Sales Document Circulation Process According to Accounting Law

The sales document circulation process plays a crucial role in financial management and optimizing a company’s cash flow. A standard process helps businesses optimize cash flow by allowing them to receive cash immediately from sales documents, instead of waiting for customer payments. This enables the business to maintain a continuous cash flow, ensuring sufficient working capital for operations and growth. So, what constitutes a standard process? How can you build a complete document circulation process? Let’s find out with 1Office in this article.

Mục lục

1. What are accounting documents?

According to the Law on Accounting, accounting documents are materials and evidence related to the financial and economic transactions of a business. These documents form the basis for recording, verifying, and reconciling transactions within the accounting system.

What content must an accounting document include?

The Law on Accounting specifies that an accounting document must include all of the following content:

- Name and code of the accounting document.

- Date (day, month, year) of issuance.

- Name and address of the issuing organization or individual.

- Name and address of the receiving organization or individual.

- Content of the economic or financial transaction that occurred.

- Quantity, unit price, and total amount of the transaction written in numbers; the total amount on documents used for cash receipts and payments must be written in both numbers and words.

- Signatures and full names of the preparer, approver, and other relevant individuals.

Regulations on documents under the current corporate accounting regime

Clause 3, Article 9 of Circular No. 200/2014/TT-BTC stipulates that all accounting document forms are for guidance and are not mandatory. Businesses can either use the forms issued in Appendix 3 of this Circular or design their own forms to suit their operations and management requirements, provided they ensure all necessary information is included as required by the Law on Accounting and related regulations.

Regulations on electronic documents

With the advancement of technology, many documents are now digitized. Article 17 of the Law on Accounting stipulates that an electronic document is recognized as an accounting document if it contains the content specified in Article 16 and is presented in the form of electronic data, is encrypted, and remains unchanged during transmission. Electronic documents must ensure security and integrity and must be managed and inspected to prevent any misuse, intrusion, or unauthorized use. Electronic documents must be managed like original accounting documents and require appropriate devices for use.

2. Sales accounting documents

Sales accounting documents are materials and evidence that record a company’s sales transactions. They serve as the basis for bookkeeping, verifying, and reconciling financial transactions, while also ensuring transparency and accuracy in the company’s financial management. These documents not only help manage cash flow effectively but also support the preparation of financial statements and audits.

Common types of sales accounting documents include:

- Sales invoice: The primary document recording revenue from the sale of goods or provision of services. Invoices can be electronic or paper-based.

- Inventory delivery note: Records the issuance of goods from the warehouse to be sold to customers. This is a crucial document for inventory management and determining the cost of goods sold.

- Sales contract: A written agreement between the seller and the buyer outlining the terms of the sales transaction, including price, quantity, quality of goods, and payment terms.

- Cash receipt voucher: Records the amount of money paid by the customer to the business for a purchase. This is an important document for managing cash flow and debt collection.

- Goods delivery record: Confirms the delivery and receipt of goods between the business and the customer. This document helps control the quantity and quality of goods and prevents future disputes.

- Warranty card, warranty record: Records the company’s commitment to product warranty, helping to manage and track after-sales services.

- Adjustment invoice: Issued when it is necessary to correct information on a previously issued invoice, such as adjusting the sales price, quantity, or other errors.

3. The correlation between the sales and cash collection cycles

The correlation between the sales and cash collection cycles plays a crucial role and directly affects a company’s operations in several ways:

- Revenue generation: The sales cycle is the first stage in generating revenue for the business. Revenue is only truly recognized when the customer pays, so the cash collection cycle is the next stage to convert potential revenue into actual cash.

- Cash flow management: Effectively managing both cycles helps the business maintain a stable cash flow. A strong cash flow allows the company to reinvest, expand operations, and ensure payment of operating expenses.

- Reducing financial risk: By closely monitoring the cash collection cycle, a business can minimize risks related to bad debt and late payments. This helps protect its financial position and enhance liquidity.

