What is the Cost of Capital? Formula and Detailed Calculation

To achieve effective financial management, minimizing the cost of capital is the key to success. It is closely related to the opportunity cost of investing cash in specific business projects and investments. In this article, let’s explore the cost of capital and the most standard and up-to-date calculation methods with 1Office.

Mục lục

- 1. What is the cost of capital?

- 2. Characteristics of the cost of capital

- 3. What factors affect the cost of capital?

- 4. Formula for calculating the cost of capital

- 5. Weighted Average Cost of Capital (WACC)

- 6. Marginal Cost of Capital

- 7. How does capital structure affect the cost of capital?

- 8. The relationship between cost of capital and financial risk

- 9. Frequently Asked Questions

1. What is the cost of capital?

The cost of capital is the rate of return that investors require for the capital a business raises for a specific investment project or business plan. This is a crucial factor representing the opportunity cost for investors, who will carefully consider it before deciding to invest in the business or choose another investment opportunity with more attractive returns.

For example: It includes actual cash costs such as interest paid on debt, dividends paid to shareholders, and opportunity costs like retained earnings.

2. Characteristics of the cost of capital

First, capital is considered a commodity, participating in buying and selling on the market, and its cost fluctuates according to market laws. In other words, this cost does not depend on the subjective decisions of the business but is formed based on the supply and demand for capital in the market.

-

Characteristics of the cost of capital

Second, the assessment of the cost of capital is based on the risk level of the investment project requiring capital. When the project’s risk level increases, the required rate of return for investors also increases, leading to a higher cost of capital. Conversely, when the risk decreases, this cost also decreases.

Third, it is usually measured as a percentage.

Fourth, it includes both an inflation premium and the real interest rate required by investors.

Fifth, it reflects the required rate of return by investors at the present time, not based on their past requirements.

Read more: ROS Index: Formula and Meaning in Financial Statements

3. What factors affect the cost of capital?

Objective factors include:

- Market interest rates: The market interest rate corresponds with the rate of return that investors require and the cost of capital. If market interest rates increase, the required rate of return for investors also increases, leading to a higher cost, and vice versa.

- Corporate Income Tax Rate: The corporate income tax rate affects the calculation of the reasonable cost of debt when calculating taxes. A higher tax rate will reduce the cost of debt capital, and vice versa.

-

Factors affecting the cost of capital

Subjective factors include:

- Investment policy: The risk level of investment projects undertaken by the company directly affects the rate of return required by investors. High-risk projects will demand a higher rate of return, which increases the cost of capital.

- Financing policy: Raising a large amount of debt can increase financial risk, leading to a higher cost of capital for the business. Heavy reliance on debt can put significant pressure on capital sources from investors.

- Dividend policy: The company’s dividend policy decisions affect the amount of retained earnings for reinvestment. If the company decides to reinvest more, it can reduce the need to raise external capital, thus lowering the cost of capital. Conversely, if dividends are high, the company may have to seek other external funding sources, which increases this cost.

See also: What is working capital? Formula and methods for managing working capital

4. Formula for calculating the cost of capital

4.1 Cost of debt

Using debt capital offers a special advantage: the interest paid can be considered a reasonable and valid expense when calculating corporate income tax. Therefore, when assessing the cost of debt, it is important to calculate both the pre-tax and after-tax costs.

- Formula for determining the pre-tax cost of debt

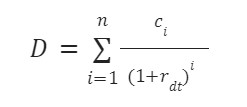

The pre-tax cost of debt is the rate of return required by lenders (also known as creditors), without considering the effect of corporate income tax. The interest rate on the loan represents the cost the business must pay for using this external capital source.

Where D is the debt capital

rdt is the pre-tax cost of debt

ci is the payment (principal and interest) to the creditor (i = 1 →n)

Using the interpolation method, we can determine rdt

-

Cost of debt

- Formula for determining the after-tax cost of debt

According to the Law on Corporate Income Tax, loan interest is considered a valid expense and can be deducted when calculating corporate income tax. The benefit of this is that the loan interest reduces the company’s taxable income. Conversely, dividends paid to shareholders, including preferred and common stockholders, are typically distributed from after-tax profits and therefore do not offer this tax benefit.

To compare the cost of using different capital sources fairly, this comparison is usually made on an after-tax basis, allowing for an evaluation on a level playing field.

It can be recalculated as follows:

Thus, the tax shield is directly proportional to the corporate income tax rate, resulting in a significant reduction in the company’s tax liability.

In practice, the cost of debt is often specified as the interest rate, which is a significant part of the total cost a company must accept when using capital from banks.

