Download 30+ Latest Financial Statement Templates under Circulars 200, 133, and 99

Financial statements are a system of reports that reflect a company’s financial position, business results, and cash flows for an accounting period. They are a crucial basis for evaluating operational efficiency and legal compliance. Starting in 2026, when Circular 99/2025/TT-BTC replaces Circular 200, the financial statement templates will be adjusted for each type of business. This article will compile a complete set of 30+ standard 2026 financial statement templates according to Circulars 200, 133, and 99, along with application guidelines and full download files.

Currently, depending on their scale and operational characteristics, businesses can apply the financial statement templates according to the corresponding circulars below:

Additionally, small and medium-sized enterprises can still apply the chart of accounts system under Circular 200/2014/TT-BTC to prepare financial statements, provided that they notify the direct tax authority and apply it consistently throughout the fiscal year. |

Mục lục

- 1. Financial statement template under Circular 200

- 2. Financial statement template according to Circular 133

- 3. Financial statement templates per Circular 99, applicable from the 2026 fiscal year onwards

- 4. Principles for Presenting Information in Financial Statement Templates

- 5. Notes on Preparing Financial Statements

- 6. Solutions to Standardize Data Before Preparing Financial Statements

- Conclusion

1. Financial statement template under Circular 200

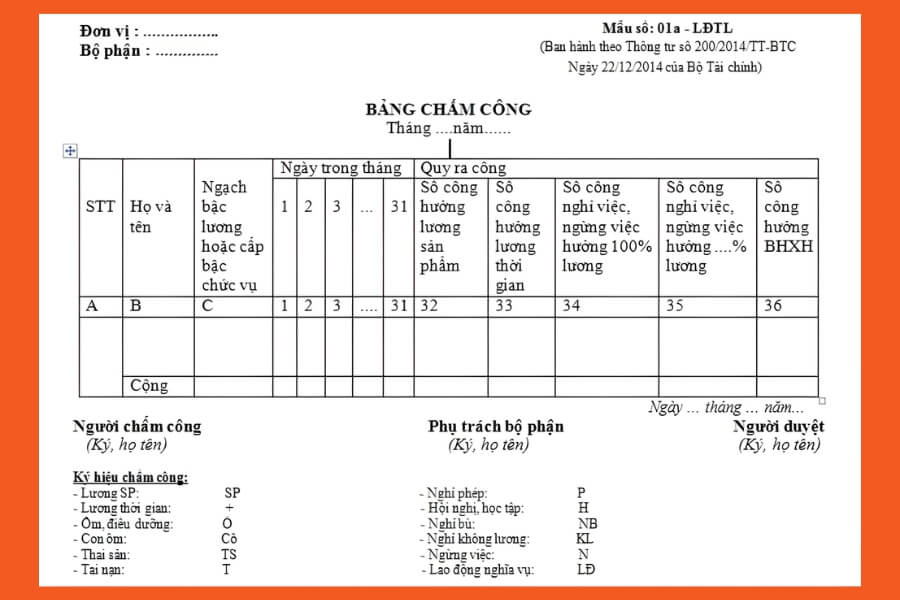

According to Article 100 of Circular 200/2014/TT-BTC, a company’s financial statement system is divided into two types: annual financial statements and interim financial statements:

1.1. Annual financial statement template

This is a report prepared at the end of the fiscal year, fully reflecting the company’s financial position, business results, and cash flows for the entire year. The annual financial statement is mandatory and is usually prepared on December 31st each year.

The annual financial statement system includes:

| No. | Report Type | Form No. | Notes |

| 1 | Statement of financial position | B01 – DN | Replaces the Balance Sheet (Circular 200) |

| 2 | Statement of income | B02 – DN | |

| 3 | Statement of cash flows | B03 – DN | Direct method |

| B03 – DN | Indirect method | ||

| 4 | Notes to the financial statements | B09 – DN |

1.2. Interim financial report template

Interim financial reports reflect the financial situation and business results on a quarterly or semi-annual basis, helping businesses adjust their operations in a timely manner. These reports are prepared in two forms: a full version and a summary version.

