4+ Standard Cash Handover Form Templates – Free Download

In all cash-related transactions – from end-of-shift fund handovers in businesses, employee travel advances, civil contract payments, to personal loans – the cash handover record is the most crucial “living document.” It helps accurately record the amount, denomination, purpose, and responsibilities of all parties at the moment of transfer. This is not just a simple administrative procedure but also a powerful legal tool that ensures accounting transparency, prevents loss and fraud, and protects rights in case of disputes. In this article, we will provide a general overview of the cash handover record: its definition, purpose, legal value, how to distinguish between a corporate fund handover record and a personal transaction record, and common situations where it is needed – helping you understand and apply it correctly in both business and daily life!

Mục lục

I. General Introduction to Cash Handover Records

A cash handover record is an administrative document created between two parties (the handing-over party and the receiving party) to officially record the transfer of a specific amount of cash at a certain time and place. This document details the amount, currency, form (banknotes, coins), condition (correct denomination, not torn), and purpose of the handover (fund handover, contract payment, advance, reimbursement, etc.), and includes the signatures of all parties to ensure transparency and accountability.

The main purposes of the record are:

- To confirm that the full and correct amount of money has been handed over.

- To serve as proof of the fulfillment of a financial obligation.

- To prevent future disputes, fraud, or losses.

Importance and Legal Value

A cash handover record holds high legal value as both an accounting document and legal evidence:

- It is a source document for recording in accounting books and settling cash funds (according to the Law on Accounting 2015 and Circular 133/2016/TT-BTC).

- It serves as evidence in civil, labor, or criminal disputes (in cases of fraud or misappropriation).

- It helps determine the point of responsibility transfer (who is responsible if the money is lost or incorrect after the handover).

- In a business, the record is a mandatory document for internal audits, state audits, or tax inspections.

Distinguishing Between a Cash Fund Handover Record and a Cash Handover Record

| Criteria | Cash Fund Handover Record (Corporate) | Cash Handover Record (General/Personal) |

| Parties Involved | Between accountants, cashiers, and work shifts within a business | Between individuals, or an individual and a business (not necessarily fund-related) |

| Purpose | Handing over the cash fund at the end of the day/shift, for advances, reimbursements, or fund deposits | Contract payments, debt repayment, personal advances, gifts, loans |

| Legal Requirements | Mandatory according to internal accounting regulations, Circular 133/2016/TT-BTC | Not legally required, but recommended for evidence purposes |

| Detailed Content | Opening fund balance, receipts/expenditures during the shift, closing fund balance, physical count | Specific amount, reason for handover, form of money, signatures of both parties |

| Frequency | Daily/per work shift | Situational (one-time or non-recurring) |

Khi nào cần lập biên bản bàn giao tiền mặt?

- Bàn giao quỹ tiền mặt cuối ca/ngày (doanh nghiệp): Thủ quỹ bàn giao cho thủ quỹ ca sau hoặc kế toán tổng hợp.

- Tạm ứng tiền mặt cho nhân viên (công tác, mua sắm vật tư, chi phí dự án).

- Hoàn ứng tiền tạm ứng sau khi kết thúc công việc.

- Thanh toán hợp đồng dân sự bằng tiền mặt (mua bán hàng hóa, dịch vụ, trả nợ cá nhân).

- Bàn giao tiền thu hộ (tiền vé, phí dịch vụ, tiền khách hàng nộp).

- Chuyển giao tiền mặt khi thay đổi nhân sự (thủ quỹ nghỉ việc, bàn giao quỹ cho người mới).

- Bàn giao tiền mặt trong giao dịch cá nhân lớn (trả nợ, tặng cho, cho mượn với số tiền đáng kể).

- Kiểm kê quỹ đột xuất theo quyết định của lãnh đạo hoặc kiểm toán.

Biên bản bàn giao tiền mặt là công cụ đơn giản nhưng cực kỳ quan trọng để đảm bảo minh bạch, trách nhiệm và bảo vệ quyền lợi trong mọi giao dịch liên quan đến tiền mặt. Trong doanh nghiệp, đây là chứng từ bắt buộc; trong giao dịch cá nhân, đây là biện pháp phòng ngừa tranh chấp hiệu quả.