- Process optimization: A tight integration between these two cycles helps optimize business processes, increase efficiency, and improve the customer experience. This also helps minimize errors and ensure transparency in financial management.

The close integration of sales and collection allows businesses to track and manage their finances more effectively. This makes it easier to plan budgets, forecast finances, and make investment decisions. Good financial management not only helps a business maintain stable operations but also creates a foundation for sustainable long-term growth.

4. The Most Accurate Sales Document Flow Process

The document flow process in the sales and collection cycle is summarized in the following diagram:

Explanation:

(1) Approaching customers

(2) Checking sales policies and providing quotes

(3) Negotiating and closing the order

(4.1) Checking accounts receivable

(4.2) Checking inventory

(5) Releasing goods from the warehouse

(6) Shipping and delivery

(8) Issuing invoices and recognizing revenue

(9) Debit note/Debt notification to the customer

To better understand each sales – collection process, the diagram above needs to be split into 2 parts according to the 2 corresponding operations.

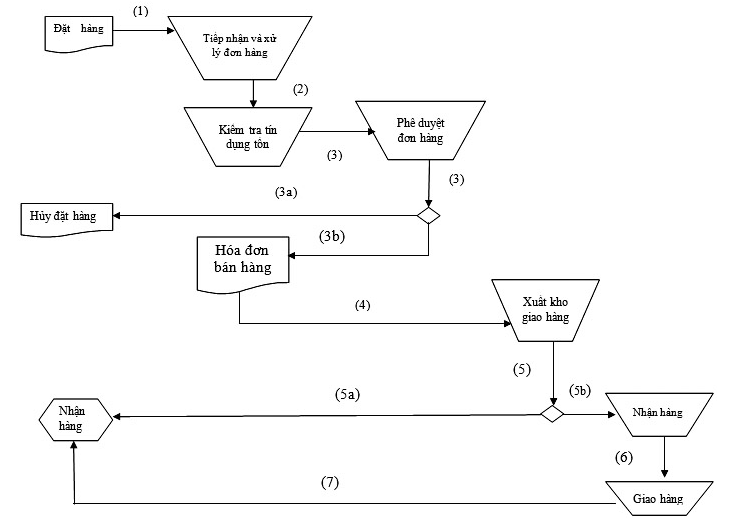

4.1. Diagram of the accounting document flow for sales operations

For example, at Pharmaceutical Company A, the company applies the document system according to Decision No. 15/2006/QD-BTC dated March 20, 2006, and Circular No. 200 of the Ministry of Finance. The accounting documents related to sales and collection reflect the economic transactions that have actually occurred and been completed. The document system used by the company in the sales process includes: Purchase Order, Economic Contract, Delivery Note, VAT Invoice, Sales Return Note, Sales Discount Note, Receipt, and Credit Note.

For the sales process:

- The customer sends a purchase request.

- The sales staff receives the purchase order, checks inventory, and assesses the customer’s credit.

- The sales manager approves the purchase order.

- a. If the purchase order is not approved, the sales staff informs the customer of the reason for rejection.

- b. If the purchase order is approved, the sales staff creates an invoice.

- The VAT invoice is sent by the sales staff to the warehouse to notify them to release the goods for the customer.

- Releasing goods:

- a. The customer picks up the goods directly from the warehouse.

- b. The delivery staff delivers the goods to the customer’s address.

