5 Effective Accounting Department Organizational Models for Businesses

Organizing the accounting department is a constantly changing process that needs continuous monitoring to ensure it aligns with the business’s development. Whether you are a small business or a large corporation, building and maintaining an effective accounting system will determine the financial success of that organization. So, how do you establish an effective organizational model for the accounting department? What are the legal regulations regarding the organization of the accounting department? All will be answered by 1Office in the article below. Follow along now!

Mục lục

- 1. What is organizing the accounting department?

- 2. How is the organization of the accounting department regulated?

- 3. The Importance of an Accounting Department Structure in a Business

- 4. 5 Common Models for Accounting Department Structures

- 5. What are the bases for building a suitable accounting structure for a business?

- 6. How do accounting structures differ in large and small businesses?

- 7. Common challenges in organizing an accounting structure

- 8. Frequently Asked Questions

- 9. Effectively manage the accounting department with supporting software

1. What is organizing the accounting department?

The accounting department (also known as the accounting system) is a term used to refer to the collection of accounting personnel, tools, equipment, processes, and resources related to accounting activities within an organization. It includes the methods and procedures for collecting, processing, controlling, recording, and reporting financial and accounting information.

Organizing the accounting department is the process of arranging and allocating human resources to build an accounting system that suits the operational scale and management requirements of each business. This task requires leaders to clearly define the structure and roles of departments, job titles, and responsibilities of each member within the accounting department.

The organizational structure of the accounting department is usually built based on revenue, personnel size, business type, complexity of work, and the specific requirements of the organization. However, a complete accounting system will include the following positions:

- Chief Accountant

- General Accountant

- Accounts Payable/Receivable Accountant

- Internal Accountant

- Tax Accountant

- Sales Accountant

By ensuring that accounting activities are carried out accurately and effectively, businesses can create transparency, reliability, and sustainability in their finances, while also creating favorable conditions for long-term development and success.

>> Read more: The Matching Principle in Accounting: Concept, Content, and Application Examples

2. How is the organization of the accounting department regulated?

The organization of the accounting department in businesses and organizations is governed by legal regulations related to the accounting field. Below are some common regulations concerning the organization of the accounting department:

2.1 How is the organization of the accounting department regulated by law?

Pursuant to Article 49 of the 2015 Law on Accounting, the regulations on organizing the accounting department are as follows:

- An accounting unit must organize an accounting department, appoint accountants, or hire accounting services.

- The organization of the department, appointment of accountants, chief accountants, persons in charge of accounting, or the hiring of accounting and chief accountant services shall be implemented in accordance with the Government’s regulations.

In addition, pursuant to Article 18 of Decree 174/2016/ND-CP, the organization of the accounting department in a business is also clearly regulated. Below is a summary of this article:

- The accounting department must have a sufficient number of accountants appropriate to the scale of operations, management requirements, and functions of the unit. Accountants may hold other concurrent positions that are not prohibited.

- The organization of the accounting department is decided by the competent authority or the legal representative.

- State budget revenue and expenditure agencies shall organize an accounting department appropriate to their functions and tasks.

- Units using the state budget shall organize their accounting departments according to the budget estimation unit. Provincial and district-level units may share a single accounting department if it complies with regulations.

- Accountants must have professional qualifications in accounting, including appropriate degrees and certificates.

- For chief accountants in the state accounting sector, individuals with 10 or more years of experience as a chief accountant and who meet other conditions may be appointed without requiring a specialized degree.

- Individuals without a specialized degree but who were appointed as accountants before January 1, 2014, may continue to work as accountants but cannot be appointed as chief accountants until they meet the full standards and conditions for a chief accountant.

2.2 Who is not allowed to work as an accountant according to legal regulations?

Article 19 of Decree 174/2016/ND-CP stipulates the individuals who are not allowed to hold accounting positions as follows:

- Individuals specified in Clause 1 and Clause 2, Article 52 of the Law on Accounting.

- Individuals who have a direct family or close relationship with financial-accounting management positions within the same unit (except in certain cases specified by the Government).