Full interim financial report template

| No. | Report | Form No. |

| 1 | Interim Balance Sheet | Form No. B 01a – DN |

| 2 | Interim Income Statement | Form No. B 02a – DN |

| 3 | Interim Cash Flow Statement | Form No. B 03a – DN |

| 4 | Notes to the Selected Financial Statements | Form No. B 09a – DN |

Condensed interim financial report template

| No. | Report | Form No. |

| 1 | Interim Balance Sheet | Form No. B 01b – DN |

| 2 | Interim Income Statement | Form No. B 02b – DN |

| 3 | Interim Cash Flow Statement | Form No. B 03b – DN |

| 4 | Notes to the Selected Financial Statements | Form No. B 09a – DN |

>>> Download the complete set of financial statement templates under Circular 200 HERE

Financial statement template according to Circular 200

2. Financial statement template according to Circular 133

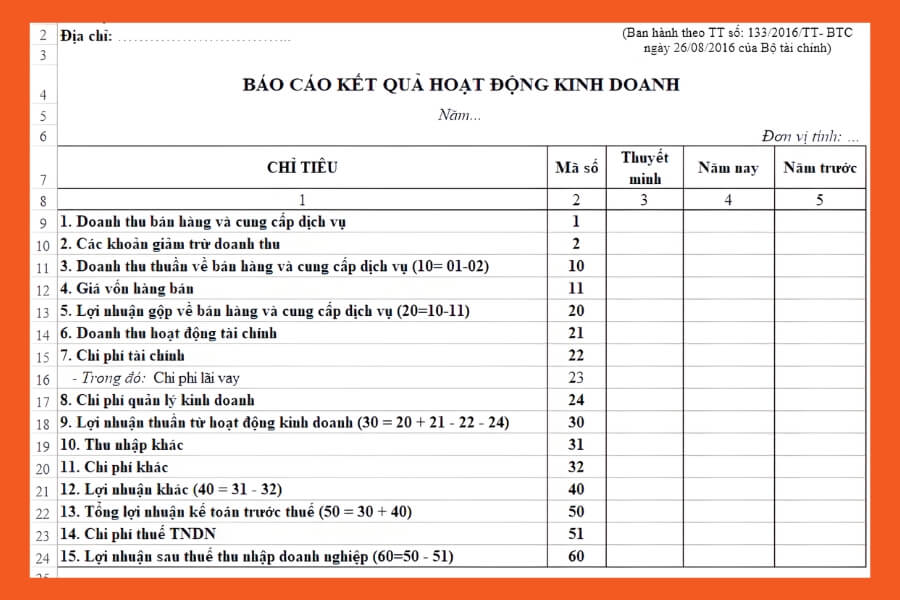

Circular 133/2014/TT-BTC regulates the financial statement template applicable to small, medium-sized, and micro-enterprises.

2.1. Annual financial reporting system for small and medium-sized enterprises with ongoing operations

Note: When submitting financial statements to the tax authority, enterprises must prepare and attach the Trial Balance according to Form F01 – DNN.

| No. | Report | Form No. | Note |

| 1 | Statement of Financial Position | Form No. B01a – DNN

or |

Mandatory |

| 2 | Income Statement | Form No. B02 – DNN | Mandatory |

| 3 | Notes to the Financial Statements | Form No. B09 – DNN | Mandatory |

| 4 | Statement of Cash Flows | Form No. B03 – DNN | Recommended |

2.2. Annual financial reporting system for small and medium-sized enterprises not operating continuously

The following are the annual financial statements required for small and medium-sized enterprises that do not operate continuously, designed to reflect their financial position during the actual period of activity.

| Financial Statement Set | Financial Statement Form under Circular 133 | Notes |

| 1. Statement of Financial Position | Form No. B01 – DNNKLT | Mandatory |

| 2. Income Statement | Form No. B02 – DNN | Mandatory |

| 3. Notes to the Financial Statements | Form No. B09 – DNNKLT | Mandatory |

| 4. Statement of Cash Flows | Form No. B03 – DNN | Recommended |

2.3. Annual financial reporting system for micro-enterprises

Below is the annual financial reporting system for micro-enterprises, with a streamlined structure suitable for their scale and volume of business transactions:

| Set of Financial Statements | Financial Statement Form per Circular 133 |

| 1. Statement of Financial Position | Form No. B01 – SME |

| 2. Income Statement | Form No. B02 – SME |

| 3. Notes to the Financial Statements | Form No. B09-SME |

>>> Full set of Financial Statement Templates per Circular 133 DOWNLOAD NOW HERE

Financial statement template per Circular 133

Read more: A comprehensive guide to analyzing corporate financial statements

3. Financial statement templates per Circular 99, applicable from the 2026 fiscal year onwards

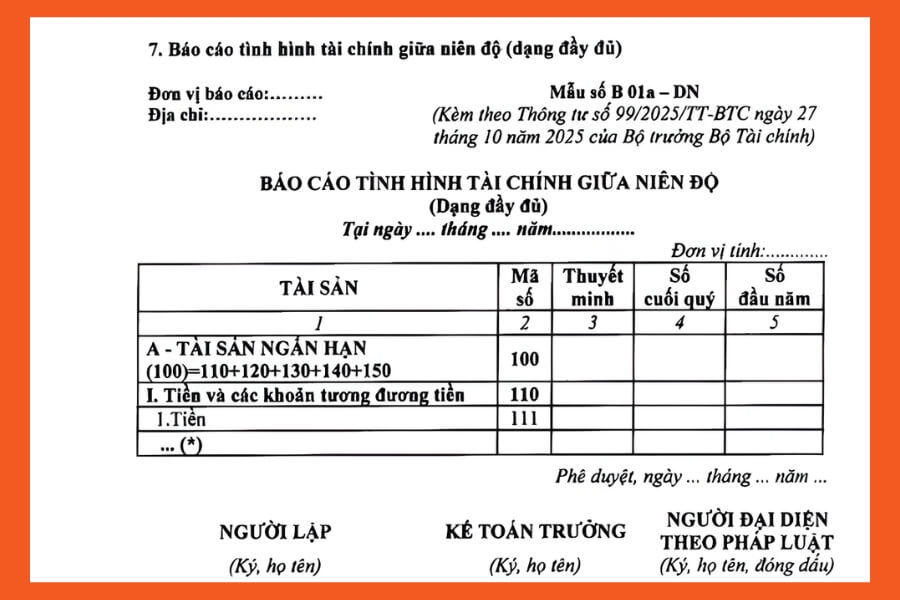

Circular 99/2025/TT-BTC was issued on October 27, 2025, officially replacing Circular 200/2014/TT-BTC. It takes effect from January 1, 2026, and applies to financial statements from the 2026 fiscal year onwards:

3.1. Annual financial statement templates

Below are the annual financial statement templates for businesses, categorized by their ability to meet the going concern assumption.

(1) Businesses that meet the going concern assumption

| No. | Report Type | Form No. | Notes |

| 1 | Statement of financial position | B01 – DN | Replaces the Balance Sheet (Circular 200) |

| 2 | Income statement | B02 – DN | |

| 3 | Statement of cash flows | B03 – DN | Direct method |

| B03 – DN | Indirect method | ||

| 4 | Notes to the financial statements | B09 – DN |

(2) The business does NOT meet the going concern assumption

| No. | Report Type | Form No. |

| 1 | Statement of Financial Position | B01-DNKLT |

| 2 | Business Performance Report | B02-DNKLT |

| 3 | Cash Flow Statement | B03-DNKLT |

| 4 | Notes to the Financial Statements | B09-DNKLT |

3.2. Interim financial report template

Below are interim financial report templates, prepared for short-term accounting periods to facilitate timely management and monitoring.

(1) Full version

| No. | Report Type | Form No. | Notes |

| 1 | Interim statement of financial position | B01a-DN | |

| 2 | Interim income statement | B02a-DN | |

| 3 | Interim statement of cash flows | B03a-DN | Direct method |

| B03a-DN | Indirect method | ||

| 4 | Selected explanatory notes to the financial statements | B09a-DN |

(2) Summary format

| No. | Report Type | Form No. | Notes |

| 1 | Interim Statement of Financial Position | B01b-DN | |

| 2 | Interim Income Statement | B02b-DN | |

| 3 | Interim Statement of Cash Flows | B03b-DN | |

| 4 | Selected Notes to the Financial Statements | B09a-DN | Used with the full version |

>>> Complete Set of Financial Statement Templates under the latest Circular 99 DOWNLOAD NOW HERE

Financial statement template under Circular 99, applicable from the 2026 fiscal year onwards

4. Principles for Presenting Information in Financial Statement Templates

Pursuant to Article 101 of Circular 200/2014/TT-BTC, information presented in financial statements must meet the following basic requirements:

- Fair and true representation of the enterprise’s financial position and business performance; ensuring completeness, objectivity, and accuracy.