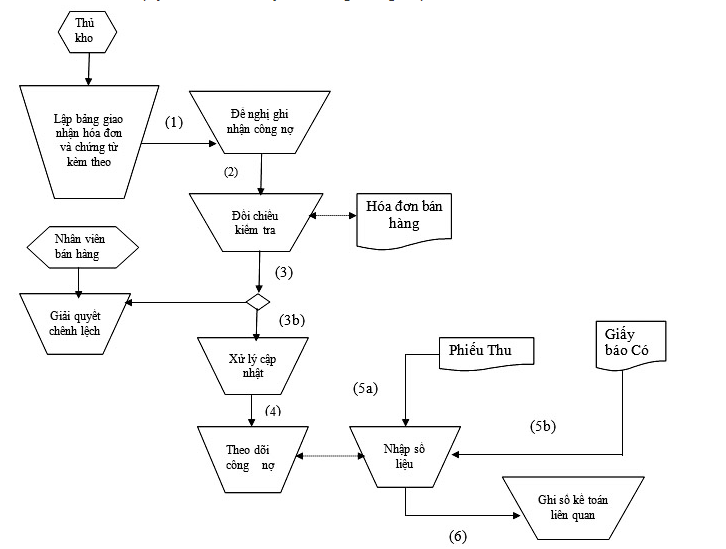

4.2. Diagram of the accounting document flow for collection operations

At Pharmaceutical Company B, for the collection stage:

- The warehouse keeper gives copy 3 of the VAT Invoice to the accounts receivable accountant; upon receiving the invoice, the accounts receivable accountant must sign the “VAT Invoice Logbook” and store this logbook at the warehouse.

- The sales accountant, based on the VAT Invoice created by the sales staff, reconciles the figures on the invoice with the data in the accounting system.

- If there is a discrepancy, the sales accountant immediately informs the sales staff to correct the error.

- Track customer accounts receivable.

- The payment accountant forwards the Credit Note and Receipt to the accounts receivable accountant for reconciliation, to check the debt collection status, and to update the data.

- The payment accountant records the related transactions in the books.

When building a document circulation process, it’s necessary to base it on the organization’s management characteristics, the accounting department’s structure, and the management requirements for the economic transactions documented. This helps ensure documents are circulated between departments scientifically and reasonably, avoiding duplication, omission, or convoluted routing (sales accounting document circulation sequence).

4.3. Combining the accounting document circulation process within the sales and cash collection cycle

By combining the sales and cash collection processes at companies A and B mentioned above, we get a complete diagram for both the sales and cash collection stages as follows:

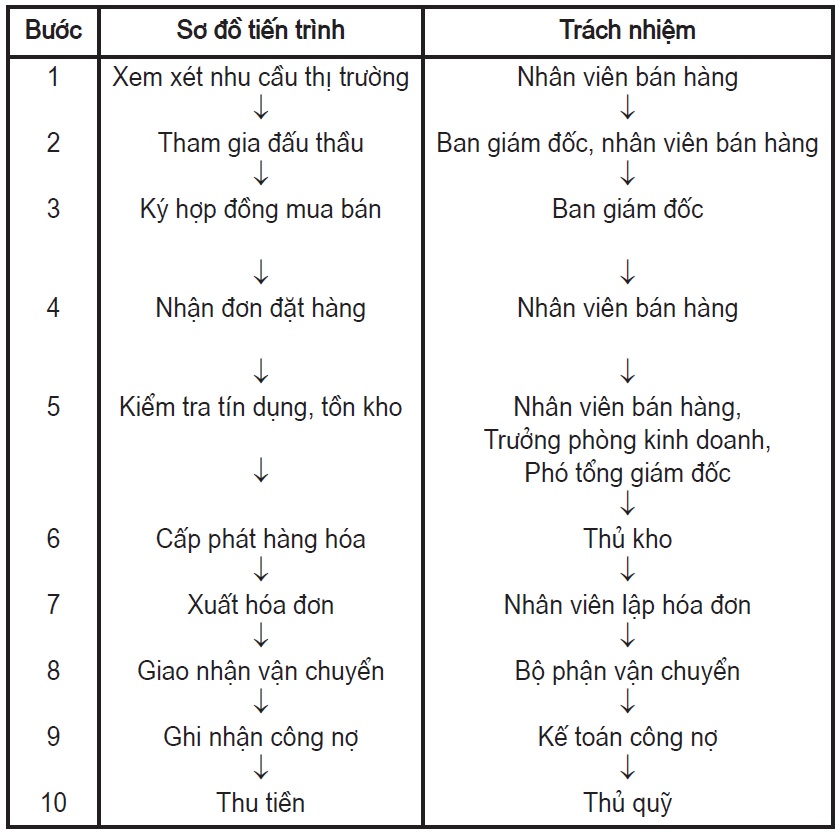

Step 1: Analyze market demand. It is necessary to analyze the annual, quarterly, and monthly sales plans, market expansion needs, and customer demand.

