What are Intangible Fixed Assets? How to Identify and Account for Them

Intangible fixed assets are assets that do not have a physical form but have a determinable value and are held and used by the business in production and business activities. To help you better understand intangible fixed assets, as well as how to identify and account for them, in the article below, 1Office will share all the information about intangible fixed assets. Find out now!

Mục lục

- 1. What are intangible fixed assets?

- 2. Classification of a business’s intangible fixed assets

- 3. Recognition criteria for intangible fixed assets

- 4. Amortization methods for intangible fixed assets

- 5. Accounting principles for intangible fixed assets

- 6. The impact of intangible fixed assets on a business

1. What are intangible fixed assets?

According to the provisions in Clause 2, Article 2 of Circular No. 45/2013/TT-BTC: “Intangible fixed assets: are assets that do not have a physical form, represent an amount of invested value that meets the standards of intangible fixed assets, and participate in many business cycles, such as certain costs directly related to land use rights; costs of issuance rights, inventions, patents, copyrights…”

Simply put, intangible fixed assets are valuable assets that you cannot see or touch. Intangible fixed assets include rights, licenses, or useful ideas, etc., owned by the business and used in production, business, and service provision activities.

See more: What is owner’s equity? The most standard and accurate way to calculate owner’s equity

2. Classification of a business’s intangible fixed assets

According to the regulations on fixed asset management in Clause b, Article 6 of Circular 45/2013/TT-BTC, a business’s intangible fixed assets are clearly classified as follows:

| Type of intangible fixed asset | Details |

| Land use rights | – As stipulated in Point dd, Clause 2, Article 4 of the Circular

– The right to use a piece of land for a certain period to serve business purposes or construct a specific project. |

| Issuing rights | The exclusive right of a business to issue stocks or bonds to raise capital from the public. |

| Invention patents | The exclusive intellectual property right for a new invention or innovative technology. |

| Literary, artistic, and scientific works | Includes artistic, literary, and scientific works such as books, paintings, articles, research, reports, etc. |

| Products, results of artistic performances | Includes artistic works performed on stage, in film, or at other performance events. |

| Audio recordings, video recordings, broadcast programs | Includes audio recordings, video recordings, and programs broadcast on television, radio, or other media. |

| Encrypted satellite signals carrying programs | Satellite signals that carry encrypted programs to provide satellite television content. |

| Industrial designs, layout-designs of semiconductor integrated circuits | Includes industrial designs and layout-designs of semiconductor integrated circuits used in the production of electronic technology. |

| Trade secrets | Important and confidential information about business operations that a company keeps secret to ensure competitiveness and commercial advantage. |

| Trademarks and trade names | Includes symbols, brand names, or images used to distinguish and identify a company’s products or services. |

| Geographical indications | Indications or information about a specific location with business value, such as maps, geographical guides, project locations, etc. |

| Plant varieties and propagation materials | Intellectual property rights for unique plant varieties or propagation materials that a business owns and distributes. |

3. Recognition criteria for intangible fixed assets

Criteria for identifying intangible fixed assets

Any actual expenditure incurred by a business that simultaneously meets all three criteria specified in Clause 1, Article 3 of Circular 45/2013/TT-BTC, and does not form a tangible fixed asset, is considered an intangible fixed asset. The specific criteria are as follows:

- The intangible fixed asset must be certain to generate future economic benefits from its use.

- It must have a useful life of 1 year or more.

- The historical cost of the intangible fixed asset must be reliably determined and have a value of VND 30,000,000 or more.

Specifically, costs incurred during the development phase are recognized as internally generated intangible fixed assets if they satisfy the following 7 conditions:

- Technical feasibility

- Intention to complete the intangible fixed asset for use or sale,

- Ability to use or sell it

- Generation of future economic benefits

- Availability of adequate resources for development

- Ability to reliably measure the expenditure to create the intangible fixed asset

- Has an estimated useful life and value as prescribed

Simultaneously meeting the above criteria is a condition for identifying an asset as an intangible fixed asset. Costs that do not meet these criteria will be directly expensed or allocated to the business’s operating expenses.

Method for identifying intangible fixed assets

To identify an intangible fixed asset, a business uses a method that checks the following 3 factors:

- Identifiability: As one of a business’s basic financial indicators, an intangible fixed asset must be an asset that can be independently identified. This means it can be distinguished separately and is capable of being used, leased, sold, or exchanged to generate future economic benefits. (Note: intangible fixed assets cannot be combined with goodwill.)