II. Các Mẫu Biên Bản Bàn Giao Tiền Mặt Phổ Biến (Kèm Link Tải)

Bàn giao tiền mặt – dù là quỹ tiền mặt cuối ca, tạm ứng công tác, thanh toán hợp đồng hay hoàn ứng – luôn cần một biên bản rõ ràng để ghi nhận chính xác số tiền, mệnh giá, mục đích và trách nhiệm của các bên ngay tại thời điểm chuyển giao. Một biên bản chuẩn không chỉ giúp doanh nghiệp tuân thủ quy định kế toán mà còn là chứng cứ pháp lý vững chắc tránh tranh chấp, thất thoát hay gian lận sau này. Trong phần này, chúng tôi tổng hợp các mẫu biên bản bàn giao tiền mặt phổ biến (cập nhật 2026), từ mẫu bàn giao quỹ tiền mặt hàng ngày, tạm ứng nhân viên, thanh toán hợp đồng dân sự bằng tiền mặt đến bàn giao tiền thu hộ – tất cả đều dễ chỉnh sửa, tải miễn phí Word, kèm hướng dẫn điền chi tiết để bạn áp dụng nhanh chóng, minh bạch và an toàn pháp lý!

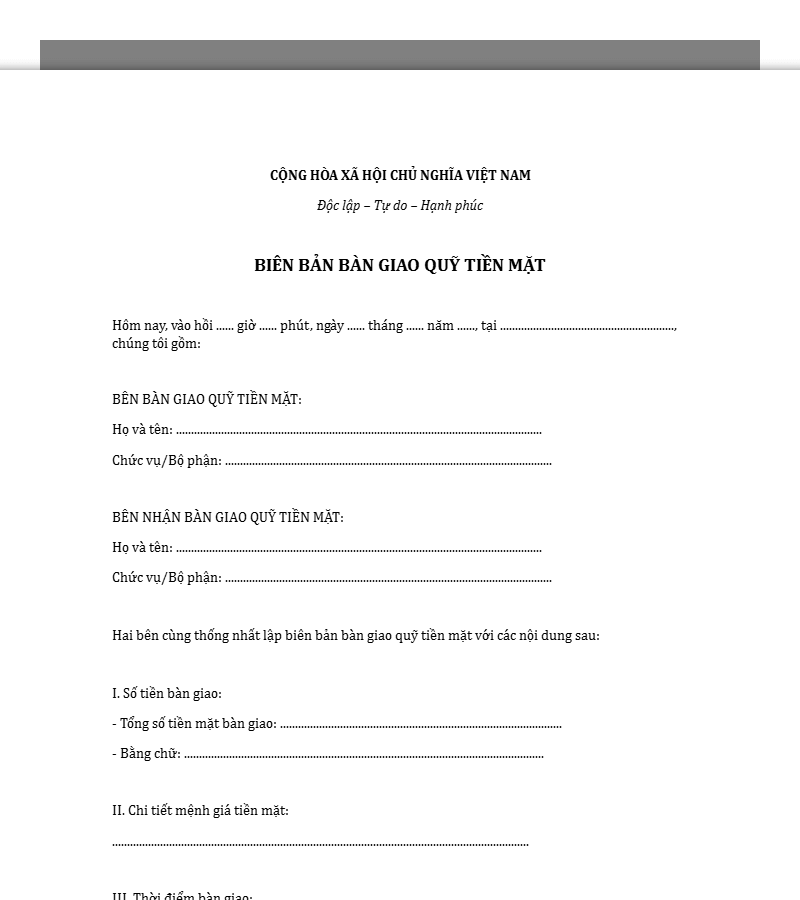

Mẫu 1: Biên bản Bàn Giao Quỹ Tiền Mặt (Dành cho Doanh nghiệp/Thủ quỹ)

