verification.

This meets anti-money laundering and financial fraud standards as regulated by the State Bank.

See details here

-

Cryptocurrency Exchanges (e.g., Remitano, Binance):

They require users to undergo multi-level identity verification (Basic – Advanced – Pro), including a facial photo, identity documents, and proof of residential address.

This helps prevent money laundering and illegal anonymous transactions. -

SaaS businesses, fintech companies:

Vietnamese startups like Trusting Social and FiinGroup provide KYC-as-a-Service solutions, allowing other businesses to integrate automated identity verification APIs.

This helps small businesses save costs and easily comply with legal regulations.

Thanks to these applications, KYC is no longer a complex process but has become an essential part of a business’s digitalization journey, ensuring both transaction security and an enhanced customer experience.

Frequently Asked Questions about KYC

1. Is KYC mandatory for all businesses?

Not all businesses are required to perform KYC. However, businesses operating in finance, banking, insurance, securities, cryptocurrency, and those with large financial transactions are often required to comply with KYC regulations according to the laws of each country.

2. What is the cost of implementing a KYC system?

The cost of implementing a KYC system depends on the business’s scale, number of customers, level of automation, and the chosen KYC solution. For small startups, the cost can range from a few thousand to tens of thousands of dollars, while for large organizations, it can reach millions of dollars.

3. Should we develop a KYC system in-house or use a ready-made solution?

Both options have their pros and cons. Developing a KYC system in-house allows for customization to the specific needs of the business but requires significant time, resources, and expertise. Using a ready-made KYC solution saves time and resources but may not perfectly fit the unique requirements of the business.

4. How can we balance user experience with KYC compliance?

To balance user experience with KYC compliance, businesses can:

- Adopt a phased approach, allowing customers to use some basic services with simple KYC and expand services as they complete advanced KYC steps

- Leverage technology to automate and simplify the KYC process (e.g., OCR, biometric verification)

- Design an intuitive and user-friendly KYC process

- Clearly explain why KYC is necessary and how it protects customers

5. How can we update customer KYC information?

Businesses should establish a process for periodically updating KYC information (usually annually or when there are significant changes in customer information). Updates can be done through:

- Automated reminders via email or app

- Requesting information confirmation when customers perform important transactions

- Integrating information updates into the daily service usage process

6. Is KYC suitable for small startups?

Yes, KYC is still suitable for small startups, especially those operating in the finance, payment, and investment sectors. Startups can begin with simple KYC solutions and expand over time. Complying with KYC regulations from the outset will help startups build trust with customers, partners, and investors, while also avoiding future legal issues.

—————————-

KYC is an indispensable part of the operations of financial institutions and is increasingly being applied in many other fields. Especially for CEOs, business owners, and startups, understanding and effectively implementing the KYC process is not just a matter of legal compliance but also an opportunity to build trust with customers and create a solid foundation for the sustainable development of the business.

By implementing KYC effectively, businesses not only protect themselves from legal and financial risks but also contribute to building a transparent, secure, and reliable financial system for all stakeholders.