- Individuals currently holding positions such as manager, operator, warehouse keeper, cashier, or asset purchaser/seller within the same accounting unit (except in certain cases specified by the Government).

2.3 How are the Chief Accountant and Accountant-in-Charge regulated?

Based on Article 20 of Decree 174/2016/ND-CP, the regulations regarding the appointment and duties of the chief accountant and the accountant-in-charge in an organization are defined, including the following main points:

- An accounting unit must appoint a chief accountant, with some exceptions. If an immediate appointment is not possible, the unit must assign an accountant-in-charge for a maximum of 12 months.

- For micro-enterprises or in certain state accounting cases, a chief accountant is not mandatory; an accountant-in-charge is sufficient.

- The term of appointment for a chief accountant or accountant-in-charge is 5 years, after which the reappointment process must be carried out.

- When changing the chief accountant or accountant-in-charge, a handover of work is required, and relevant departments must be notified.

- The Ministry of Home Affairs will provide guidance on matters related to chief accountants and accountants-in-charge in the state accounting sector.

>> See more: Chief Accountant Appointment Form: Regulations, Process with Downloadable Template File

3. The Importance of an Accounting Department Structure in a Business

The accounting department structure is an indispensable part of building and maintaining a company’s financial operations. It plays a crucial role in ensuring the stability and continuity of the accounting and financial system, while also helping the business achieve its strategic goals effectively.

Cost Control and Management Support: By tracking and analyzing revenues and expenditures to optimize resource utilization, it helps managers make smart and effective business decisions.

Example: The accounting department analyzes the company’s procurement invoices and proposes cuts to unnecessary expenses for equipment, research activities, travel, etc., to minimize business inputs and optimize profits.

Support for Business Operations: Providing financial information and reports helps the business monitor and evaluate business performance, identify strengths and weaknesses, and implement appropriate improvement measures.

Example: The accounting department analyzes profit and loss statements, allowing the business to evaluate revenue and profit per product and make decisions to enhance or adjust business strategies.

Internal Control and Risk Prevention: It helps the business establish and implement an internal control system, from defining processes, regulations, and policies to monitoring and evaluating accounting activities. This helps minimize the risk of fraud, accounting errors, and non-compliant behavior.

Example: A manager proposes segregating accounting duties, restricting access to financial data, and conducting periodic audits to prevent fraud or accounting errors.

Ensuring Stability and Continuity: An organized accounting department ensures that accounting processes are completed on time and that financial reports are prepared and provided promptly. This helps the business comply with legal regulations and the requirements of stakeholders.

Example: The accounting department structure ensures that tax reports are filed by the deadline, helping the company comply with the law and avoid penalties.

4. 5 Common Models for Accounting Department Structures

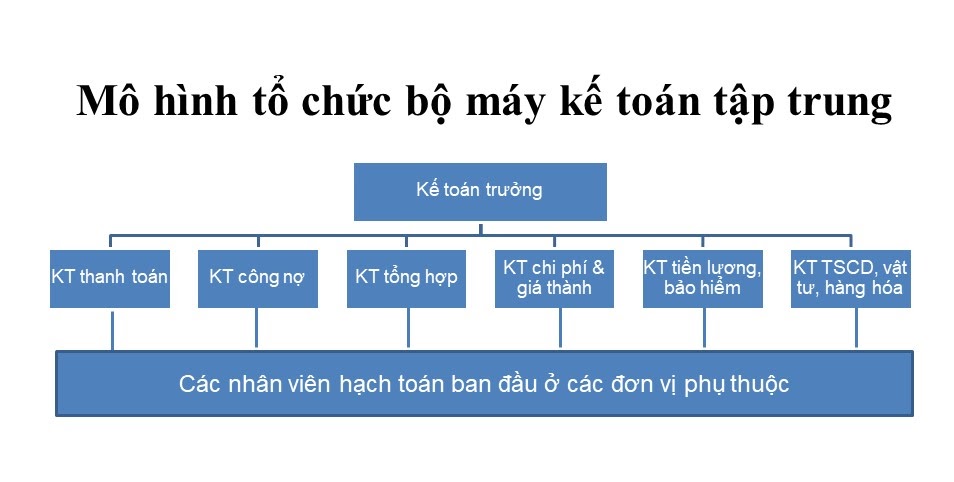

4.1 Centralized Accounting Department Organizational Model

In this centralized accounting department model, accounting and financial activities are concentrated and performed at a main accounting center and there are no accounting departments in the subsidiary units. All financial and accounting information from the subsidiary units is sent to the center for processing and reporting. The accounting center is responsible for standardizing accounting processes and policies, and ensuring the consistency and efficiency of accounting operations.