Trong môi trường doanh nghiệp, việc bàn giao quỹ tiền mặt cuối ca, cuối ngày hoặc khi thay đổi nhân sự là quy trình bắt buộc để đảm bảo tính minh bạch, tuân thủ quy định kế toán và tránh thất thoát. Biên bản bàn giao quỹ tiền mặt là chứng từ quan trọng ghi nhận tồn quỹ thực tế, cơ cấu mệnh giá, chứng từ kèm theo và trách nhiệm của thủ quỹ. Mẫu này được thiết kế chuẩn theo quy định kế toán Việt Nam, giúp kế toán, thủ quỹ dễ dàng kiểm kê, đối chiếu sổ quỹ và bảo vệ quyền lợi doanh nghiệp một cách chuyên nghiệp, an toàn pháp lý.

Tải Ngay Mẫu Biên bản Bàn Giao Quỹ Tiền Mặt

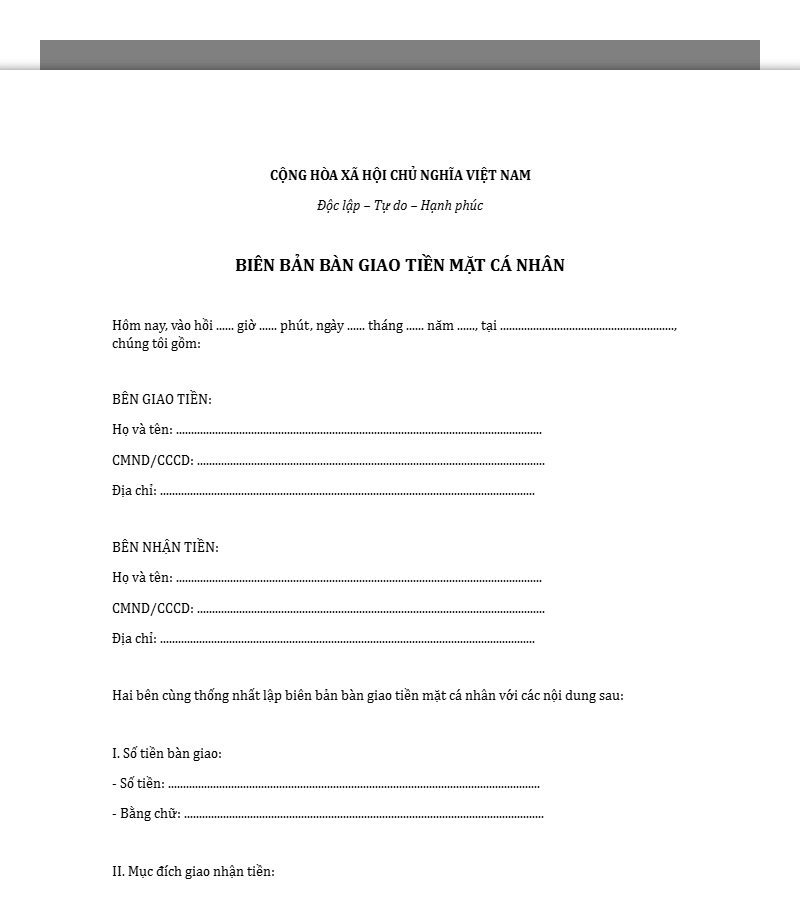

Mẫu 2: Biên bản Bàn Giao Tiền Mặt Cá Nhân (Giao dịch dân sự, vay mượn, mua bán)

Với các giao dịch cá nhân như cho vay, mượn tiền, thanh toán mua bán hàng hóa hoặc chuyển tiền giữa cá nhân với nhau, biên bản bàn giao tiền mặt là “lá chắn” pháp lý đơn giản nhưng cực kỳ hiệu quả để ghi nhận số tiền, mục đích và cam kết của các bên. Mẫu này phù hợp cho mọi giao dịch dân sự không chính thức, giúp tránh tranh chấp về số tiền, thời điểm bàn giao hay trách nhiệm trả nợ sau này, đồng thời vẫn đảm bảo tính pháp lý khi cần dùng làm chứng cứ trước tòa.