Step 2: Participate in bidding

After introducing the product, if medical facilities express interest, the company will participate in the bidding process.

Step 3: Sign the commercial contract

Upon winning the bid, the company will sign a contract with the medical facility, including information such as:

- Information of the seller and buyer (name, address, tax code, bank account, representative)

- Product list: drug name, dosage, concentration, origin, expiration date, specifications, quantity, unit price, total amount

- Goods quality

- Payment method

- Complaint resolution procedure

The Head of Sales reviews the contract and submits it to the Deputy General Director in charge of sales for approval.

Step 4: Receive purchase orders

- Directly: Staff receive orders from hospital pharmacy departments and clinics.

- Indirectly: The sales department receives orders via phone or fax.

Step 5: Check credit limit and inventory levels

The salesperson checks the customer’s inventory and credit limit, then forwards the order to the Head of Sales for approval.

Step 6: Issue goods

- Prepare goods: Check storage location, verify name, dosage, origin, lot number, expiration date, and pick the correct items according to the sales order.

- Inspect goods: The shipping staff re-inspects the goods before they leave the warehouse.

Step 7: Issue invoice

The accountant prints the invoice based on the sales order, delivery note, and purchase order.

Step 8: Shipping and delivery

- The delivery person prepares suitable transportation, ensuring the safety of the quantity and quality of the goods.

- After delivery, the recipient is responsible for submitting the invoice and related documents back to the company and relevant departments.

Step 9: Record accounts receivable

The accountant checks the consistency of sales documents and cross-references the invoice information with the system. If there are discrepancies, they notify the salesperson to resolve the issue and then record the receivable.

Step 10: Collect payment

Upon receiving a bank advice or a payment voucher from the customer (for cash payments), the accounts receivable accountant compares the amount received with the amount due and updates the Customer Payment Log to track commission expenses.

5. Common risks in sales document circulation

In any business, sales documents are not only a legal basis but also the foundation for recording revenue, cash flow, and tax obligations. However, the document circulation process often passes through multiple departments and processing stages, making it prone to risks. Without strict control, even a minor error can lead to significant consequences: inaccurate financial reports, financial losses for the business, and even legal troubles.

Below are common risks, along with their consequences and solutions, to help businesses better understand and take preventive measures.

- Errors in document creation:

-

- Risk: Missing information (date, amount, tax code) or incorrect data entry.

- Consequence: The document becomes invalid, is not accepted by tax authorities, and causes difficulties in tax finalization and deduction.

- Remedy: Review carefully before signing for approval; implement a cross-checking step between the accounting and sales departments.

- Prevention: Establish standard document templates and use software to limit manual data entry.

- Lost or delayed document circulation:

-

- Risk: Documents must pass through multiple departments, making them easy to lose or delay.

- Consequence: Revenue is not recognized in the correct period, affecting financial statements.

- Solution: Create a tracking log and send reminders when documents have not reached their destination.

- Prevention: Prioritize using electronic documents and centralized storage for easy retrieval.

- Internal fraud:

-

- Risk: Employees alter data, create fraudulent documents, or skip verification steps.

- Consequence: Loss of assets, incorrect profit reporting, and legal risks for the business.

- Solution: Increase unannounced inspections and cross-reference documents with actual goods.

- Prevention: Clearly segregate duties: the creator, verifier, and approver must be separate individuals.

