4+ Standard Asset Inventory Report Templates [Latest 2026]

An Asset Inventory Report is used to record the entire asset inventory process of a business. This document has high legal validity and is used as a basis for determining asset value and resolving disputes and claims related to assets. In this article, let’s explore the content, sample templates, and important notes for creating a business asset inventory report with 1Office. Stay tuned!

Mục lục

- 1. What is an Asset Inventory Report?

- 2. When is an Asset Inventory Report needed?

- 3. Basic Contents of an Inventory Report Template

- 4. Asset Inventory Report Templates According to Regulations

- 8. Common Mistakes When Creating an Inventory Report and How to Fix Them

- 9. Vietnam’s Leading Enterprise Asset Management Solution

- 10. Frequently Asked Questions About Asset Inventory Reports

1. What is an Asset Inventory Report?

An Asset Inventory Report is an administrative document created to record, inspect, and reconcile all assets of an individual, organization, or business at a specific point in time. This document reflects the quantity, current status, and actual value of assets, and serves as a basis for comparison with data in the accounting records.

What is an Asset Inventory Report used for?

An Asset Inventory Report is used for several important purposes, including:

- Determining the actual quantity of assets: Including types of assets such as machinery, equipment, tools and supplies, inventory, fixed assets…

- Reconciling with accounting records: To check if the actual figures match the recorded data, thereby identifying discrepancies, shortages, or losses.

- Identifying the cause of asset surpluses or shortages: Helping the business clarify the reasons for discrepancies to find appropriate solutions.

- Recording the condition of assets: Specifically assessing the condition of each asset, such as good working order, damaged, difficult to use, or needing liquidation.

- Serving as a basis for financial and accounting processing: Used for supplementing records, adjusting figures, making accounting entries, and preparing reports for audit or tax authorities.

- Supporting year-end closing or asset handover: Often used at the end of the fiscal year or when there is a need to transfer or reorganize assets within the business.

2. When is an Asset Inventory Report needed?

An Asset Inventory Report should be created when a business conducts a review and reconciliation of the actual quantity and value of assets against its accounting records, either periodically or when significant changes in structure or ownership occur.

Specifically, according to legal regulations, units must perform this task in the following cases:

Pursuant to Article 40 of the Law on Accounting 2015, businesses must conduct an asset inventory.

- At the end of each annual accounting period.

- Accounting units undergoing changes such as division, separation, consolidation, merger, dissolution, termination of operation, bankruptcy, or the sale or lease of assets.

- Accounting units changing their type or form of ownership.

- Businesses affected by unusual events such as fire, floods, and other damages.

- Businesses needing to re-evaluate assets according to a decision by a competent state authority.

- Other situations as stipulated by current law.

3. Basic Contents of an Inventory Report Template

Asset inventory is the process of detailed inspection and evaluation of all assets owned by a business within a specific period to reconcile with accounting records. The content of an Asset Inventory Report includes the following information:

Information about the inventorying unit and the unit being inventoried:

- Name of the inventorying unit: write the full name of the unit assigned to conduct the asset inventory.

- Name of the unit being inventoried: write the full name of the unit whose assets are being inventoried.

- Address of the inventorying unit and the unit being inventoried: write the specific address of each unit.

- Date of inventory: write the day, month, and year the asset inventory is conducted.

List of inventoried assets:

- Asset code: write the asset code according to the unit’s regulations.

- Asset name: write the full name of the inventoried asset.

- Quantity: write the actual quantity of the asset.

- Original cost: write the original cost of the asset according to the accounting records.

- Remaining value: write the remaining value of the asset according to the accounting records.

Asset inventory results:

- Actual asset quantity: write the actual quantity of assets inventoried.

- Actual asset value: write the actual value of assets inventoried.

- Discrepancy between actual asset quantity and value versus accounting data: write the difference between the actual asset quantity and value compared to the accounting data.

Signatures of the inventory committee members, chief accountant, and business director:

- After the inventory is completed, the inventory committee must sign to confirm the Asset Inventory Report. The chief accountant and the business director also need to sign for it to be used as a basis for accounting entries.

