What is Manufacturing Overhead? How to Optimize Cost Control

Manufacturing overhead is a significant item that directly affects product cost, but not all businesses allocate and account for it correctly from the beginning. In this article, you will gain a clear understanding of what manufacturing overhead is, what it includes, how to allocate it, and what to note when accounting for it.

Mục lục

- 1. What is manufacturing overhead?

- 2. What does manufacturing overhead include?

- 3. How to allocate manufacturing overhead

- 4. Formula for calculating manufacturing overhead costs

- 5. Notes on accounting for Acct 627 – Manufacturing Overhead

- 6. Common mistakes when allocating manufacturing overhead

- 7. The role of manufacturing overhead in calculating product cost

- 8. Solutions to effectively reduce manufacturing overhead and increase business profits

1. What is manufacturing overhead?

According to Article 87 of Circular No. 200/2014/TT-BTC, which regulates the corporate accounting system, manufacturing overhead is defined as follows:

Manufacturing overhead includes all costs incurred to serve the general production and business processes at the factory, department, construction site, etc., excluding direct material costs and direct labor costs.

Thus, this is a crucial cost in determining the cost of products and services. Accurately allocating manufacturing overhead helps businesses determine the precise product cost, thereby making effective business decisions.

>> Read more: What are production costs? Classification, Examples, and Calculation Formula

2. What does manufacturing overhead include?

According to the regulations in Article 87 of the aforementioned Circular, manufacturing overhead recorded in Account 627 must be accounted for in two types: fixed manufacturing overhead and variable manufacturing overhead. Specifically:

- Fixed manufacturing overhead: These are costs that do not change with the quantity of products produced, such as depreciation of fixed assets, maintenance costs, and administrative management costs in production workshops and departments.

- Variable manufacturing overhead: These are costs that change directly or almost directly with the quantity of products produced, such as indirect raw materials, indirect materials, and indirect labor costs.

Below are some common manufacturing overhead costs in a business:

- Indirect raw materials and supplies costs: includes the costs of purchasing, transporting, storing, and using various raw materials and supplies for the production process, excluding direct materials.

- Indirect labor costs: includes salaries, wages, allowances, insurance, etc., for employees serving the production process, excluding direct labor.

- Purchased service costs: includes costs of outsourced services for general production and business, such as electricity, water, telephone, internet, warehouse rental costs, etc.

- Administrative management costs in production workshops and departments: includes salaries, wages, allowances, insurance, etc., for administrative management staff in production workshops and departments.

>> Read more: What are hidden costs? Classification & Formula for calculating Implicit Cost

3. How to allocate manufacturing overhead

At the end of the business period, the allocation of manufacturing overhead is calculated based on the normal capacity of the production machinery – which is the average number of products achieved under normal production conditions. Specifically:

| Case | Fixed manufacturing overhead costs | Variable manufacturing overhead costs |

| Actual production level is higher than normal capacity | Fixed manufacturing overhead costs are allocated to each product unit based on the actual production level incurred.

The fixed manufacturing overhead cost per product unit will decrease as production volume increases. |

Variable manufacturing overhead costs are fully allocated to the conversion costs for each product unit based on the actual costs incurred. |

| Actual production level is lower than normal capacity | Fixed manufacturing overhead costs are allocated to the conversion costs for each product unit based on the normal capacity level.

The unallocated manufacturing overhead is recognized as cost of goods sold for the period. |

Manufacturing overhead cost allocation table during the production and business process