| Advantages | Disadvantages |

|

|

The centralized accounting organizational model is suitable for most types of businesses, especially for businesses whose accounting activities require high synchronization and centralized management. Additionally, even units with multiple branches, subsidiaries, or member units can apply this model. It helps increase consistency and comprehensive control over accounting, while optimizing the use of human resources and resources.

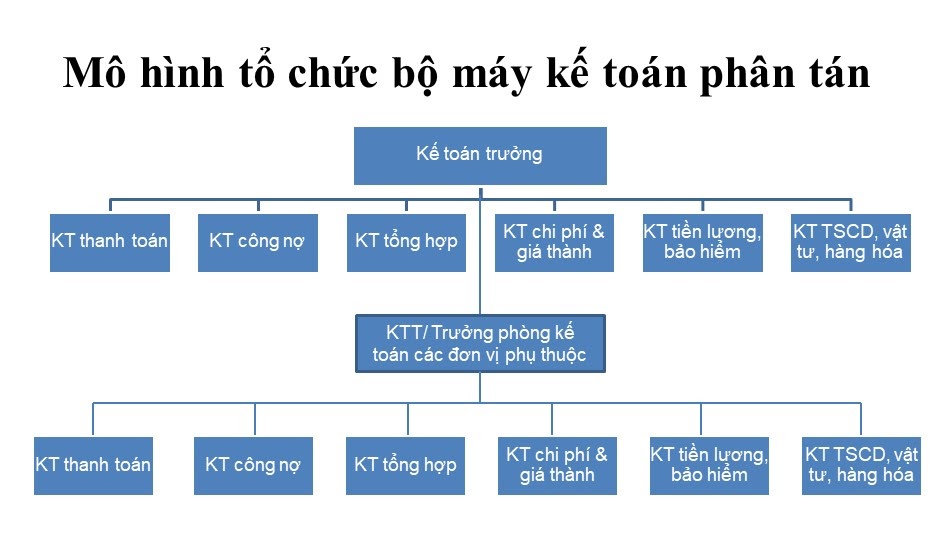

4.2 Decentralized Accounting Structure Model

The decentralized accounting structure model usually distributes accounting and financial activities to each subsidiary, branch, or office. This model is decentralized into a central accounting department and subordinate accounting units. Each unit has its own accounting department and is responsible for its financial and accounting management. At the same time, subsidiaries have the autonomy to manage their own accounting activities.

| Advantages | Disadvantages |

|

|

The decentralized accounting organizational model is often applied in:

- Accounting activities that require proximity and flexibility at each separate business unit.

- Large-scale enterprises with extensive business areas, multiple branches, and a dispersed structure.

- Enterprises with complex business structures, including various types of businesses and different industries.

- Organizations with many constituent base units that are all dependent on a single economic legal entity.

