What is Contribution Margin? Calculation Formula and Applications

To accurately assess a company’s financial health, the contribution margin is a crucial and useful metric that allows investors and managers to understand and compare the profitability of each product or service. Additionally, the contribution margin is a standard measure for evaluating a company’s ability to manage operating costs and generate profit. Join 1Office to learn more about what a contribution margin is in this article.

Mục lục

1. Overview of Contribution Margin

Contribution Margin is a key indicator in financial analysis that helps businesses clearly understand the relationship between revenue, costs, and profit. It serves as a foundation for determining which products or services are truly contributing to profit after deducting variable costs. A firm grasp of this concept helps managers make optimal decisions regarding product mix, pricing, and business strategy.

1.1. Definition

1.1.1. What is a contribution margin?

Contribution margin, also known as marginal profit, is the metric that represents the difference between revenue (selling price) and variable costs. In other words, the contribution margin is the portion of revenue remaining after variable costs have been deducted. This metric indicates how much profit a company retains to cover its fixed costs.

The contribution margin is typically calculated per product unit, per product line, or for all of a company’s product types.

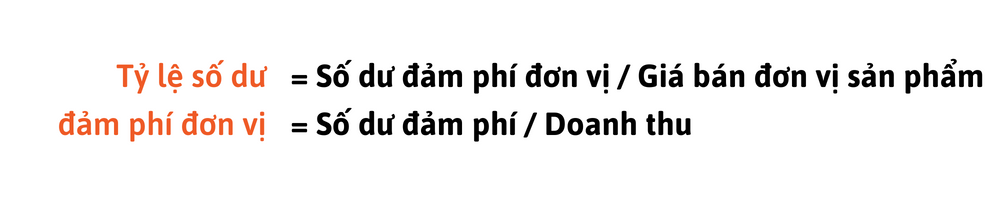

1.1.2. What is the contribution margin ratio?

Additionally, a related metric to the Contribution margin is the Contribution margin ratio. This ratio indicates the relationship between revenue and contribution margin, meaning for every dollar of revenue generated, it shows how many dollars of contribution margin the company earns.

1.2. Differentiating Contribution Margin and Gross Margin

Besides Contribution margin, Gross margin is also a frequently used metric to assess a company’s profitability. However, the purposes of these two metrics are entirely different, so they must be clearly distinguished to avoid confusion.

Gross margin shows the profit retained after deducting costs directly related to production (cost of goods sold) from revenue. Meanwhile, the Contribution margin measures the profit after deducting variable costs.

| Contribution Margin | Gross Profit Margin |

|

|

To learn more about Gross profit margin, its calculation formula, and its practical applications, read our article:

What is Profit Margin? How to Accurately Calculate the 3 Types of Profit Margins

1.3. What is the significance of Contribution Margin?

The Contribution Margin metric is used to assess a company’s financial ability to cover fixed costs and serves as a basis for generating profit. Analyzing the Contribution Margin can provide the following insights:

- If Contribution Margin = 0: The revenue generated is just enough to cover fixed costs, the business has reached its break-even point, and the company is neither making a profit nor incurring a loss.

- If Contribution Margin > 0: The company has sufficient ability to cover fixed costs and can generate a profit from selling its products.

- If Contribution Margin < 0: The company is operating at a loss because the revenue generated is not enough to cover fixed costs.

2. How to Calculate Contribution Margin and Examples

To fully understand the nature of contribution margin, businesses need to grasp its calculation formula and practical application. Accurate calculation not only helps in evaluating the performance of individual products but also aids in determining the break-even point, planning for profits, and financial forecasting. This section will provide specific illustrations with detailed examples to help you easily apply it to your actual business operations.

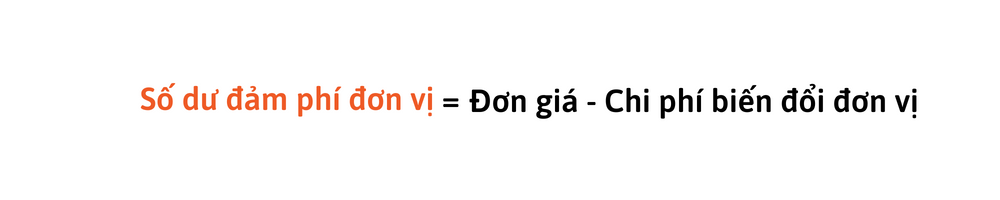

2.1. Contribution margin per unit

Contribution margin per unit is the contribution margin calculated for a single product unit, showing how much one unit contributes to covering the company’s fixed costs. Calculating the contribution margin per unit helps managers determine the sales volume needed to cover fixed costs and achieve the desired profit level.

