Popular trial balance template, applicable to multiple industries

The Trial Balance will help you effectively control your cash flow and financial situation. Whether you are a CEO, business owner, head of accounting, accountant, or a finance student, understanding and using this balance sheet is crucial. In this article, 1Office will share with you basic information about the trial balance, common templates, principles for its preparation, and important notes for its use.

Mục lục

1. What is a Trial Balance?

The trial balance (also known as the statement of accounts) is a report that summarizes all economic transactions occurring within an accounting period.

This statement shows the opening balance, transactions during the period, and the closing balance for each account. This allows you to track the changes in each account, from cash and inventory to accounts payable.

The trial balance not only helps verify the accuracy of the data but also serves as the basis for preparing other financial statements, such as the balance sheet and the income statement.

2. Common Trial Balance Templates

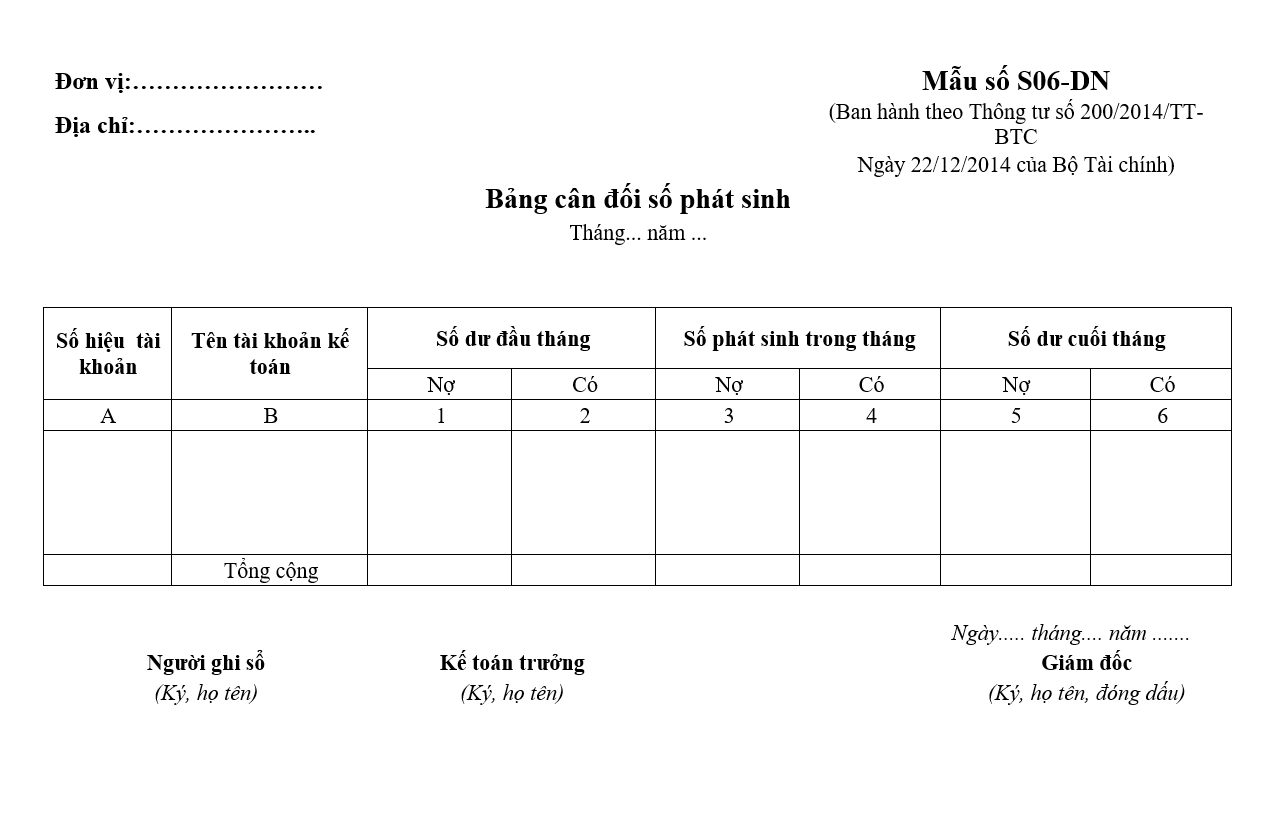

2.1. Trial Balance Template according to Circular 200

Download Free Trial Balance Template according to Circular 200

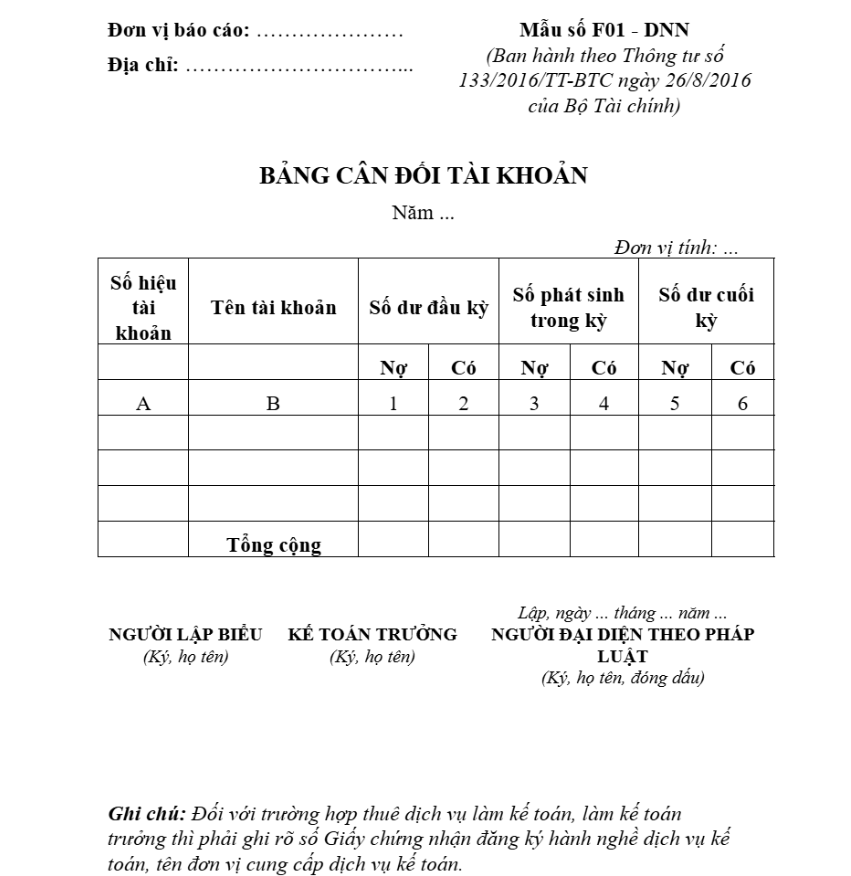

2.2. Trial Balance Template according to Circular 133

Download Free Trial Balance Template according to Circular 133

3. What does a Trial Balance include?

A trial balance has 8 columns, as follows:

- Column 1 – Account Number: This column is used to record the numbers of the level 1 accounts (or both level 1 and level 2) that the business uses for reporting during the year.

- Column 2 – Account Name: This column records the name of each account in the order of the account types the business is using.

- Columns 3 and 4 – Opening Balance: These two columns show the opening debit and credit balances for each account. This data is taken from the general journal or general ledger, or can be referenced from the data in columns 7 and 8 of the previous year’s trial balance.

- Columns 5 and 6 – Transactions during the

5. The role of the trial balance of accounts in a business

The trial balance of accounts is an important accounting tool that helps businesses track detailed transactions during a period and accurately assess their financial situation. The role of the trial balance of accounts in a business can be analyzed through the following points:

-

Tracking debits and credits: The trial balance allows accountants to clearly understand the debit and credit balances of each account, thereby controlling cash flow and expenditures.

-

Supporting financial statement preparation: The trial balance of accounts is the basis for preparing financial statements such as the balance sheet, income statement, and cash flow statement.

-

Managing liabilities and receivables: Thanks to the trial balance, businesses can track accounts receivable and accounts payable, thereby avoiding the risks of late payments or uncollectible debts.