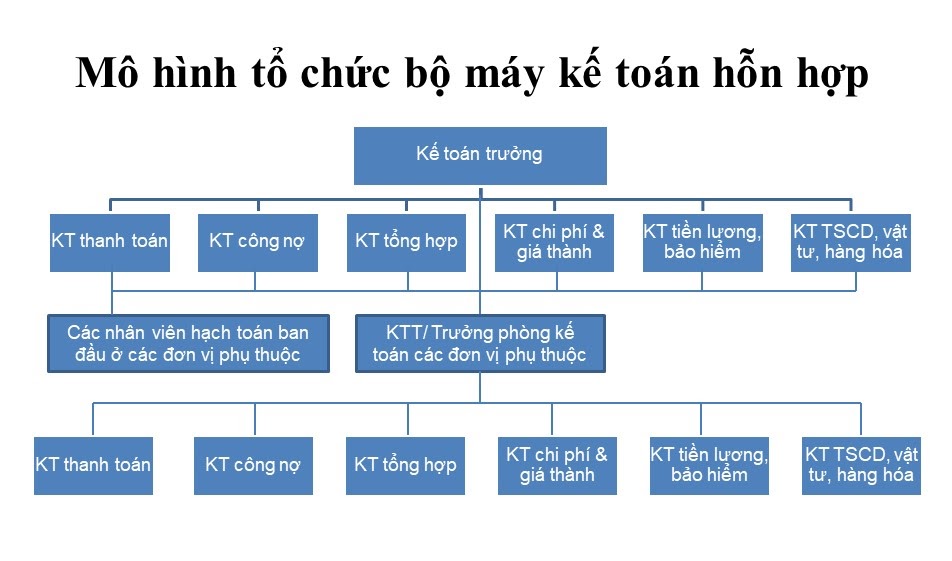

4.3 Hybrid Accounting Department Organizational Model

The hybrid accounting department model, also known as the combined centralized and decentralized model, is characterized by having a main accounting center but also subsidiary units or accounting departments at different locations. The accounting center is responsible for managing and guiding the subsidiary units, while the subsidiaries have autonomy in carrying out their specific accounting activities.

| Advantages | Disadvantages |

|

|

The hybrid accounting organizational model is often applied in various types and sizes of businesses, such as:

- Accounting activities that require a balance between centralization and flexibility at each business unit.

- Large or global-scale enterprises with many branches, subsidiaries, and complex business operations.

- Multinational or international-scale enterprises with numerous financial and accounting activities that need to be managed and controlled comprehensively and consistently.

- Medium or large-sized enterprises with multiple branches, offices, or subsidiaries.

- Businesses that need an accounting organization that ensures consistency and comprehensive centralization while also being flexible and responsive to the specific accounting issues of each unit.

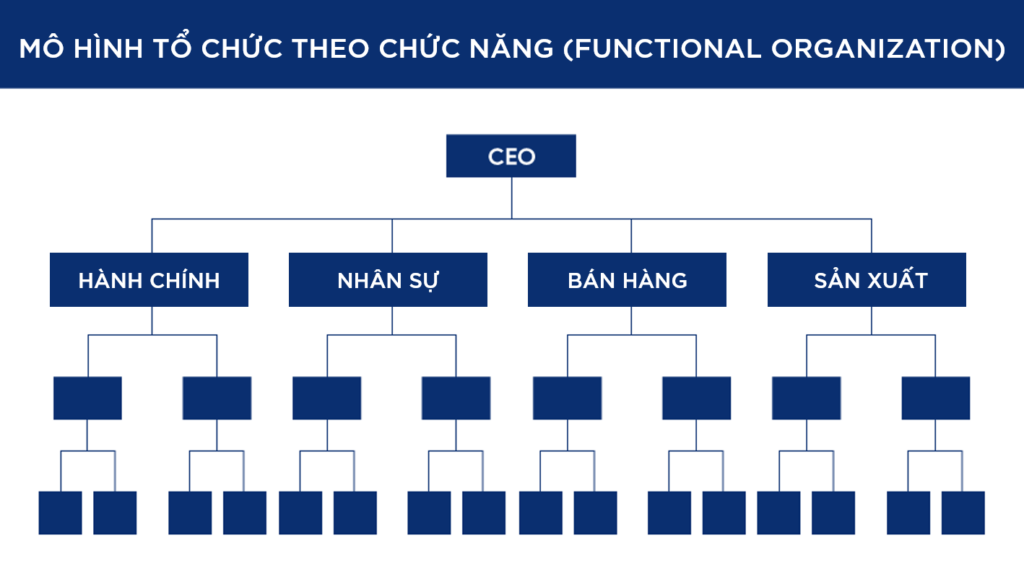

4.4 Functional Accounting Organizational Model

In the functional accounting organizational model, the accounting department is organized based on specific job descriptions and functions. For example, management accounting, financial accounting, cost accounting… each department is responsible for a specific area of accounting.