Tải Ngay Mẫu Biên bản Bàn Giao Tiền Mặt Cá Nhân

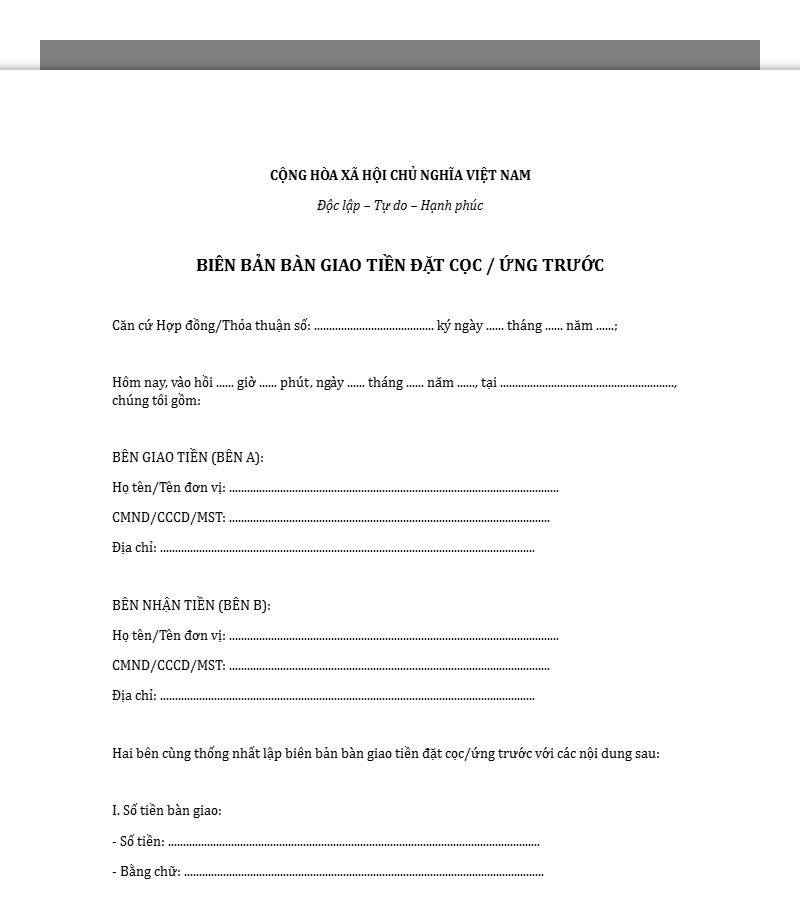

Mẫu 3: Biên bản Bàn Giao Tiền Đặt Cọc/Ứng Trước

Tiền đặt cọc hoặc ứng trước là khoản tiền quan trọng trong các giao dịch mua bán nhà đất, thuê mặt bằng, hợp đồng dịch vụ hoặc dự án. Biên bản bàn giao tiền đặt cọc/ứng trước giúp các bên xác nhận rõ ràng số tiền, mục đích, điều kiện hoàn trả hoặc chuyển đổi thành thanh toán, tránh tình trạng “nói miệng” dẫn đến tranh chấp. Mẫu này được soạn chi tiết, nhấn mạnh cam kết pháp lý, phù hợp cho cả cá nhân và doanh nghiệp, giúp bảo vệ quyền lợi tối đa khi giao dịch liên quan đến số tiền lớn.

