5+ Latest Standard Invoice Adjustment Record Templates (TT78)

In the course of business, discovering errors on invoices is unavoidable. To resolve this issue legally and effectively, businesses need to clearly understand the process of creating an invoice adjustment record according to Circular 78 (TT78). This article will provide you with the necessary information along with the latest standard invoice adjustment record templates for practical application.

Mục lục

- What is an Invoice Adjustment Record?

- Cases requiring invoice adjustment

- Process for creating an invoice adjustment record

- Standard Invoice Adjustment Record Template per Circular 78

- Guide to Filling Out the Invoice Adjustment Record

What is an Invoice Adjustment Record?

An invoice adjustment record (also known as an invoice adjustment agreement) is an official document created between the seller and the buyer to record that an issued e-invoice has errors or changes (discounts, returned goods, incorrect quantity, incorrect unit price, incorrect item name, incorrect Tax ID…).

From June 1, 2025, according to Decree 70/2025/ND-CP and Circular 32/2025/TT-BTC, this record becomes mandatory in most cases of e-invoice adjustments (with a few minor exceptions).

Role of the Adjustment Record

| Purpose | Explanation |

|---|---|

| Record the agreement of both parties | Prove that the buyer has agreed to the adjustment |

| Serve as a legal basis | For the seller to issue a valid adjustment invoice (form 01/ĐC-HĐĐT) or replacement invoice |

| Protection during tax audits | The tax authority will require this record to be presented during an inspection |

| Avoid penalties | No record → a fine of 3–20 million VND (Decree 125/2020) |

Cases requiring invoice adjustment

When does a business need to adjust an invoice?

- Incorrect seller or buyer information: name, address, tax code

- Incorrect economic content of the transaction: unit price, quantity, total amount

- Incorrect tax rate, tax amount: applying the wrong tax rate or miscalculating the tax amount

- Incorrect total payment amount: incorrect amount in numbers or words

- Returned goods: goods do not meet specifications or quality standards

- Discount applied after issuing the invoice: as agreed between the buyer and seller

- Incorrectly issued invoice discovered: but not yet delivered to the buyer

Adjusting invoices helps businesses comply with accounting and tax regulations, avoid legal risks, and ensure accuracy in recording revenue and expenses.

Process for creating an invoice adjustment record

Step 1: Identify the issue to be adjusted

The first and most important step is to accurately identify the issue on the invoice that needs adjustment. This process includes:

- Reviewing the original invoice and comparing it with the actual transaction to detect errors. It is necessary to carefully check information such as: name, address, tax code, item, quantity, unit price, tax rate, and total amount.

- Ensuring all details are re-verified before making adjustments. This may involve checking contracts, purchase orders, delivery notes, or other related documents to confirm the correct information.

- Classifying the error to determine the appropriate form of adjustment: creating an adjustment record or issuing an adjusted/replacement invoice.

Note: According to Circular 78, the deadline for adjusting an invoice is before the tax authority announces a decision to inspect or audit at the taxpayer’s headquarters.

Step 2: Create the adjustment record

After clearly identifying the error, both the buyer and seller will proceed to create an invoice adjustment record with the following content:

- Provide complete information about the original invoice: invoice number, series, date of issue, seller’s/buyer’s tax code.

- Details of the necessary changes: clearly state the incorrect information and the correct information to be adjusted, and the reason for the adjustment.

- Confirmation signatures of the relevant parties: legal representatives of the seller and buyer, chief accountant (if any).

- Distinguish between adjusting information and issuing a replacement invoice:

- For simple information errors (name, address, etc.): only an adjustment record is needed

- For value-related errors (unit price, quantity, tax amount, etc.): in addition to the record, an adjusted invoice must also be issued

The adjustment record must be made in at least 02 copies, with each party keeping one copy for accounting and tax finalization purposes.