| Advantages | Disadvantages |

| Each accounting department is responsible for a specific function such as fixed assets, capital, taxes, etc., which helps focus expertise and improve work quality. | Lacks a holistic view due to excessive focus on separate functions, leading to a disconnection between different parts of the accounting process. |

This model is suitable for: Large and complex enterprises where many aspects of accounting require deep expertise. Specifically, businesses in industries such as banking, insurance, healthcare, etc. The functional accounting model helps optimize the efficiency and quality of accounting work in each specific area.

4.5 Accounting Organizational Model by Industry

The accounting organizational model by industry focuses on the accounting requirements and specific regulations of each industry. Some industries include: manufacturing, real estate, banking and finance, information technology, etc., in which accounting departments specialize in specific industries and apply appropriate accounting procedures. Below are the pros and cons of this model:

| Advantages | Disadvantages |

| The accounting system is built on an in-depth understanding of a specific industry, enabling it to grasp the unique requirements and regulations of that sector. | By focusing too heavily on a specific industry, this model can limit the ability to diversify and expand accounting operations into other sectors. |

The industry-specific model is suitable for businesses operating in specific industries with their own accounting regulations, such as construction, information technology, etc. This model helps meet specific accounting requirements and comply with industry regulations.

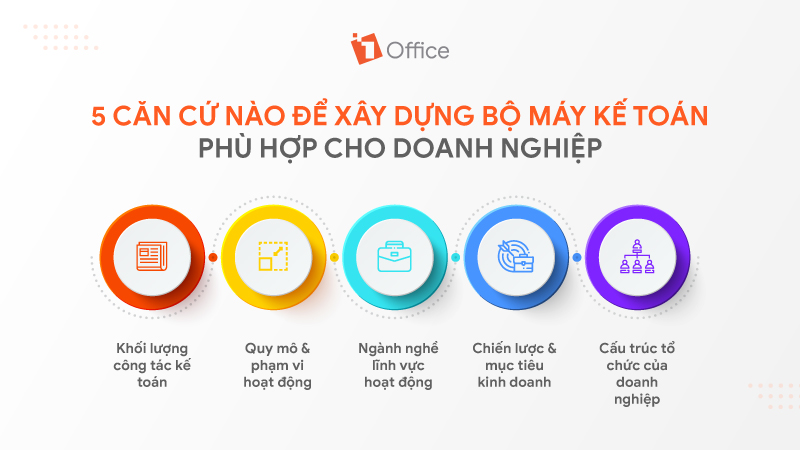

5. What are the bases for building a suitable accounting structure for a business?

Volume of accounting work: This includes the accounting tasks required in the process of collecting, recording, checking, controlling, and reporting information. Based on the volume of accounting work, the business can determine the number and type of accounting personnel needed, and assign tasks and responsibilities for each position within the accounting structure.

Scale and scope of business operations: The size and scale of the business will affect the structure and organization of the accounting department. The business needs to determine the necessary number of accounting staff and corresponding management positions.

Industry of operation: Each industry has its own accounting requirements and regulations. Therefore, it is necessary to consider industry regulations and specific accounting requirements to build a suitable accounting structure.

Business strategy and objectives: The accounting structure must be designed to support the achievement of the business’s goals and strategies. It must be able to provide accurate and timely financial information to support business decisions.

Organizational structure of the business: For businesses with multiple branches, subsidiaries, or international operations, it is necessary to consider centralized, decentralized, or hybrid accounting models to ensure consistency and control over accounting activities.

6. How do accounting structures differ in large and small businesses?

The organizational structure of the accounting department depends directly on the scale and specific operations of the business. Small and large businesses have distinct differences in how they build, operate, and manage their accounting systems.

Characteristics of the accounting structure in small businesses:

- Lean structure: Usually, there are only a few accounting staff members in charge of multiple areas simultaneously (taxes, payroll, expenses, accounts receivable/payable…).