Tải Ngay Mẫu Biên bản Bàn Giao Tiền Đặt Cọc, Ứng Trước

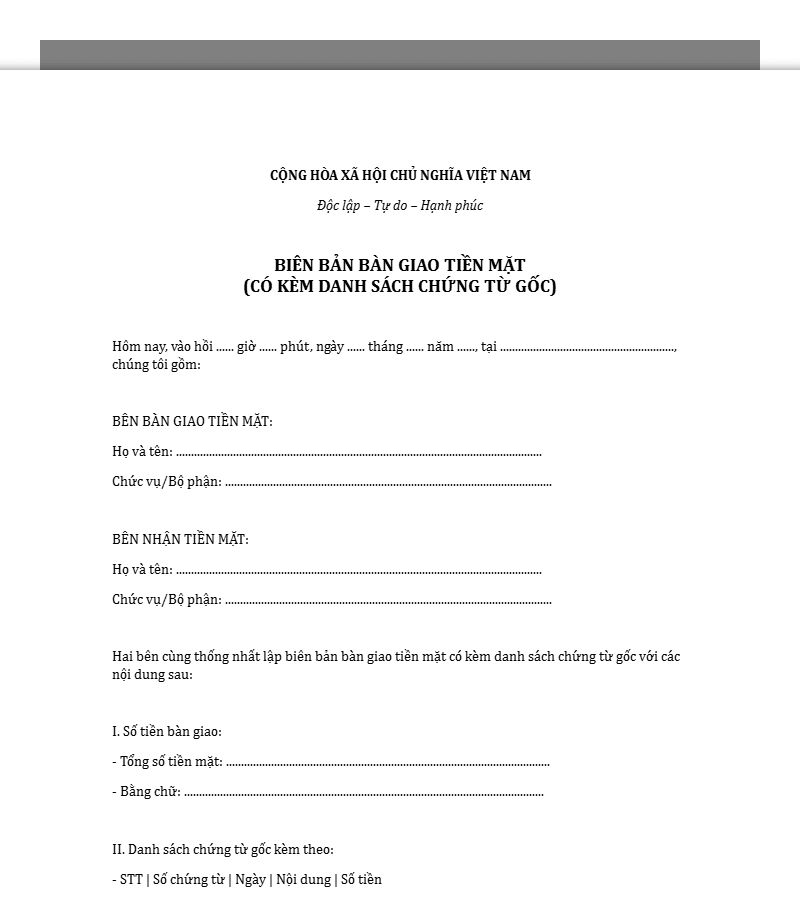

Mẫu 4: Biên bản Bàn Giao Tiền Mặt Có Kèm Danh Sách Chứng Từ Gốc

Khi bàn giao tiền mặt đi kèm với các chứng từ gốc (hóa đơn, phiếu thu, phiếu chi, hợp đồng, giấy tờ vay nợ…), biên bản cần được lập cẩn thận để liệt kê đầy đủ danh sách chứng từ, số lượng, tình trạng và mục đích bàn giao. Mẫu này đặc biệt hữu ích trong doanh nghiệp khi chuyển giao hồ sơ tài chính, hoàn ứng tạm ứng hoặc thanh toán hợp đồng lớn bằng tiền mặt, đảm bảo tính toàn vẹn chứng từ, dễ dàng kiểm toán và tránh rủi ro thất lạc giấy tờ quan trọng.

Tải Ngay Mẫu Biên bản Bàn Giao Tiền Mặt Kèm Chứng Từ Gốc

III. Hướng Dẫn Chi Tiết Biên Bản Bàn Giao Tiền Mặt

Biên bản bàn giao tiền mặt cần được lập theo thể thức văn bản hành chính chuẩn (Nghị định 30/2020/NĐ-CP về công tác văn thư), đảm bảo tính chính xác, minh bạch và có giá trị chứng cứ pháp lý cao nhất. Dưới đây là hướng dẫn chi tiết cách trình bày và điền từng phần (cập nhật thực tiễn kế toán, doanh nghiệp Việt Nam năm 2026).

1. Quốc hiệu, Tiêu ngữ và Tên Biên bản

Trình bày ở đầu trang, căn giữa, in đậm:

CỘNG HÒA XÃ HỘI CHỦ NGHĨA VIỆT NAM

Độc lập – Tự do – Hạnh phúc

BIÊN BẢN BÀN GIAO TIỀN MẶT

(V/v bàn giao tiền mặt quỹ ngày … / tạm ứng / thanh toán hợp đồng …)

Lưu ý: Tên biên bản nên ghi cụ thể mục đích để dễ tra cứu (ví dụ: “Bàn giao quỹ tiền mặt ca chiều ngày 01/01/2026”, “Bàn giao tiền tạm ứng công tác”, “Thanh toán hợp đồng dịch vụ bằng tiền mặt”).