Step 3: Send the adjustment record to the partner

After completing the adjustment record, the business needs to notify and send the record to the partner:

- Methods of notification for the adjustment can be:

- Company email (should have receipt confirmation)

- Fax (with successful transmission report)

- Direct delivery (with signed acknowledgment)

- Postal mail (with receipt)

- Deadline for sending the record: It should be sent as soon as possible after discovering the error, preferably no later than 10 working days from the date the record is created.

- Store proof of sending the record to ensure there is evidence to present to the tax authority when necessary.

Step 4: Update data in the accounting system

The final step is to update the adjusted information in the accounting system and tax reports:

- Adjust accounting books and e-invoice software, if any. For e-invoices, follow the procedure of the e-invoice service provider.

- Record the changes in tax reports:

- For the seller: adjust revenue, output tax

- For the buyer: adjust input costs, deductible VAT

- Store the adjustment record along with the original invoice and related documents for future inspections and audits.

Important Notes When Using the E-Invoice Adjustment Record Template

According to Vietnamese law on e-invoices (HĐĐT), an adjustment record is a mandatory document before issuing an adjusted invoice (form 01/ĐC-HĐĐT), especially from June 1, 2025, under Decree 70/2025/ND-CP (amending Decree 123/2020/ND-CP) and Circular 32/2025/TT-BTC. Using an incorrect record template can lead to administrative fines from 3-20 million VND (Decree 125/2020/NĐ-CP). Below are detailed notes, based on guidance from the Ministry of Finance and tax authorities, to ensure legal compliance and avoid risks.

1. Determining When to Create a Record

- Mandatory to create a record: When an invoice has errors affecting tax obligations (incorrect amount, tax rate, tax ID, or goods name not matching specifications/quality) or other details that change the nature of the transaction. From June 1, 2025, it is mandatory to create an agreement record before adjusting/replacing, unless the buyer is an individual (in which case, notification via email/website is sufficient).

- Not mandatory if: The error is only in the name/address/tax ID and does not affect the value/tax (only need to inform the buyer and keep an internal record).

- Note: Incorrect invoices can no longer be canceled – only adjusted or replaced. If multiple invoices from the same month for the same buyer are incorrect, create one consolidated adjustment record + one consolidated adjusted invoice with an attached list (Form 01/BK-ĐCTT).

2. Content and How to Fill Out the Record Template

- Mandatory information: Provide full details for both parties (name, tax ID, correct address, authorized representative), reference the original invoice (number, serial number, issuance date), describe the specific error (e.g., “Incorrect quantity from 100 to 120”), state the reason for adjustment (data entry error, contract change), and include a commitment from both parties (to declare taxes according to the new invoice).

- Number of copies: Prepare 04 copies (or 02 electronic copies), with each party keeping 02 copies of equal legal validity.

- Signature and seal: Must have a handwritten signature + seal of the representatives of both parties (or a digital signature if using software like MISA, MeInvoice). If using a digital signature, attach it to the storage system.

- Note: Clearly state that the adjustment does not change the nature of the transaction (it cannot be used for tax evasion). Use the template from the Appendix of Decree 70/2025/ND-CP to avoid errors.

3. Timing and Procedure (No Delays)

- Deadline: Create the record immediately upon discovering the error, before issuing the adjusted invoice. Send the adjusted invoice to the buyer within 07 days of signing the record (a delay may result in a fine of 4-8 million VND).

- Basic procedure:

- Discover error → Create an agreement record.

- Sign for confirmation → Issue an adjusted/replacement invoice (digitally sign and send to the tax authority if a code is required).

- Send the record + new invoice to the buyer (via email/electronic system).

- Storage: Keep the record + original/adjusted invoices for at least 10 years for tax audits.

- Note: If the tax authority discovers the error first (via notice Form 01/TB-RSĐT), you must handle it within the specified deadline; otherwise, it will escalate to an audit of e-invoice usage.

4. Tax Declaration and Post-Adjustment Processing

- Declaration: The seller records the adjustment in the VAT declaration for the period in which it occurred (no impact if the error does not change the tax amount). The buyer uses the record + new invoice to deduct input tax.