Formula

Example

Company X sells product A for 80,000đ/product, and the variable cost per unit is 20,000đ. Therefore, the contribution margin per unit for one product can be calculated as: 80,000 – 20,000 = 60,000đ

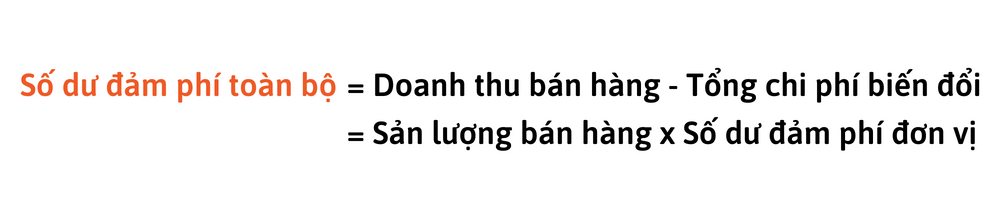

2.2. Total Contribution Margin

Total contribution margin is used to calculate for all types of goods and products within the company, helping managers get the most comprehensive overview of the overall business and production situation.

Formula

Example

In the case mentioned above, if company X sells 1,000 units of product A during the period, the total contribution margin for all products sold would be: 1,000 x 60,000 = 60,000,000đ

2.3. Contribution Margin Ratio

Formula

From the example above, the Contribution Margin Ratio can be determined as = 60,000 / 80,000 = 0.75 = 75%

3. Applications of Contribution Margin

3.1. Basis for selecting the product mix

For businesses with a diverse product portfolio, the most difficult problem for managers is how to allocate resources across all product lines most reasonably and effectively within limited production capacity. In this case, the contribution margin will be used to evaluate each product category to determine which products should be prioritized for production.

For example, if the contribution margin of item A is higher than item B, item A will be prioritized for resource allocation in production due to its higher profit potential.

3.2. Basis for pricing decisions

Product pricing decisions always play a strategic role in business operations, so they must be carefully considered and based on scientific grounds. Businesses will rely on the contribution margin to determine a reasonable selling price for the product, one that can both cover the costs incurred and generate the desired profit.

3.3. Basis for eliminating or retaining a product line

In reality, not every department or business item can bring profit to the company. In such cases, managers will face a difficult decision: whether to eliminate or retain that product line. If they simply think that discontinuing the item will remove the cost burden it causes, they may very well make the wrong decision.

The truth is that when an item is removed from the product portfolio, only the direct costs incurred for that product line are reduced. Meanwhile, the common costs that serve the entire production operation are not only not cut but must also be shared among the remaining products, causing the cost of these products to be inflated.

Therefore, managers need to consider carefully based on the segment contribution margin and place it in relation to other fixed costs to make the wisest decision.

3.4. Basis for raising investment capital

Contribution margin is also one of the indicators that investors and stakeholders use when considering funding. This is the basis for recognizing and evaluating a company’s capabilities through how it covers its operating costs.

A higher contribution margin means the company has greater strength and potential, generating more profit. A low contribution margin is common in labor-intensive industries such as manufacturing because variable costs account for a large proportion of revenue. Meanwhile, a high contribution margin is often seen in capital-intensive sectors.

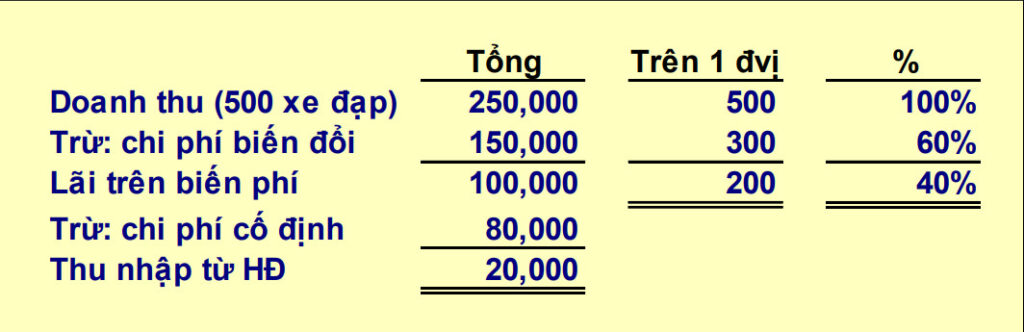

4. How to prepare an income statement based on contribution margin

Contribution margin is a key indicator for preparing a company’s internal financial reports. Therefore, after understanding what contribution margin is and how to apply this indicator in business, the next problem for managers to solve is preparing an income statement based on contribution margin.