2. Thời gian và Địa điểm lập biên bản

Ghi chính xác, cụ thể đến phút để xác định thời điểm pháp lý:

Hồi … giờ … phút, ngày … tháng … năm 2026

Tại: …………………………………………………………… (ví dụ: Phòng Kế toán – Công ty TNHH ABC, tầng 3, số 123 đường Lê Lợi, Quận 1, TP. Hồ Chí Minh)

Lưu ý: Thời gian phải là thời điểm thực tế bàn giao và ký biên bản, không ghi trước hoặc sau. Địa điểm nên là nơi kiểm kê và bàn giao tiền (phòng quỹ, phòng kế toán, văn phòng).

3. Thông tin các bên tham gia

Liệt kê rõ ràng, đầy đủ thông tin định danh:

- Bên Giao (Bên A): Họ và tên: …………………………………………………………… Chức vụ: Thủ quỹ / Kế toán trưởng / Nhân viên … Đơn vị: …………………………………………………………… Số CCCD/CMND: …………………………………………………………… Địa chỉ thường trú: ……………………………………………………………

- Bên Nhận (Bên B): Tương tự như trên.

- Thành phần chứng kiến (nếu có – khuyến nghị khi số tiền lớn hoặc bàn giao quỹ): Họ và tên: …………………………………………………………… Chức vụ/Đơn vị: …………………………………………………………… Số CCCD: ……………………………………………………………

Lưu ý: Đối với doanh nghiệp, ưu tiên có ít nhất một người chứng kiến (kế toán trưởng, trưởng phòng tài chính) để tăng tính khách quan.

4. Nội dung bàn giao tiền mặt

Đây là phần quan trọng nhất, cần ghi rõ ràng, không tẩy xóa:

- Tổng số tiền: Bằng số: …………………………………………………………… đồng Bằng chữ: …………………………………………………………… đồng chẵn

Chi tiết cơ cấu mệnh giá tiền (bắt buộc để tránh tranh chấp về loại tiền): Lập bảng chi tiết:

| Mệnh giá (đồng) | Số lượng tờ/cọc | Thành tiền (đồng) |

|—————–|——————|——————-|

| 500.000 | 20 tờ | 10.000.000 |

| 200.000 | 15 tờ | 3.000.000 |

| 100.000 | 50 tờ | 5.000.000 |

| 50.000 | 100 tờ | 5.000.000 |

| Tổng cộng | | 23.000.000 |

- Liệt kê các chứng từ, tài liệu đi kèm (nếu có):

- Phiếu thu/phiếu chi số … ngày …

- Hóa đơn GTGT số …

- Giấy tạm ứng số …

- Biên bản kiểm kê quỹ (nếu bàn giao quỹ).

- Purpose of handover: State specifically, for example: “Handover of cash on hand at the end of the shift on January 1, 2026,” “Cash advance for Mr. Nguyen Van A for a business trip to Da Nang,” “Payment for advertising service contract No. 01/HDDV dated December 15, 2025”

5. Commitment and Signatures

- Commitment: The parties agree to confirm:

- The handed-over amount is correct in quantity and denomination as stated above.

- The cash is intact, not torn, and not counterfeit.

- The receiving party is responsible from the time of signing this record.

- There are no complaints or disputes about the amount after signing.

Signatures:

REPRESENTATIVE OF THE HANDING-OVER PARTY (Party A) REPRESENTATIVE OF THE RECEIVING PARTY (Party B)

(Sign, full name) (Sign, full name)

Nguyen Thi X Tran Van Y

(Stamp if a corporate treasurer)

WITNESS (if any)

(Sign, full name)

Le Van Z

Note: Signatures must be wet signatures (signed by hand), not electronic signatures unless the business uses a valid digital signature (according to Decree 130/2018/ND-CP). The business should affix the company seal or the treasurer’s position seal.

