6 Steps to Build a Risk Management Process for Your Business

In the face of unpredictable changes in the business environment, risk management acts as a shield, protecting the enterprise from both internal and external factors. However, the current risk management process in many businesses is still very “rudimentary,” leading to lax control and unnecessary damages. To help businesses better and more clearly understand the nature and implementation of an optimal risk management process, 1Office provides the necessary knowledge in the article below.

Mục lục

1. What is a risk management process? The importance of risk management in a business

A risk management process is the process of planning and implementing measures to respond to unforeseen situations that could hinder or damage a company’s business operations, with the aim of preventing and minimizing losses.

The risk management process acts as a solid line of defense for the business to operate and grow stably. Business risk management not only helps protect existing values but also creates opportunities to generate new ones. Specifically:

- Maintains the stability of business operations.

- Ensures safety and security for the organization.

- Protects the business from damage to assets, resources, and personnel.

- Reduces the costs of rectifying consequences caused by risks.

- Creates conditions for the business to develop and compete sustainably in the market.

- Assists leadership in predicting potential threats to formulate effective business strategies.

| Read more: What is Financial Risk? Solutions to Prevent and Handle Risks |

2. Common Types of Risks in Business

For the risk management process to be effective and ensure the smoothness of the business management process, managers need to identify the form of risk based on specific signs to have appropriate risk handling plans. There are many different criteria for classifying business risks, but typically, risks are grouped into the following 3 categories:

2.1. By Source of Risk

- Internal Risk: Risks arising from factors within the business’s own operations, such as human resource risks, financial risks, business strategy risks, etc. Most of the causes of this risk stem from the management capabilities of the leadership team.

- External Risk: Risks influenced by factors from the external objective environment, which are beyond the control of the business, such as economic risks, market risks, legal risks, etc.

2.2. By Scope of Impact

- Systematic Risk: A type of risk that, when it occurs, affects the entire economic system and all related businesses. This risk reflects the general state of the domestic or global economy and can arise from political instability, changes in trade policies, the integration status of countries, etc.

- Unsystematic Risk: This is a risk that only affects the operations of a single business or a specific industry without causing losses to other entities. This type of risk can be identified in the manager’s capabilities, changes in industry policies, and the correlation between competitors in the same industry.

2.3. By Nature of Risk

- Non-Financial Risk: Risks related to the business environment, such as political, socio-cultural, natural, and scientific-technological factors.

- Financial Risk: This type of risk is related to financial depreciation, such as inflation and currency devaluation. This risk is also influenced by how financial decisions impact the company’s profitability.

| Read More: Risks in HR Management and How to Mitigate Them |

3. 6 Steps to Standardize the Business Risk Management Process

Step 1: Establish the context

In the first step of the risk management process, the manager must identify the context and business environment for implementing the company’s strategies. This will help identify the objectives of the risk management activities and define the scope for risk treatment.

Step 2: Identify risks

This is the process of identifying risks that could affect the achievement of the company’s strategic objectives. To thoroughly review all potential risks, managers need to define at-risk groups and identify risks by their indicators to avoid omissions.

To do well in this step, you will need to answer the following questions:

- What could happen?

- How could it happen?

- Why could it happen?

Step 3: Classify risks

After identifying the risks, they need to be classified into smaller groups with similar characteristics, as mentioned above. This process will help the business develop appropriate solutions to handle each group of risks.

Step 4: Assess risks

In this step, the manager needs to determine the likelihood and impact of the risk on the business. By doing this, you will determine the priority of risk management strategies, which risks are acceptable, and which ones need to be eliminated.

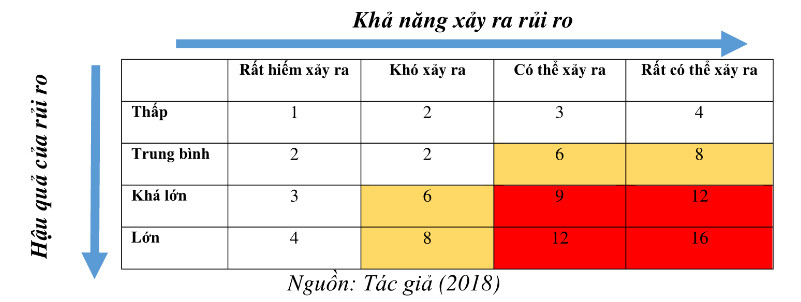

A common risk assessment technique is the 4×4 matrix, corresponding to 4 levels of consequence and 4 levels of likelihood:

After quantifying the criteria, the risks will be classified into 3 levels as shown in the table:

| Risk Level | Assessment Score |

| Low Risk | 1 – 4 |

| Medium Risk | 6 – 8 |

| High Risk | 9 – 16 |

Step 5: Risk Treatment

After assessing the significance of the risks, it is necessary to propose specific solutions and actions to address and control them. Arguably, this is the most critical stage that determines the implementation direction and effectiveness of risk management.

There are 3 common control methods applied to handle risks, including:

- Preventive Control: this activity is used to prevent unwanted incidents from occurring. For example, restricting access to prevent information leaks.

- Detective Control: is the task of monitoring activities/processes to identify shortcomings in preventive controls and devise appropriate response plans.

- Corrective Control: is a control implemented to identify errors that have already occurred in order to take timely corrective action.

Step 6: Monitoring and Reporting

Risks are always evolving and changing continuously; therefore, even after controls are in place, businesses still need to track and monitor changes in these risks. Additionally, it is necessary to evaluate the effectiveness of the risk control methods used to learn from experience and improve the risk management process for greater efficiency.

| Read more: What is a Bottleneck? 4 Ways to Quickly Identify Bottlenecks in Your Business |

4. Standardize the business risk management process with 1Office

To optimize the risk management process and minimize unexpected losses for the business, a process management software is an effective tool that helps managers identify and assess risks, and implement timely solutions.

1Office is a solution that helps businesses build a systematic and professional risk management process with smart features such as:

- A system of continuous, visual reports to monitor the business overview and details of each department from multiple aspects: personnel fluctuations, revenue, and costs

- Conduct business asset inventory, assign permissions to each individual and specific department, easily look up asset status, and prevent losses

- Smart alerts to remind personnel of tasks and track contract expiration dates for employees and partners

- Manage and monitor processes, promptly identify and resolve process bottlenecks to prevent incidents

- Monitor personnel’s work progress anytime, anywhere in real-time

Through this article, 1Office hopes we have provided our readers with useful information about the risk management process and solutions to optimize risk management within your business. To experience the 1Office software, please register for a free consultation here:

For more details, please contact:

- Hotline: 083 483 8888

- Fanpage 1Office: https://www.facebook.com/1officevn

- Youtube Channel: https://www.youtube.com/c/1OfficeNềntảngquảnlýtổngthểDoanhNghiệp