To prepare a business performance report based on contribution margin, managers need to gather all relevant information regarding sales for the period, product costs, variable costs, and fixed costs.

After collecting the necessary financial data, the report preparer will calculate the contribution margin index according to the given formula to include it in the income statement.

Example of a contribution margin income statement for a bicycle retailer with sales of 500 bicycles during the period:

5. Factors affecting Contribution Margin

Contribution Margin is an indicator that reflects the contribution of revenue after deducting variable costs, used to cover fixed costs and generate profit. This indicator is not fixed but is influenced by many operational and strategic factors within the business.

Below are the most important factors:

5.1. Selling price of products or services

The selling price is a variable that directly impacts the contribution margin. When a business increases the selling price while variable costs remain unchanged, the Contribution Margin will increase accordingly. However, price adjustments need to consider the reaction of the market and customers—because if the price increases too much, it may reduce sales volume, causing the total contribution margin to decrease.

5.2. Variable costs

Variable costs include raw materials, direct labor, sales commissions, shipping costs, etc. If variable costs increase while the selling price remains unchanged, the contribution margin will decrease.

Therefore, optimizing production processes, negotiating with suppliers, or applying automation technology to reduce variable costs are direct ways to improve this indicator.

5.3. Product Mix and Goods Portfolio

Different products often have different contribution margin levels. A business that focuses more on product groups with a high contribution margin will improve its overall CM.

Conversely, if revenue comes from items with a low CM, even with high sales volume, the overall profit will not improve significantly.

5.4. Labor Productivity and Production Efficiency

Efficiency in the production, distribution, and sales processes affects the variable cost per unit. High labor productivity, less waste, and fewer product defects will help reduce variable costs and increase the unit contribution margin.

5.5. Discount and Promotion Policies

Discount programs, promotions, or trade discounts often reduce the actual selling price, thereby lowering the Contribution Margin.

Businesses need to calculate carefully when applying incentive policies to ensure a reasonable contribution margin ratio is maintained after promotional activities.

5.6. Production Scale and Economies of Scale

As production volume increases, the average variable cost can decrease due to economies of scale (better raw material prices, lower allocated transportation costs, etc.). This helps improve the overall contribution margin and the profit-to-revenue ratio.

6. Solutions to Improve the Contribution Margin

6.1. Improve Revenue

Looking at the Contribution Margin formula, it’s clear that this metric is influenced by two factors: Revenue and Variable Costs. Most businesses typically focus their efforts on improving revenue as this solution offers the most benefits. Common strategies used to increase the contribution margin are upselling and cross-selling.

6.2. Reduce Variable Costs

Variable costs are expenses that fluctuate, changing depending on the scale of production and the quantity of goods and products sold by the business. Unlike fixed costs, variable costs are a factor that businesses can control and adjust flexibly to suit their operational needs and production capacity. Therefore, a company can consider cutting the variable costs spent on producing and selling products by considering alternatives, such as using cheaper raw materials or changing suppliers.

6.3. Consider Increasing Prices

The final and also most difficult method for a business wanting to improve its Contribution Margin is to increase product selling prices. A price increase will lead to higher sales revenue, which in turn increases the Contribution Margin.

However, businesses must consider carefully before deciding to raise prices, as it can easily lead to negative reactions from customers or, more seriously, the risk of loyal customers abandoning the brand.

6.4. Apply Technology to Effectively Solve Corporate Financial Challenges

To build a healthy business with a strong financial foundation, in addition to applying financial metrics, managers need tools to control and manage cash flow scientifically and systematically. Currently, more and more businesses are turning to technology solutions to optimize overall operations and financial management in particular.

1Office is one of the most outstanding business financial management software on the market. The software provides a comprehensive solution for businesses to manage revenue and expenditures in a synchronized and unified manner, helping to save time and costs in work processing with outstanding features such as:

- Automatically compiles reports on the company’s revenue and expenditure situation

- Revenue and expenditure data is automatically calculated into other features on the software (sales, accounts receivable,…)

- Controls all company expenditures, preventing loss and fraud

Our article above has provided an understanding of what contribution margin is and also presented a 4.0 business financial management solution to help managers master cash flow and make the most effective business decisions. To experience the number 1 business management software on the market, please contact us using the information below.

For more detailed information, please see:

- Hotline: 083 483 8888

- Fanpage: https://www.facebook.com/1officevn/

- Youtube: https://www.youtube.com/channel/UCeTIRNqxaTwk0_kcTw6SxmA

Related keywords: what is contribution margin, contribution margin