-

Evaluating business performance: The aggregate figures from the trial balance help management clearly see the efficiency of production and business operations and the level of profitability, thereby making accurate strategic decisions.

-

Detecting errors and fraud: The trial balance of accounts helps accountants easily compare and reconcile data, detect discrepancies or unusual items, and enhance the reliability of financial information.

Thus, the trial balance of accounts is not only an accounting tool but also an important management tool that helps businesses operate transparently, efficiently, and sustainably.

The role of the trial balance of accounts in a business 6. Classification of the trial balance of accounts by industry

The trial balance of accounts is applied differently depending on the specific operations of each type of business. A clear classification helps accountants and business leaders manage data accurately, serving financial goals and business strategy.

6.1 Manufacturing businesses

-

Focuses on raw materials, production costs, and inventory.

-

Important accounts often include: raw materials, direct labor costs, manufacturing overhead, and finished goods inventory.

-

The trial balance helps businesses track production costs and calculate product costs, thereby optimizing the production process and controlling inventory.

6.2 Trading businesses

-

Emphasizes sales revenue, cost of goods sold, and customer receivables.

-

Common accounts include: merchandise inventory, shipping costs, selling expenses, accounts receivable, and accounts payable.

-

The trial balance helps businesses manage inventory, monitor revenue and debts, ensure smooth business operations, and optimize cash flow.

6.3 Service businesses

-

Focuses on service costs, contract revenue, and accounts receivable.

-

Important accounts include: labor costs, supply costs, outsourced service costs, service revenue, and customer receivables.

-

The trial balance helps track contract payment status and measure service profitability, thereby improving business operational efficiency.

6.4 Non-profit organizations

-

Emphasizes tracking funding sources, grants, and operating expenses.

-

Important accounts include: sponsored capital, contribution funds, operating expenses, project costs, and accounts receivable/payable.

-

The trial balance helps non-profit organizations manage resources effectively, ensure financial transparency, and optimize budget utilization for non-profit goals.

-

Conclusion

The trial balance of accounts plays a crucial role in controlling and monitoring a company’s financial situation. It not only helps managers and accountants track changes in each account but also serves as a solid foundation for preparing other financial statements, such as the balance sheet and the income statement. Understanding and correctly using the trial balance will help you ensure accuracy in accounting records, thereby supporting effective financial decision-making for the business.