- Control over a resource: Based on the business’s legal rights over the intangible fixed assets, the business has the right to control these assets.

- Future economic benefits: Intangible fixed assets must bring future economic benefits to the business. For example: cost savings, increased revenue, or other benefits related to the use of the intangible fixed asset.

If an asset meets all 3 factors above, it will be identified as an intangible fixed asset and recorded on the business’s financial statements. If it does not meet these factors, the asset may be considered under other regulations and may be accounted for as operating expenses for the period.

Example: A company’s logo is an intangible fixed asset that can be separately identified. This is because it is a distinct asset of the company, easily recognizable, and does not exist in physical form. Additionally, the company holds legal rights to its logo. The company’s logo can generate future economic benefits by helping to build a strong brand and attract customers. Every time the logo appears on their products, advertisements, or website, it increases brand recognition and contributes to sales revenue.

4. Amortization methods for intangible fixed assets

According to Article 13 of Circular 45/2013/TT-BTC, there are 3 specific methods for amortizing intangible fixed assets as follows:

Straight-line amortization method

Straight-line amortization is a method of calculating the wear and tear of an asset evenly over each year. In this method, the amortization expense is the same throughout its useful life. The formula for calculating straight-line amortization is as follows:

Annual Amortization = (Historical Cost – Residual Value) / Useful Life

This is the simplest method for calculating the amortization of intangible and tangible fixed assets. Businesses can calculate the asset’s wear and tear evenly throughout its useful life. However, when using this method, the amortization value does not accurately reflect the actual wear and tear of the asset.

Suppose a business has a project management software used in its production activities. This software has an initial historical cost of VND 10 billion and is expected to be used for 5 years.

Annual Amortization = (10 – 0) / 5 = 2 billion/year

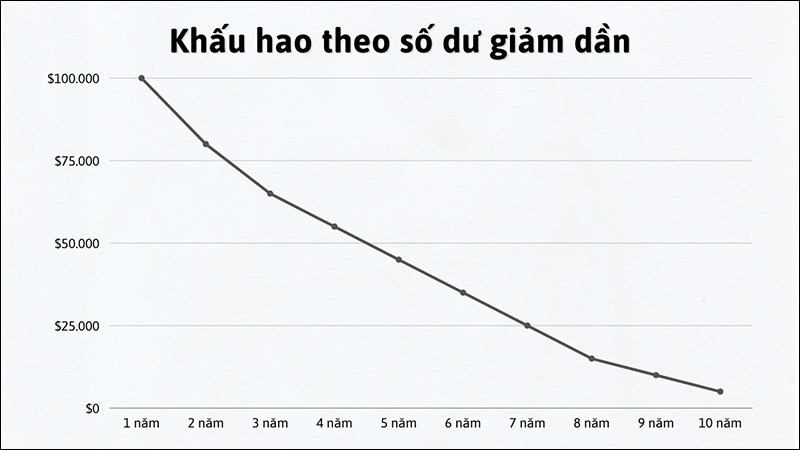

Declining balance amortization method

Declining balance depreciation is a method of calculating fixed asset depreciation based on a fixed percentage of the remaining depreciable value. The formula for calculating depreciation using the declining balance method is as follows:

Annual depreciation = Remaining depreciable value * Depreciation rate

This method depreciates fixed assets more heavily in the early stages. Therefore, this method is often suitable for fixed assets that lose more value in the early stages. Intangible fixed assets depreciated using the declining balance method must be newly invested (unused) intangible fixed assets.

Suppose a transportation company operates a fleet management system. This system is newly invested and has a remaining depreciable value of 80% after each year. The initial original cost of the system is 1,000,000 VND.

Annual depreciation = 1,000,000 * 0.8 = 800,000 VND/year (first year)

Annual depreciation = 800,000 * 0.8 = 640,000 VND/year (second year)

…

Units of production depreciation method

Units of production depreciation is a method of calculating depreciation based on the number of products produced or the operational output of an intangible fixed asset. The formula for calculating depreciation using the units of production method is as follows:

Annual depreciation = (Original cost – Residual value) / Total estimated units of production or operational output.

This is a suitable method when an intangible fixed asset has a variable expected lifespan or is not used consistently throughout its useful life. The types of intangible assets depreciated by the units of production method must be assets that satisfy the following conditions:

– Directly related to the production activities that create the product.