4. Formula for calculating manufacturing overhead costs

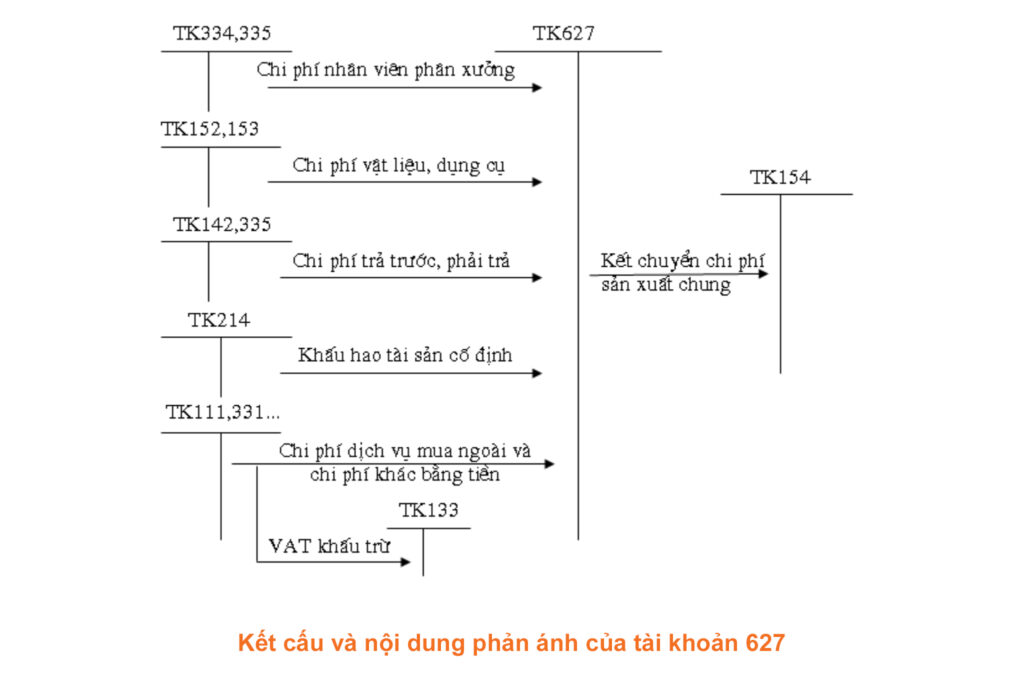

4.1. Structure and recorded content of account 627

According to Clause 2, Article 87 of Circular No. 200/2014/TT-BTC, manufacturing overhead costs are recorded in account 627. This account has no ending balance and includes 6 sub-accounts.

- Account 6271 – Workshop employee costs: Records costs such as salaries, allowances, mid-shift meals, social insurance, health insurance, trade union fees, and unemployment insurance payable to workshop management and production department staff.

- Account 6272 – Material costs: Includes costs of materials used for the workshop, such as materials for repairing and maintaining fixed assets, tools, and equipment under the workshop’s management and use, costs of temporary shelters, etc.

- Account 6273 – Production tool costs: Records costs of tools and equipment used for the production and business activities of the workshop, department, or production team.

- Account 6274 – Fixed asset depreciation costs: Includes depreciation costs of fixed assets used directly for production and business activities and fixed assets used jointly for the activities of the workshop, department, or production team.

- Account 6277 – Purchased service costs: These are costs of external services supporting the workshop or production department’s activities, such as repair costs, outsourcing costs, electricity, water, telephone expenses, fixed asset rental fees, and payments to subcontractors (for construction companies).

- Account 6278 – Other cash costs: Includes cash expenses other than those mentioned above that serve the activities of the workshop, department, or production team.

The accounts above form the basis for determining the total manufacturing overhead costs incurred during the production and business process, excluding direct material costs and direct labor costs.

4.2. How to calculate manufacturing overhead costs – Accounting for account 627

The formula for calculating manufacturing overhead costs is the sum of the 6 sub-accounts of account 627, including account 6271, account 6272, account 6273, account 6274, account 6277, and account 6278.

| Overhead manufacturing costs = Factory labor costs + Material costs + Production tool costs + Depreciation costs of fixed assets + Outsourced service costs + Other cash expenses |

Manufacturing overhead costs incurred during the period are recorded on the Debit side of account 627. The actual amount of manufacturing overhead costs incurred and paid during the period is recorded on the Credit side of account 627.

For unallocated manufacturing overhead costs, at the end of the period, they will be transferred to the Debit side of account 154.

4.3. Example of key economic transactions for account 627

At the end of the business period, electronics company A has a total Debit balance in account 627 of 75,000,000 VND, of which:

- Fixed manufacturing overhead is 21,000,000 VND and variable manufacturing overhead is 54,000,000 VND

- The normal capacity of machinery and equipment is 3000 products.

