What is Working Capital Turnover? Significance, Calculation, and Example

Working capital turnover is a crucial indicator that helps businesses assess how efficiently they are using their short-term capital. But what is working capital turnover, how is it calculated, and what should a business do when this ratio is low? This article will help you understand everything from the formula and its meaning to practical ways to improve it.

Mục lục

- 1. What is Working Capital Turnover?

- 2. Formula and Detailed Calculation of Working Capital Turnover

- 3. The Significance of the Working Capital Turnover Ratio

- 4. Example Calculation of the Working Capital Turnover Ratio

- 5. How to Improve the Working Capital Turnover Ratio

- 6. Frequently Asked Questions about Working Capital Turnover

- 7. Conclusion

1. What is Working Capital Turnover?

Working capital turnover (Working Capital Turnover) is a financial ratio used to evaluate the efficiency of a company’s working capital usage. This ratio indicates how much revenue a company generates for every dollar of working capital used over a specific period, typically a year.

Working capital, also known as circulating capital, is the capital used to finance a company’s short-term operations, such as purchasing inventory, paying daily operating expenses, and meeting short-term debt obligations. Working capital is calculated by subtracting short-term liabilities from current assets.

When a business can use its working capital efficiently, it can generate more revenue from the same amount of capital, thereby increasing profits and reducing the need for borrowing. This is why working capital turnover is a ratio of great interest to financial managers and investors.

2. Formula and Detailed Calculation of Working Capital Turnover

2.1. Working Capital Turnover Formula

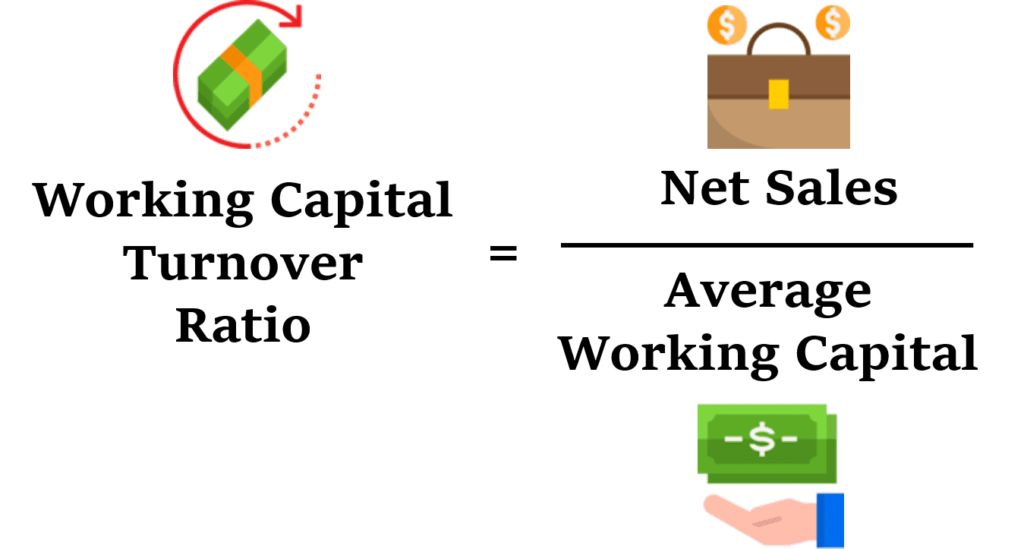

Working capital turnover is calculated using the following formula:

Working Capital Turnover = Net Revenue / Average Working Capital

Where:

- Net Revenue: is the total revenue from the company’s primary business activities after deducting allowances (discounts, sales returns, etc.)

- Average Working Capital: is the average value of working capital during the period, typically calculated as (Beginning Working Capital + Ending Working Capital) / 2

To calculate working capital turnover accurately, you first need to determine the working capital:

Working Capital = Current Assets – Short-term Liabilities

3. The Significance of the Working Capital Turnover Ratio

The working capital turnover is a crucial indicator that reflects the efficiency of a company’s capital usage. This ratio has several important meanings:

3.1. Assessing Capital Utilization Efficiency

A high working capital turnover ratio indicates that the company is using its working capital effectively to generate revenue. This means the company can generate more revenue with the same amount of working capital, or maintain its revenue with less working capital.

3.2. Reflecting Liquidity

This ratio indirectly reflects the company’s liquidity and financial situation. A high working capital turnover ratio often corresponds to good liquidity, as the company can quickly convert short-term assets into cash to meet its debt obligations.

3.3. A Tool for Comparing Operational Efficiency

The working capital turnover is a useful tool for comparing the operational efficiency of different companies within the same industry or for evaluating a company’s efficiency changes over the years.