- Cost-optimized: Limited personnel and tools, prioritizing cost savings.

- Multitasking: The chief accountant or person in charge of accounting often handles multiple management and execution tasks.

- Limited specialization: Lack of detailed task assignment leads to risks of errors or lack of control.

Characteristics of the accounting structure in large businesses:

- Hierarchical structure: There are multiple specialized accounting departments/divisions for each area (general accounting, accounts receivable/payable, inventory, cost accounting, taxes…).

- High specialization: Personnel handle specialized tasks, reducing errors and improving efficiency.

- Technology application: Often integrates ERP and modern financial management software to handle large volumes of data.

- Enhanced control: Multiple layers of checks and approvals ensure transparency and legal compliance.

The accounting structure of a small business is flexible but lacks depth, while that of a large business is professional and rigorous but has high operating costs. Businesses need to choose a model that suits their capabilities and development goals.

7. Common challenges in organizing an accounting structure

Organizing an accounting structure may seem like just assigning personnel, but in reality, it presents many difficulties, especially as businesses must balance legal compliance, cost optimization, and management efficiency.

Common challenges:

- Lack of specialized personnel: Small businesses often find it difficult to recruit experienced chief accountants.

- Improper task assignment: Personnel have to handle multiple jobs, which can easily lead to errors and high pressure.

- Lack of transparency: Loose accounting processes can lead to fraud and losses.

- Limited technology application: Businesses have not invested in software systems, resulting in manual and inefficient data processing.

- Complex legal compliance: Accounting and tax regulations change constantly, making it difficult for the accounting department to stay updated.

To overcome these challenges, businesses need to build transparent processes, train personnel, apply technology, and regularly update legal regulations. This is the key to ensuring the accounting structure operates stably, reduces risks, and supports long-term development strategies.

8. Frequently Asked Questions

Do small businesses need a separate accounting department?

Not necessarily. For small businesses with few documents and simple transactions, starting with 1–2 accounting staff or outsourcing is a viable option. As the business scales up, generates more transactions, and requires tighter internal controls, it should then consider establishing a separate accounting department.

What is a reasonable size for an accounting department?

There is no fixed number for every business. The appropriate size depends on revenue scale, number of documents, operating model, number of branches, and the complexity of financial operations.

How should a multi-branch business organize its accounting?

Multi-branch businesses should typically organize with a centralized management approach, having unified processes and data across the entire system. Each branch can handle on-site operations, but consolidation, control, and reporting should be synchronized to a single point to minimize data discrepancies.

Is managing the accounting department with Excel still suitable?

Excel is no longer suitable. As the number of documents increases, multiple people handle them, and coordination between departments is needed, Excel reveals its limitations, such as being prone to errors, difficult version control, and time-consuming consolidation. At this point, businesses should consider using software for more effective management.

Who holds a higher position: Chief Accountant or Head of Accounting?

The Chief Accountant. In a business, the Chief Accountant is a position with higher professional responsibility than the Head of Accounting because they are responsible for organizing and controlling all accounting activities and approving related matters according to regulations.

9. Effectively manage the accounting department with supporting software

In general, building a specialized accounting model suitable for each type of business can present many difficulties and potential risks. If a business sets up an unsuitable model, it can lead to an inefficient accounting department, causing difficulties in financial reporting and thereby affecting business operations.

To solve this problem, HR planners need a clear human resource planning strategy and should use supporting software. Among them, 1Office Human Resource Management software is an excellent solution that helps businesses effectively manage human resources and the accounting department.

Proud to be one of the HR Management software trusted by over 5,000 businesses, 1Office software supports businesses in: creating recruitment processes, digitizing employee records, centralizing information storage, visually assessing competencies, evaluating KPIs effectively… all on a single platform.

Contact 1Office now for a consultation and to experience the Human Resource Management feature completely free of charge. We wish your business success!

- Hotline: 083 483 8888

- Facebook: https://www.facebook.com/1officevn/

- Youtube: https://www.youtube.com/@1office-chuyendoisodn