4.2 Cost of capital from preferred stock

As mentioned in the previous section, there are many types of preferred stock, but one of the most common forms used by many companies worldwide is dividend preferred stock. The owners of this preferred stock receive a fixed dividend and have no voting rights in company decisions. Dividends from preferred stock are not considered a reduction in the company’s taxable income, unlike common stock. The unique feature of this type of stock is that holders only receive a fixed annual payment and do not benefit from profit growth.

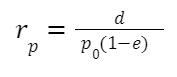

If we let P0 be the current market price of the preferred stock.

e is the issuance cost ratio

d is the dividend per preferred share

Then the cost of preferred stock, rp, is determined as follows:

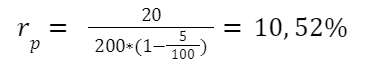

Example: Company X issues preferred stock with a price of 200,000 VND/share and a dividend of 20,000 VND/share. The issuance cost is 5,000 VND/share.

4.3 Cost of retained earnings

Joint-stock companies, as well as other businesses, often use a portion of their after-tax profits for reinvestment. This is an internal source of equity capital, primarily generated from profits from production and business activities. This helps strengthen the company’s internal finances and provides capital for development and expansion projects without having to raise funds externally.

From an accounting perspective, when a company decides to retain earnings for reinvestment, there is no specific fundraising cost to be paid for using this capital source. However, from a financial perspective, it is necessary to consider the opportunity cost of retaining earnings for investors (i.e., the owners).

-

Cost of retained earnings

There are three main methods for estimating the cost of using retained earnings for reinvestment:

- The dividend growth model method

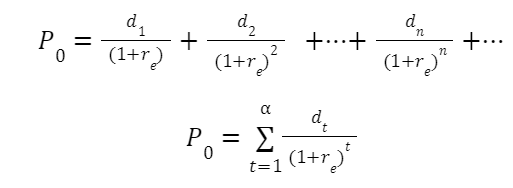

This is a commonly used method. According to the dividend growth model, also known as the discounted cash flow (DCF) method, the price of a common stock is considered the present value of the stream of dividends that an investor expects to receive in the future. The formula to determine this value can be expressed as follows:

Where:

– P0: The current market price of the common stock.

– dt: The expected dividend to be received in year t.

– re: The required rate of return for common stockholders.

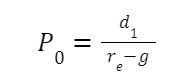

Assuming dividends grow at a constant rate g each year, the stock price is determined by the formula:

Where: + d1 is the expected dividend to be received in year 1

+ g is the expected constant annual growth rate of dividends.

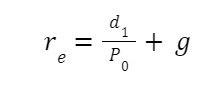

From the formula above, the required rate of return for stockholders, also known as the cost of retained earnings, can be determined by the following formula:

In this method, determining the constant annual dividend growth rate (g) for any future period is not a simple challenge. Typically, for companies that do not make sudden increases or decreases in dividends, investors often rely on the situation and dividend payment data from past years to determine the average dividend growth rate and then make future projections. For companies with fluctuating dividend payments, considering information from securities analysts is also an important means of forecasting.

- The Capital Asset Pricing Model (CAPM) method

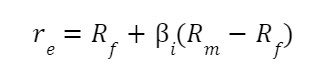

In the Capital Asset Pricing Model, there is a significant correlation between the rate of return required by investors and the risk premium. A common method for determining the cost of retained earnings is to use the Capital Asset Pricing Model (CAPM). This formula can be expressed as follows:

Where:

re: The required rate of return for investors on retained earnings

Rf: The risk-free rate of return (or interest rate), often calculated using the interest rate of government bonds

Rm: The expected market rate of return

i: The beta coefficient, which measures the actual risk of the company’s stock relative to the market portfolio

Example: The risk-free rate (Rf) is 10%, the market rate of return (Rm) is 12%, and the risk coefficient for Company X’s stock is determined to be 1.5. Therefore, the required rate of return for investors in Company X’s stock is: re=10% + 1.5(12%-9%)=14.5%

However, estimating the market risk premium and the company’s stock beta coefficient is not simple in practice. Furthermore, both of these factors often fluctuate over time and depend on various other elements. This makes it difficult to determine them accurately.

Moreover, the CAPM method uses historical statistical data to predict the future. However, economic conditions and financial markets change unpredictably, so relying on the past can lead to inaccurate results in a volatile context.

This poses a challenge for investors and policymakers who have to make decisions based on the CAPM model. The model’s sensitivity to market fluctuations and the uncertainty in its predictions are factors that need to be carefully considered when applying this method for capital asset pricing.

- The bond yield plus risk premium method

The basis of this method is that investors in corporate bonds typically bear less risk than shareholders investing in the company’s stock. Therefore, the required rate of return for shareholders can be determined by adding a risk premium to the company’s bond interest rate. This means that the company’s bond interest rate is proportional to the level of risk, and consequently, the risk premium required by shareholders is also higher. From this, it can be concluded that:

| Cost of retained earnings = Bond yield + Additional risk premium |

The bond interest rate is determined as the bond’s yield to maturity (YTM).