- Improper document storage:

-

- Risk: Storing documents haphazardly, losing them, or destroying them before the legally required retention period (minimum 10 years).

- Consequence: When tax authorities or auditors conduct an inspection, the business lacks sufficient records → leading to potential penalties.

- Solution: Organize documents systematically with a clear storage index.

- Prevention: Use an electronic storage system with scanned copies for backup.

- Lack of standardization when implementing electronic documents:

-

- Risk: The business switches to e-invoices but fails to synchronize systems, leading to data duplication.

- Consequence: It takes a long time to look up information, and documents may be rejected by tax authorities if not in the standard format.

- Solution: Periodically check electronic data and reconcile it with accounting records.

- Prevention: Choose e-invoice software that meets the standards of the General Department of Taxation and train employees on its proper use.

6. Sales Document Circulation Process: Small Businesses vs. Large Corporations

The sales document circulation process is not the same for every business. Depending on the scale and complexity of the organization, the way documents are handled will differ significantly. Small businesses often opt for a lean, fast approach with fewer approval stages, while large corporations focus on control, segregation of duties, and transparency, resulting in a more multi-step and rigorous process.

To make it easier to understand, the section below will analyze the differences in detail across several aspects: the number of participating departments, the level of control, processing time, and the application of technology in each type of business.

6.1. Sales Document Circulation Process in a Small Business

In small businesses, the sales document circulation process is typically simple and streamlined. This is because the transaction volume is not yet high, the accounting team is small, and the management model is centralized. Therefore, steps are often condensed, prioritizing speed and flexibility over multiple layers of approval.

- Creating sales documents: A sales employee or accountant directly creates the sales invoice, warehouse issue slip, and related documents. The goal is to record the transaction immediately to avoid omissions.

- Confirming delivery and payment: The warehouse department confirms the shipment of goods; the accountant or cashier verifies payment documents (cash/bank transfer). A weakness is that the accountant often both creates and checks the documents, lacking an independent verification step.

- Bookkeeping and document storage: After the documents are fully signed, the accountant records them in the books and stores hard copies (paper) or soft files (Excel). Storage is often disorganized and documents can be easily lost without clear conventions.

- Reporting to the business owner: In a small business, the owner or director typically receives daily/weekly revenue reports directly from the accountant. This allows for quick decision-making but lacks internal control mechanisms.

6.2. Sales Document Circulation Process in a Large Corporation

Unlike small businesses, large corporations have a broader business scale, multiple branches, high transaction volumes, and stricter control requirements. Therefore, the sales document circulation process in corporations is often more multi-stepped, involves many departments, and is strongly supported by management software or an ERP system.

- Creating documents at the point of sale or branch: The sales department or branch where the transaction occurs will create the sales invoice, warehouse issue slip, and related documents. Unlike small businesses, corporations typically use a centralized software system for creation, which automatically sends data to the head office.

- Warehouse department confirms and updates the system: Goods are only dispatched with valid documentation. Warehouse staff will cross-reference the sales order with the actual quantity. The confirmation is recorded immediately in the system, avoiding the “do first, enter later” situation.

- Branch accounting department verifies documents: After the goods are dispatched, the branch accountant reviews the data and checks the validity of documents (invoice, issue slip, payment proof). This step creates the first layer of control, reducing the risk of fraud or errors.

- Head office finance/accounting department consolidates: Documents from branches are sent to the head office, where the finance department reconciles and consolidates them into the corporation-wide report. Thanks to the ERP, data is updated in real-time, reducing paperwork.

- Centralized approval and storage: The department head, chief accountant, or Chief Financial Officer (CFO) approves the documents. They are then stored both as hard copies (as required by law) and electronically in the system. This ensures transparency and easy retrieval for internal audits or tax authority requests.

————————————–

Above are the details of the common sales and cash collection document circulation process applied by businesses in Vietnam. We hope this information is helpful for your sales and cash collection process. Wishing you success!