If the number of products produced during the period is 2500. Determine the manufacturing overhead to be transferred to calculate the cost of goods manufactured? Prepare the journal entry?

Instructions:

Since the normal capacity of machinery and equipment is 3000 products, there are 2 cases as follows:

- Case 1: If the number of products produced during the period is >= 3000, then all fixed and variable manufacturing overhead is included in the cost of goods manufactured.

- Case 2: If the number of products produced during the period is < 3000, then the variable manufacturing overhead is included in the cost of goods manufactured, and the fixed manufacturing overhead is allocated based on the normal capacity of machinery and equipment to the cost of goods manufactured and the cost of goods sold (period cost).

Specifically, if the number of products produced during the period is 2500 (lower than normal capacity), the manufacturing overhead is calculated as follows:

- Variable manufacturing overhead = 54,000,000 VND

- Fixed manufacturing overhead included in cost of goods manufactured = 21,000,000 x (2500/3000) = 17,500,000 VND

- Fixed manufacturing overhead included in period cost = 21,000,000 x (1 – 2500/3000) = 3,500,000 VND

From there, the accountant proceeds to record and prepare the journal entry:

- Debit Acct 154: (54,000,000 + 17,500,000) = 71,500,000 VND

- Debit Acct 632: 3,500,000 VND

- Credit Acct 627: 75,000,000 VND

5. Notes on accounting for Acct 627 – Manufacturing Overhead

When allocating and accounting for account 627 – Manufacturing Overhead, accountants should note the following issues:

- Salaries recorded in Acct 627 are for management staff and should be distinguished from the wages of direct labor involved in production, which are recorded in Acct 622.

- Raw material costs recorded in Acct 627 are for tools used in the workshop; managers need to distinguish these from direct materials used in production, which are in Acct 621.

- When accounting for manufacturing overhead costs, accountants must rely on valid and legal documents to ensure the accuracy of the data.

- The allocation of manufacturing overhead must be based on a reasonable allocation basis and must be carried out in accordance with current accounting regulations.

- Actual manufacturing overhead costs incurred and paid during the period are recorded on the Credit side of account 627.

- At the end of the period, accountants need to check and reconcile the figures on the business report to ensure accuracy. Unallocated manufacturing overhead will be transferred to account 154 – Work in Process.

6. Common mistakes when allocating manufacturing overhead

Allocating manufacturing overhead (MOH) is a crucial step in calculating product cost. This is an indirect cost but directly affects financial results and management decisions. However, in practice, many businesses often make the following mistakes:

6.1. Not separating fixed and variable costs

One of the biggest mistakes many businesses make is lumping all manufacturing overhead (MOH) into one group without classifying it into fixed and variable costs. The consequence is that when production volume changes, the cost allocated to each product is no longer accurate.

For example, during a period of lower-than-normal production, fixed costs like machine depreciation or factory rent remain the same, causing the unit cost to increase unreasonably. This leads to inaccuracies in evaluating business performance and the product’s competitiveness.

6.2. Using an unreasonable allocation basis

In practice, many businesses choose to allocate based on “labor hours” or “machine hours.” However, this is not always a suitable basis. For industries where costs arise from the number of machine setups, factory floor space, or production batches, using only one fixed basis will distort the results:

-

Simple products often get “burdened” with too much cost.

-

Complex products have their actual costs underestimated.

This causes the product cost to not accurately reflect the resources consumed, making it difficult for the business to make pricing decisions or analyze profitability.

6.3. Not adjusting for normal capacity

Another common mistake is allocating fixed costs based on actual output. When output is lower than expected, fixed costs are allocated to fewer products, causing the unit cost to increase abnormally.

Accounting standards require fixed costs to be allocated based on normal capacity, which is the average output achievable under stable production conditions. If this is not followed, the cost will not accurately reflect production capacity, leading to distorted financial reports and inaccurate business plans.

6.4. Lack of accurate and timely data

Manual recording, slow updates, or a lack of transparency in tracking machine hours, utility costs, auxiliary materials, etc., will make input data unreliable. When data is incorrect, manufacturing overhead allocation will not reflect reality, making it difficult to control costs and optimize production.