- Complete and appropriate information, providing necessary data for users to correctly understand the nature, form, and risks of transactions and events; in some cases, additional notes are required to clarify influencing factors.

- Objective and unbiased presentation, ensuring neutrality in the selection, description, and interpretation of financial information.

- Free from material error, with no omitted information or inaccurate recording of items on the statement.

- Ensuring materiality, focusing on items that have a significant impact based on the nature and scale of the information.

- Verifiable, timely, and understandable, helping users predict, analyze, and make economic decisions.

- Consistent and comparable presentation, allowing for comparison between accounting periods and between enterprises.

Principles for presenting information in financial statement templates

5. Notes on Preparing Financial Statements

Compliance with legal regulations involves not only presenting information correctly but also adhering to requirements for form and procedure. Below are mandatory points that businesses and accounting departments must pay special attention to.

Note 1 – Strictly adhere to prescribed forms: The Vietnamese accounting legal system has issued a complete set of standardized financial statement templates. When submitting to tax authorities, statistical agencies, and other state management bodies, businesses are required to use these exact forms. Arbitrarily adjusting the structure or items may result in the report being rejected.

Note 2 – Clearly distinguish between financial reports and management reports

- Financial reports are legally binding, serve external parties such as tax authorities, banks, and investors, and must strictly comply with current accounting standards and regulations.

- Management reports serve internal operational purposes and can be flexibly designed according to the specific management needs of each business, such as by project, department, or business channel. Management reports cannot replace legally required financial statements.

Note 3 – Be flexible, but within permissible limits: Businesses may add or detail certain items on financial statements to better reflect their specific operations. However, all adjustments must not contradict general regulations and can only be applied with written approval from the Ministry of Finance.

Note 4 – Ensure consistency across accounting periods: Items, calculation methods, and presentation formats should be maintained consistently from one period to the next. This consistency not only facilitates data comparison but also demonstrates transparency and professionalism in accounting practices.

Notes on preparing financial statements

See more: 6 steps to effectively read financial statements

6. Solutions to Standardize Data Before Preparing Financial Statements

In practice, most errors in financial statements do not stem from the templates or presentation principles, but from scattered, slowly updated, or uncontrolled input data. Therefore, in parallel with using the correct regulated financial statement templates, many businesses are choosing to digitize financial management to ensure data is always complete and consistent before being compiled into reports.

In this context, management platforms like 1CRM act as operational support systems, helping businesses control their finances more effectively before entering the official financial statement preparation phase.

Specifically, 1CRM supports businesses in the following aspects:

- Track cash flow in real-time across multiple internal accounts, helping accountants and managers get a comprehensive financial picture at any given moment.

- Automatically remind of payments due, reducing the risk of overlooking debts or recording them in the wrong period.

- Centrally manage accounts receivable and payable information, supporting data reconciliation before preparing financial statements.

- Provide reporting dashboards and trend analysis, helping businesses review financial fluctuations and detect anomalies early in the accounting period.

- Digitize financial approval processes, strengthening internal controls and clarifying responsibilities among related departments.

- Ensure financial data security according to the ISO/IEC 27001:2013 standard, meeting information security requirements in a digital environment.

It should be noted that systems like 1CRM do not replace legally required financial statements. Instead, they serve as a foundational platform for data and process support, helping businesses reduce manual workload, limit errors, and improve information quality before preparing and submitting financial statements in the correct Ministry of Finance format.

Solution to support data standardization before preparing financial statements

Conclusion

Updating and correctly applying the new regulated financial statement templates is a mandatory requirement for businesses from 2026 onwards. We hope the collection of templates and guidance in this article will help you easily select, prepare, and submit reports accurately and on time.

However, for reports to accurately reflect the business’s situation, input data must also be centrally and consistently controlled. Therefore, many organizations choose 1Office to digitize financial and accounting management, reduce errors, and improve report quality. Contact 1Office for a consultation on a solution tailored to your business’s scale and needs.