6. Number of copies

- The record is made in 03 copies of equal legal validity:

- Copy 1: Stored in the Accounting/Treasury department (original file).

- Copy 2: Kept by the handing-over party.

- Copy 3: Kept by the receiving party.

- Clearly state at the end of the record: “This record is made in 03 copies of equal legal validity, with each party keeping 01 copy.”

Important notes for preparation and completion:

- Do not erase or use abbreviations → if there is a mistake, create a new record.

- Count the cash in the presence of both parties (count each note/stack).

- Attach photos of the cash (if the amount is large) or a video of the count as an appendix.

- Store the record for at least 10 years (according to the Accounting Law).

A standard cash handover record must detail the denominations, specify the exact time, include all necessary signatures, and have a clear commitment. Proper preparation helps businesses comply with accounting regulations, individuals avoid disputes, and fully protect their rights.

IV. Important Notes to Ensure Legal Safety

Creating a cash handover record may seem simple, but a lack of caution can lead to losses, disputes, or violations of accounting regulations. Below are the most important notes to ensure the record has high legal validity, is secure, and minimizes risks (updated according to Vietnamese accounting regulations for 2026).

1. Thoroughly count the cash

- Standard procedure:

- Both parties (handing-over and receiving) must count together in each other’s presence; do not let one party count alone.

- Count by each denomination (from largest to smallest), count each stack/note, and use a currency counter for large amounts.

- Compare the actual total amount with the amount recorded in the record (in numbers and words).

- Check the quality of the currency: not torn, not counterfeit, correct denomination.

- Note: If a discrepancy is found (shortage, surplus, counterfeit), immediately create a separate record of the error. Do not sign the handover record until it is resolved. Clearly state the reason and have both parties sign to confirm.

2. Use a witness

- Benefits:

- Increases objectivity and transparency, preventing one party from denying it later.

- Serves as additional evidence if a dispute arises (the witness can testify in court).

- Especially necessary for large amounts (>50 million VND), shift fund handovers, or cash handovers between unfamiliar individuals.

- Who should be a witness: Chief accountant, head of finance, other company employees, or an outsider (for personal transactions).

- How to record: Write down the witness’s full information (full name, position, ID card number) and ask them to sign the record for confirmation.

3. Storing the record

- Storage period:

- For corporate cash fund handover records: at least 10 years (according to the 2015 Accounting Law and Circular 133/2016/TT-BTC).

- For personal transaction records: recommended for at least 5–10 years (the statute of limitations for civil lawsuits is 3 years according to Article 429 of the 2015 Civil Code).

- Storage method:

- Hard copy: Store in an accounting/treasury filing cabinet, numbered sequentially, and categorized by year/month.

- Soft copy: Scan the entire record in color (high-quality PDF), save it on a secure cloud system (password-protected Google Drive, OneDrive), or in a document management software.

- Recommendation: Use a digital signature (if the company has one) to store an electronic version with equivalent legal validity.

4. Handling errors and disputes

- If an error is discovered after signing:

- Create a supplementary record or an addendum to the record clearly stating the error, the reason, and the corrective action, with both parties re-signing for confirmation.

- Do not erase the original copy (as it invalidates the evidence).

- If a dispute arises:

- Negotiate directly based on the record and accompanying documents.

- Seek mediation at the People’s Committee of the ward/commune or a commercial mediation center.

- File a lawsuit at the People’s Court if an agreement cannot be reached (3-year statute of limitations).

- Prevention: Always count in person, have a witness, and take photos/videos of the counting process (as an appendix) to increase credibility.

5. Reconciling with accounting books (For cash fund records)

- After signing the record, the accountant must immediately reconcile:

- The cash on hand at the end of the shift per the record = the cash on hand recorded in the cash ledger.

- Record any accompanying payment/receipt vouchers into the cash ledger.

- If there is a discrepancy, create a fund adjustment record and report to management immediately within the day.

- Comply with regulations for periodic fund audits (usually at the end of the month, or ad-hoc as required by auditors).

6. Clear and coherent language

- Use objective and precise language:

- Correct: “The total amount handed over is 50,000,000 VND (Fifty million Vietnamese dong even).”