4. Asset Inventory Report Templates According to Regulations

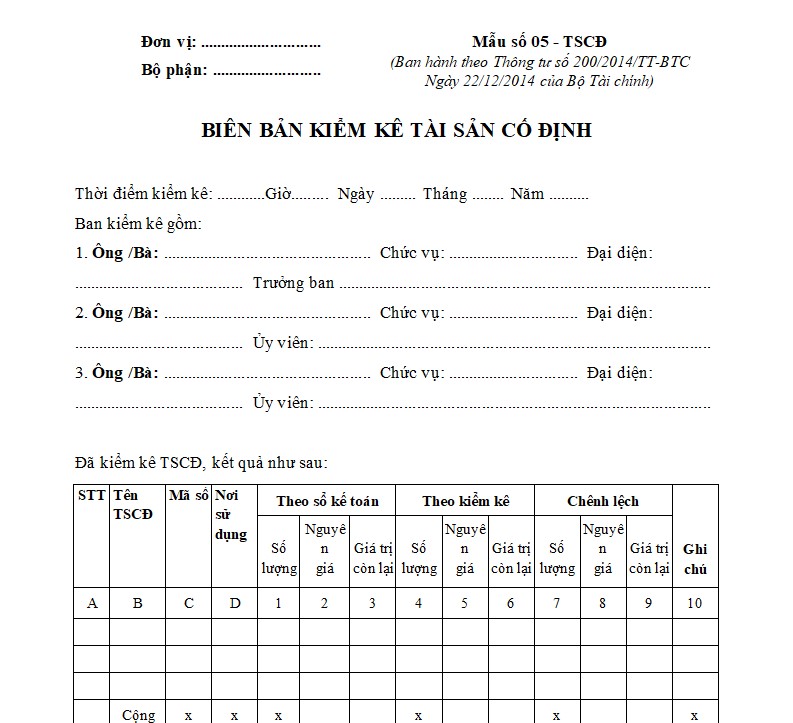

4.1. Fixed Asset Inventory Report Template according to Circular 200

This fixed asset inventory report template is issued with Circular 200/2014/TT-BTC, applicable to businesses in all sectors and economic components. This template is used to record the entire fixed asset inventory process of a unit.

Download now: [1OFFICE] Fixed Asset Inventory Report according to Circular 200.docx

4.2. Cash Fund Inventory Report Template according to Circular 133

This cash fund inventory report is a document issued with Circular 133/2016/TT-BTC, applicable to businesses that apply the accounting regime under Circular 133. This template is used to record the entire cash fund inventoryThe inventory committee is considered the “direct arbiter,” ensuring the inventory process is objective and the data is accurate. They are responsible for collecting actual data, comparing it with accounting records, and honestly reflecting the inventory results. In other words, the inventory committee is the bridge between the actual state of assets and the figures in the accounting books.

Responsibilities of the Inventory Committee:

- Create an inventory plan: The inventory committee is responsible for scheduling, defining the scope and subjects of the inventory, and notifying relevant departments.

- Conduct the physical inventory: Directly measure, count, and check the quantity and condition of assets, supplies, tools, and goods; compare with accounting records.

- Record honestly: All data must be recorded accurately, without alteration or omission. If there are discrepancies, the cause must be clearly stated.

- Propose handling measures: Make recommendations for handling surplus, missing, damaged, or lost assets; propose better management measures.

- Be legally responsible: The inventory committee is responsible for the accuracy and objectivity of the data recorded in the report.

If the inventory committee handles the “field work,” then the leadership is the “helmsman.” Leadership provides direction, supervision, and makes the final decisions based on the inventory results. They ensure the entire process complies with laws and regulations and serves the overall interests of the business.

Responsibilities of the Unit’s Leadership:

- Direct and supervise: The business leadership issues the decision to establish the inventory committee and assigns tasks to each member.

- Ensure transparency: Require the inventory to follow the correct template according to circulars (200/2014, 133/2016), without arbitrary changes or omissions.

- Review and approve: After completion, the leadership must read, review, sign, and stamp the inventory report to ensure its legal validity.

- Handle inventory results: Based on the committee’s recommendations, the leadership makes decisions on handling discrepancies (recording asset increases or decreases, assigning liability for compensation if any).

- Bear final responsibility: The leadership is ultimately responsible before the law, auditing bodies, and shareholders for the approved inventory data.

Clearly defining responsibilities helps to:

- Increase transparency in financial management.

- Reduce the risk of fraud or data inaccuracies.

- Ensure the inventory report becomes a solid legal basis for preparing financial statements, serving audits, or inspections.

8. Common Mistakes When Creating an Inventory Report and How to Fix Them

During the process of creating an asset inventory report, even with clearly defined templates, businesses can still easily make mistakes. These errors can stem from omissions in recording, a lack of rigor in organizing the inventory, or the incorrect application of legal regulations. The important point is that every mistake has a solution if the business understands and follows the correct procedure.