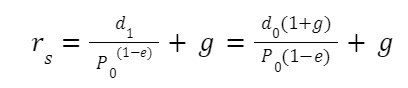

The amount of capital the business uses for investment is equal to the current market price of common stock minus issuance costs (printing, underwriting, brokerage fees, etc.).

Let P0 be the current market price of common stock

e is the issuance cost ratio, then the net price = P0(1-e)

d1 is the expected dividend per common share in the first year

g is the expected dividend growth rate (assuming constant growth)

rs is the cost of new equity

Note: Determining the expected dividend growth rate (g)

Where: b: Reinvestment profit ratio.

ROE0: Return on equity from the previous period

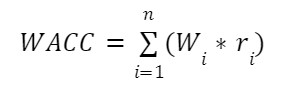

5. Weighted Average Cost of Capital (WACC)

A business can typically raise capital from various sources (e.g., loans, retained earnings, issuing bonds, stocks, etc.). Therefore, calculating the weighted average cost of capital for all sources is crucial. The weighted average method is used, where the weight depends on two main factors: the cost of using each capital source and the proportion of each capital source. The formula for calculating the weighted average cost of capital (WACC) is:

Where: WACC: Weighted Average Cost of Capital

Wi: Proportion of capital source i (i = 1-n)

ri: Cost of capital source i

6. Marginal Cost of Capital

Concept: The weighted average cost of capital for each additional dollar of new capital raised during the same period.

How to determine the break point of the marginal cost of capital curve:

- Each business typically chooses a capital structure based on its access to capital resources, industry characteristics, risk level, and other factors at different times. For example, during the COVID-19 pandemic, a business might maintain its capital size, while in a growth phase, it needs more capital to expand. In both periods, the capital structure may change to reflect the business situation. The goal of every business is to optimize its capital structure.

- An optimal capital structure is one that is safe, financially appropriate, and has the lowest cost of capital. However, in reality, as the demand for new investments increases, the need to raise capital can change, thereby altering the cost of using different capital sources.

- Typically, businesses will start by seeking easily accessible capital sources with a low cost of capital. As they expand and need to raise larger amounts of capital, they may turn to sources that are harder to access, which often comes with a higher cost per unit of capital. This can occur at a specific stage in the company’s development.

- Marginal Cost of Capital

The threshold point from which the cost of new capital begins to rise is called the break point. The break point (BP) is determined by the formula:

Considering and estimating the cost of capital is a crucial aspect for corporate financial managers. This is a critical factor when making decisions about raising capital for investment projects.

7. How does capital structure affect the cost of capital?

Capital structure is the ratio of debt to equity in a company’s total capital. This factor directly influences the cost of capital because each type of capital has a different cost. When a company changes its proportion of debt or equity, the weighted average cost of capital (WACC) also changes accordingly.

If a company increases its debt ratio, the initial cost of capital usually decreases because interest on debt is tax-deductible, creating a “tax shield.” However, when debt becomes too high, financial risk increases, and interest rates are pushed up, causing the overall cost of capital to rise again. Conversely, if a company relies heavily on equity, the cost of capital will be higher because shareholders demand a higher expected rate of return, but the level of financial risk is lower.

In practice, each industry has its own optimal capital structure. For example, the real estate industry often uses a lot of debt to leverage, while the technology industry relies more on equity due to its high-risk nature. The challenge for financial managers is to identify a reasonable balance point where the weighted average cost of capital is lowest while still maintaining the company’s safety.

8. The relationship between cost of capital and financial risk

The cost of capital and financial risk have a close, almost directly proportional relationship. In essence, the cost of capital is the price a business pays to use other people’s money. When financial risk increases, investors and creditors will demand a higher return to compensate for the risk they bear, which in turn increases the cost of capital.

For example, if a company has a good debt repayment history and a moderate financial leverage, its borrowing interest rate will be low, and shareholders will be more confident → the cost of capital decreases. But when a company borrows too much, has unstable cash flow, and an increased risk of bankruptcy, banks will raise interest rates, and shareholders will demand a higher rate of return. As a result, the cost of capital increases sharply.

A clear example is the 2008 financial crisis: corporate lending rates skyrocketed due to widespread default risk, making the cost of capital for most global companies much higher than in stable times.

Therefore, good financial risk management – through controlling debt, maintaining stable cash flow, and building creditworthiness – not only helps businesses become more secure but also reduces the cost of capital, creating a long-term competitive advantage.

9. Frequently Asked Questions

————————

1Office hopes that through this article, businesses, managers, and readers will gain a clearer and deeper understanding of the costs of using capital sources in a business. We hope that with this information, investment and capital mobilization decisions will be made effectively within your organization.