- Incorrect: “Around 50 million” or “more than 50 million.”

- Avoid vague words: “enough,” “correct,” “ok” → replace with “correct in quantity and denomination as per the detailed table.”

- The purpose of the handover must be specific: “Handover of cash on hand for the afternoon shift on January 1, 2026” instead of “handover of money.”

A secure cash handover record must be based on a thorough count, have a witness, use precise language, be stored carefully, and be reconciled with accounting books promptly. By following these notes, you can almost completely eliminate legal risks, losses, or disputes related to cash.

V. Frequently Asked Questions About Cash Handover Records

Below are concise answers based on current Vietnamese law (as of January 1, 2026), combined with practical applications in business and personal transactions.

Does a cash handover record need to be notarized?

Not mandatory.

A cash handover record is a written agreement between parties (a document recording the transaction) and is not on the list of documents that require mandatory notarization according to the 2014 Law on Notarization (as amended and supplemented).

As long as it has the full handwritten signatures of all parties (deliverer, receiver, witnesses if any) and a seal (if it’s a business), the record is legally valid enough to serve as evidence before a court or state agency.

However, notarization is recommended if:

- The amount of money is very large (hundreds of millions of VND or more).

- The transaction involves unfamiliar individuals or has high-risk factors (loans, asset gifts).

- You want to increase its legal validity and facilitate future procedures (e.g., proving the origin of funds for tax declaration, anti-money laundering).

Can a cash handover record be handwritten?

Yes, and it is very common.

Vietnamese law does not require the record to be typed or pre-printed. A handwritten record (with clear, unerased handwriting) is fully legally valid if:

- It has the full handwritten signatures of all parties.

- The content is clear and accurate (amount in numbers and words, purpose, time, location).

- It has witnesses (if necessary) who sign to confirm. Note: Handwriting can be easily disputed, so it is preferable to type it (in Word), then print and sign it. If handwriting, use pre-printed letterhead or write the national emblem and motto at the top to increase professionalism.

When should a cash handover record be created?

Create it immediately at the actual time of the cash handover (when the money has been counted and physically transferred).

Specifically:

- Handing over cash funds for a work shift: Immediately at the end of the shift, before the next shift’s cashier signs to receive it.

- Cash advance/reimbursement: Immediately when the money is given to the person receiving the advance or returned to the fund.

- Paying a contract in cash: Immediately after counting and the receiving party confirms the full amount. Note: Do not sign the record before counting (risk of a shortfall), nor sign it afterward (difficult to prove the time of responsibility transfer). The recorded time must be accurate to the minute.

Are there any special considerations for large cash handovers?

Yes, enhanced safety and transparency measures are needed:

- Counting: Count in front of multiple people (with witnesses), use a money counter, and check each bill/stack.

- Witnesses: It is mandatory to have at least 1-2 witnesses present (accountant, department head, or an external party).

- Additional evidence: Take photos/videos of the counting process, record the serial numbers of bill stacks (if necessary).

- Notarization or authentication: It is recommended to notarize the record if the amount exceeds 100-200 million VND.

- Secure method: If the amount is very large, prioritize bank transfers over cash to reduce the risk of loss or counterfeiting.

- Reporting: The business must immediately record it in the cash book, report to management, and store the document carefully.

Can a cash handover record replace a contract?

It cannot replace a contract.

A cash handover record only documents the partial fulfillment of a payment obligation under a contract (or civil transaction).

The original contract (sales contract, loan agreement, service agreement, etc.) remains the primary document that stipulates rights and obligations, transaction value, payment terms, penalties for breach, etc.

The record is merely a document of execution (similar to a receipt/payment voucher) and cannot be a substitute if the law requires the transaction to be in writing (e.g., a loan agreement over 100 million VND requires a written document according to Article 463 of the 2015 Civil Code).

Note: If there is no original contract, the record still has value in proving a civil transaction, but it will be difficult to prove other terms (interest rates, repayment deadlines, penalties, etc.).