Additionally, a lack of timely data prevents businesses from making quick decisions, missing opportunities for improvement or cost reduction.

6.5. Not updating allocation methods to reflect actual changes

The production environment is always changing: product portfolios become more diverse, new technologies are adopted, or processes change. However, many businesses still use old allocation methods that were only suitable for a previous stage. This leads to allocation results that are increasingly detached from reality.

Businesses need to periodically review and adjust allocation criteria, and even apply more modern methods like Activity-Based Costing (ABC) to ensure accuracy.

7. The role of manufacturing overhead in calculating product cost

Manufacturing overhead (SXC) is a crucial component of the cost structure. Although not directly tied to a specific product, it strongly influences the entire process of cost and profit management. The role of manufacturing overhead can be viewed from several aspects:

7.1. Accurately determining product cost

The formula for calculating product cost includes not only direct material costs and direct labor costs, but also a reasonable allocation of manufacturing overhead. If a business omits or incorrectly allocates this, the product cost will be distorted, leading to inaccurate pricing. As a result, products may be overpriced, reducing competitiveness, or underpriced, causing the business to sell at a loss without realizing it.

7.2. Basis for pricing and competitive strategy

In practice, many businesses use a cost-plus pricing method. When manufacturing overhead is allocated accurately, the business has a solid basis for setting a market-appropriate price that is both competitive and maintains expected profits. Conversely, if the figures are inaccurate, the entire pricing strategy can be disrupted, causing losses for the business.

7.3. Impact on product mix and production strategy

Properly allocated manufacturing overhead helps businesses clearly see which products are highly profitable and which are reducing the overall profit margin. From there, managers can make strategic decisions such as: continuing to invest in expanding profitable products, improving underperforming ones, or discontinuing loss-making product lines. This is a crucial basis for optimizing the product portfolio and setting long-term production direction.

7.4. Meeting accounting and financial reporting requirements

Allocating manufacturing overhead according to accounting standards not only ensures the transparency and reliability of financial reports but also supports internal management. Businesses can monitor the performance of each workshop and department in detail, thereby identifying weaknesses and waste for timely adjustments.

8. Solutions to effectively reduce manufacturing overhead and increase business profits

Thus, manufacturing overhead (SXC) is one of the key factors affecting a company’s product cost and profitability. Therefore, reducing this cost is an effective solution to help businesses achieve higher profits. Some ways to reduce manufacturing overhead that businesses should apply include:

- Enhance cost management by building a strict, scientific management system to effectively track, analyze, and control manufacturing overhead.

- Optimize the production process to minimize waste of raw materials, time, and labor. For example, use energy-saving equipment, improve the lighting system, manage energy consumption, etc.

- Invest in training and upskilling employees to help increase labor productivity and reduce labor costs.

- Consider in-house production of necessary products and services instead of outsourcing, while always being ready to seek and select better suppliers.

- Strengthen warehouse management, avoid excessive inventory, and perform regular maintenance and repairs on equipment and machinery to minimize unexpected repair costs.

- Apply modern technology to production and business to automate processes, increase labor productivity, and reduce manufacturing overhead.

Among them, 1Office’s revenue and expenditure management software is a comprehensive financial management solution. 1Office helps businesses easily track and control revenues and expenditures, including manufacturing overhead costs, allowing managers to implement appropriate measures to improve business efficiency and generate profits.

Experience a free demo of 1Office’s revenue and expenditure management feature today!

Through the article 1Office has just shared, we hope to have helped your business better understand the allocation and planning of manufacturing overhead costs. Additionally, reducing manufacturing overhead costs is a long-term process that requires the effort of the entire workforce. Businesses need to choose solutions that are suitable for their actual situation to achieve the highest efficiency. If you need more detailed advice on the 1Office revenue and expenditure management software, please contact us via:

- Hotline: 083 483 8888

- Facebook: https://www.facebook.com/1officevn/

- Youtube: https://www.youtube.com/@1office-chuyendoisodn