3.4. Identifying Issues in Capital Management

A low working capital turnover ratio can be a sign of several issues in capital management, such as:

- Excess inventory

- Ineffective accounts receivable collection policies

- Over-investment in short-term assets

- Declining revenue

4. Example Calculation of the Working Capital Turnover Ratio

To better understand how to calculate the working capital turnover, consider the following example of a company that manufactures and distributes electronic devices:

Example: An Electronic Device Distribution Company

ABC Company is a manufacturer and distributor of electronic devices with the following financial information:

Year 2024:

- Net Revenue: 50 billion VND

- Current Assets at the beginning of the year: 15 billion VND

- Current Liabilities at the beginning of the year: 8 billion VND

- Current Assets at the end of the year: 18 billion VND

- Current Liabilities at the end of the year: 10 billion VND

Step 1: Calculate working capital at the beginning and end of the year

- Working capital at the beginning of the year = 15 billion – 8 billion = 7 billion VND

- Working capital at the end of the year = 18 billion – 10 billion = 8 billion VND

Step 2: Calculate average working capital

- Average working capital = (7 billion + 8 billion) / 2 = 7.5 billion VND

Step 3: Calculate the working capital turnover

- Working capital turnover = 50 billion / 7.5 billion = 6.67 times

Result: The working capital turnover for ABC Company in 2024 is 6.67 times. This means that for every dong of working capital, 6.67 dong of revenue was generated during the year.

Analysis: With a working capital turnover ratio of 6.67, ABC Company is using its working capital quite effectively. However, for an accurate assessment, this ratio should be compared with other companies in the industry or with the company’s own results from previous years.

5. How to Improve the Working Capital Turnover Ratio

Improving the working capital turnover ratio can help a business increase its capital efficiency and enhance its financial situation. Here are some effective methods:

5.1. Optimize Inventory Management

- Apply the Just-in-Time (JIT) model: Procure goods just when needed to reduce storage costs

- ABC Analysis: Classify inventory based on importance to focus management efforts

- More Accurate Demand Forecasting: Reduce instances of overstocking or stockouts

- Liquidate Dead Stock: Free up capital tied up in non-standard or obsolete inventory

5.2. Improve Accounts Receivable Management

- Customer Assessment: Check the creditworthiness of customers before extending credit

- Shorten Debt Collection Period: Negotiate more favorable payment terms

- Offer Early Payment Incentives: Provide discounts for payments made before the due date

- Closely Monitor Receivables: Use management software to send reminders and track payments

5.3. Effectively manage accounts payable

- Negotiate longer payment terms: Increase the time cash is held within the business

- Take advantage of payment discounts: Weigh the benefits of early payment against holding onto cash

- Plan payments reasonably: Ensure on-time payments to avoid penalties and maintain good relationships with suppliers

5.4. Increase revenue

- Develop new products: Expand the product portfolio to reach more customer segments

- Improve marketing strategy: Increase brand awareness and attract new customers

- Expand the market: Seek business opportunities in new geographical areas

- Optimize pricing: Adjust selling prices to compete effectively while ensuring profitability

5.5. Reduce operating costs

- Automate processes: Reduce labor costs and increase efficiency

- Renegotiate with suppliers: Seek better prices and terms

- Outsource non-core activities: Focus on core areas of expertise

- Adopt energy-saving technology: Reduce long-term operating costs

6. Frequently Asked Questions about Working Capital Turnover

6.1. Is working capital turnover the same as the current ratio?

No, working capital turnover and the current ratio are two different financial metrics, although both are related to a company’s working capital.

The current ratio is calculated by dividing current assets by current liabilities. This ratio assesses a company’s ability to pay its short-term liabilities with its short-term assets.

- Formula: Current Ratio = Current Assets / Current Liabilities

Working capital turnover measures the efficiency of using working capital to generate revenue. This ratio indicates how much revenue a company generates for every dollar of working capital.

- Formula: Working Capital Turnover = Net Revenue / Average Working Capital

Key difference: The current ratio assesses liquidity, while working capital turnover assesses the efficiency of capital use.

6.2. Is working capital turnover the same as the cash conversion cycle?

No, working capital turnover and the cash conversion cycle (CCC) are two different metrics.

The cash conversion cycle measures the time (in days) it takes to convert investments in inventory and accounts receivable into cash, minus the time delayed in paying suppliers.

- Formula: CCC = Days Inventory Outstanding + Days Sales Outstanding – Days Payable Outstanding

Working capital turnover measures the efficiency of using working capital to generate revenue, expressed as the number of times working capital turns over in a year.

- Key difference: The cash conversion cycle focuses on the time it takes for cash to circulate, while working capital turnover focuses on the efficiency of using capital to generate revenue.

6.3. What is the average working capital turnover ratio?

The average working capital turnover ratio varies depending on the industry and business size. There is no specific number that is considered the “standard” for all businesses.

However, in general:

- Retail industries: Often have a high working capital turnover ratio, potentially from 5-10 times or more, due to the nature of business with fast-moving inventory.

- Manufacturing industries: Usually have a lower ratio, around 2-5 times, as more working capital is needed to maintain the production process.

- Service industries: Can have a high ratio as they typically have little inventory and short payment cycles.

It is important to compare your company’s working capital turnover ratio with other businesses in the same industry and of a similar size, and to monitor this ratio’s trend over the years.

7. Conclusion

Working capital turnover is an important financial ratio that helps assess how efficiently a company uses its working capital. By monitoring and analyzing this ratio, managers can make sound decisions to optimize capital utilization and improve operational efficiency.

Improving the working capital turnover ratio requires a comprehensive strategy, including the effective management of inventory, accounts receivable, and accounts payable, as well as efforts to increase revenue and reduce costs. By achieving an optimal working capital turnover ratio, a business can enhance its competitiveness, improve its financial standing, and create greater value for its stakeholders.