– The intangible fixed asset’s total quantity or volume of production can be determined.

– The intangible fixed asset must operate, produce, or be used at least at 100% of its designed capacity in each month of the fiscal year.

Suppose a brewery uses an automated quality control system to ensure that its products always meet quality standards. This system is integrated directly into the production process and inspects 10,000 beer bottles per month. The original cost of the system is 500,000 VND and it is expected to operate for 3 years.

Annual depreciation = (500,000 – 0) / (10,000 * 12 * 3) = 1.39 VND/beer bottle

5. Accounting principles for intangible fixed assets

How is the original cost of an intangible fixed asset determined?

According to the provisions of Clause 2, Article 4 of Circular 45/2013/TT-BTC on determining the original cost of intangible fixed assets by type is as follows:

| Type of intangible fixed asset | How to determine the historical cost of intangible fixed assets |

| Purchase | Historical cost = Actual purchase price payable + Taxes – Directly related costs incurred up to the time the asset is put into use. |

| Acquired through exchange | Historical cost = Fair value of the fixed asset received or fair value of the asset exchanged + Any additional amounts payable or minus any amounts receivable + Taxes – Directly related costs incurred up to the estimated time the asset is put into use. |

| Received as a grant, gift, donation, or transfer | Historical cost = Initial fair value + Directly related costs incurred up to the time the asset is put into use. |

| Internally generated | Historical cost = Directly related costs incurred in the construction and trial production phase up to the estimated time the fixed asset is put into use. |

| Land use rights | Historical cost = Total amount paid to obtain legal land use rights + Costs for compensation, site clearance, land leveling, and registration fees (excluding costs incurred to construct buildings on the land) or the value of land use rights received as a capital contribution. |

| Copyrights, industrial property rights, plant varieties | Historical cost = Total actual costs incurred to obtain copyrights, industrial property rights, and rights to plant varieties in accordance with intellectual property laws. |

| Software programs | Historical cost = Total actual costs incurred to acquire the software programs in cases where the software program is a separable component from the related hardware, layout-designs of semiconductor integrated circuits in accordance with intellectual property laws. |

Can the original cost of intangible fixed assets be changed?

According to Clause 4, Article 4 of Circular 45/2013/TT-BTC, the cases where the original cost of a company’s fixed assets can be changed are as follows:

- Revaluation of fixed assets in the following cases:

– By decision of a competent state authority.

– Reorganizing the enterprise, changing enterprise ownership, or changing the enterprise form: division, separation, merger, consolidation, equitization, sale, contracting, leasing, converting a limited liability company into a joint-stock company, or converting a joint-stock company into a limited liability company.

– Using assets for investment outside the enterprise.

- Investing in upgrading fixed assets.

- Dismantling one or more parts of a fixed asset where these parts are managed according to the standards of a tangible fixed asset.

When changing the original cost of a fixed asset, the enterprise must create a record clearly stating the basis for the change and redetermine the indicators of original cost, remaining value in the accounting books, accumulated depreciation, and useful life of the fixed asset, and proceed with accounting as prescribed.

In summary, the original cost of intangible fixed assets can be changed in certain cases as regulated.

6. The impact of intangible fixed assets on a business

Intangible fixed assets have a significant impact on the operations and business performance of an enterprise. Typical impacts of intangible fixed assets on a business include:

- Enhancing competitive advantage: Fixed assets such as trademarks, copyrights, trade secrets, intellectual property rights, etc., help businesses create unique and differentiated products or services compared to competitors.

- Building brand value: Intangible fixed assets like brand, reputation, goodwill, etc., contribute to building brand value for the enterprise. This typically includes the ability to increase the company’s stock value and generate significant profits in the future.

- Ensuring sustainability and stability: When possessing high-value intangible assets, a business has an advantage in attracting investors, business partners, and talented employees. This, in turn, promotes sustainable development for the enterprise.

- Creating a rich supply of offerings: Businesses can create diverse and abundant products and services thanks to the value of intangible fixed assets such as intellectual property rights, trade secrets, copyrights, etc.

- Financial reporting: Intangible fixed assets are a crucial part of a company’s financial statements. The value of these assets can increase or decrease over time. Businesses need to monitor and evaluate these assets to determine appropriate strategies.

Thus, intangible fixed assets are assets that lack physical substance but play a crucial role in the establishment and development of a business. We hope you found the content of this article useful. We wish you success!