Missing or incorrect basic information:

- Common mistake: Omitting the unit’s name, department, date, or not clearly specifying the inventory time.

- Consequence: The report loses its legal validity and is difficult to reference when needed.

- Solution: Always check a list of mandatory information (unit name, time, location, inventory committee members) before signing.

Incomplete signatures for confirmation:

- Common mistake: Missing signatures from the warehouse keeper, accountant, or leadership.

- Consequence: The report is invalid and has no legal value during an audit.

- Solution: Ensure all inventory committee members and the unit’s leadership have signed before filing the document.

Recording data that doesn’t match reality:

- Common mistake: Data from accounting records and the physical count are not carefully compared, or the unit of measurement is recorded incorrectly.

- Consequence: Leads to inaccurate financial reports and risks during inspections.

- Solution: Conduct the inventory at least twice, with cross-checking, and clearly specify the unit of measurement in the inventory sheet.

Failing to state the reason for discrepancies:

- Common mistake: Only recording the discrepancy amount without explaining the reason (loss, damage, mix-up).

- Consequence: Raises suspicion of fraud and complicates accounting procedures.

- Solution: Always include a “Reason” column and clearly state the proposed solution.

Not complying with official circular templates:

- Common mistake: Creating a custom template or omitting information columns required by regulations.

- Consequence: The report is invalid and will not be accepted during an audit.

- Solution: Use the correct template according to Circular 200/2014 or 133/2016, only adding supplementary columns in an appendix if necessary.

Missing detailed appendices:

- Common mistake: For a warehouse with thousands of items, only a summary report is created without a detailed appendix.

- Consequence: Insufficient legal evidence, difficult to cross-reference.

- Solution: Create a detailed appendix to accompany the main report, number the pages, and add an overlapping signature across pages.

Improper storage of the report:

- Common mistake: Saving a soft copy without printing a hard copy, or storing it haphazardly, making it easy to lose.

- Consequence: Difficult to retrieve when needed for audits or tax authorities.

- Solution: Store both a signed hard copy and a digital version; organize by accounting period and assign a file code.

9. Vietnam’s Leading Enterprise Asset Management Solution

1Office Joint Stock Company provides asset management software for businesses and is regarded as the leading solution in Vietnam. This platform with integrated asset management features will help managers easily access and tightly control assets from anywhere.

The 1Office software provides a full suite of essential asset management features for businesses, including:

- Asset portfolio management: Manage asset portfolios by type, department, and location.

- Asset inventory management: Conduct periodic asset inventories, detect and handle asset discrepancies.

- Asset maintenance and repair management: Track the history of asset maintenance and repairs.

- Asset depreciation management: Calculate asset depreciation in accordance with legal regulations.

Register for a Free Feature Demo!

10. Frequently Asked Questions About Asset Inventory Reports

Who is responsible for creating the inventory report?

- Usually the Asset Inventory Committee, which includes:

- An accounting representative

- A representative from the department using the assets

- The person in charge of asset management

- A leadership representative (for approval)

Is it mandatory to use a specific template for the inventory report?

It is not mandatory to use a single template. Businesses can design a form that suits their needs. However, accountants often refer to Circular 200 or Circular 133 to ensure completeness and acceptance during audits.

How are asset discrepancies handled after an inventory?

- Asset surplus: record an increase and investigate the cause.

- Asset shortage: determine responsibility, report to leadership, and handle according to regulations.

- Damaged assets: consider for repair or liquidation.

How long should asset inventory reports be stored?

According to accounting storage regulations, the inventory report is a mandatory document and must be kept for a minimum of 5 years, depending on the type of asset and internal policies.

What is the difference between an asset inventory and a stock inventory?

- Asset inventory: applies to machinery, equipment, buildings, vehicles, and fixed assets.

- Stock inventory: applies to raw materials, goods, work-in-progress, and finished products. Both require a report, but the forms and objectives are slightly different.

Does the inventory report have legal value?

Yes. It is an important document for:

- Financial settlement

- Audits

- Inspections

- Determining responsibility in case of loss

- Adjusting accounting records

If you are looking for a reputable and effective enterprise asset management software, 1Office is a perfect choice for you. To learn more about this software, please contact us via:

- Hotline: 083 483 8888

- Facebook: https://www.facebook.com/1officevn/

- Youtube: https://www.youtube.com/@1office-chuyendoisodn

- Zalo OA: https://zalo.me/3883877516951440238