- Special cases: If an address changes due to administrative boundary adjustments (from July 1, 2025), check with the new managing tax authority, but a declaration of change in e-invoice information is not required.

- Note: Keep the record to present during tax audits; if using software (MISA, EasyInvoice), integrated templates can automate the process.

5. Penalty Risks and Tips to Avoid Errors

- Risks: Failure to create a record (fine of 3-5 million VND); repeated errors (double the fine); late submission of the adjusted invoice (fine of 4-8 million VND).

- Tips: Double-check information before issuing an invoice; keep a record template ready; consult the local tax authority for complex cases. Use invoice software with automatic error detection.

Standard Invoice Adjustment Record Template per Circular 78

Below are invoice adjustment record templates for common cases, meeting the requirements of Circular 78:

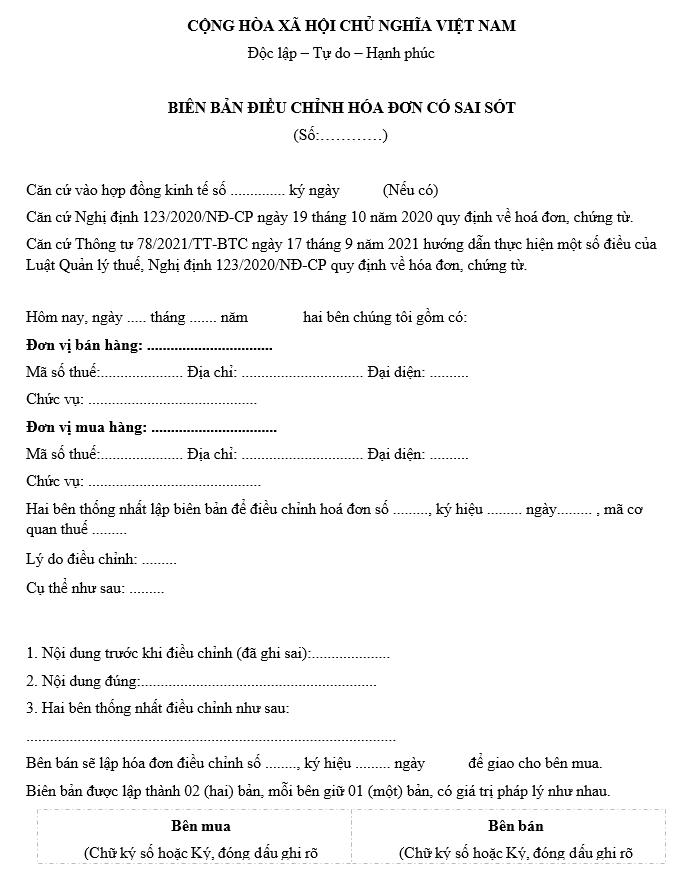

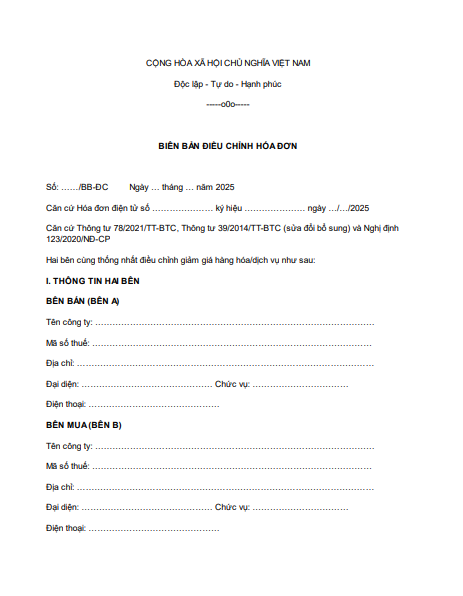

1. Invoice Adjustment Record Template (General Template)

Download the free invoice adjustment record template (general template)

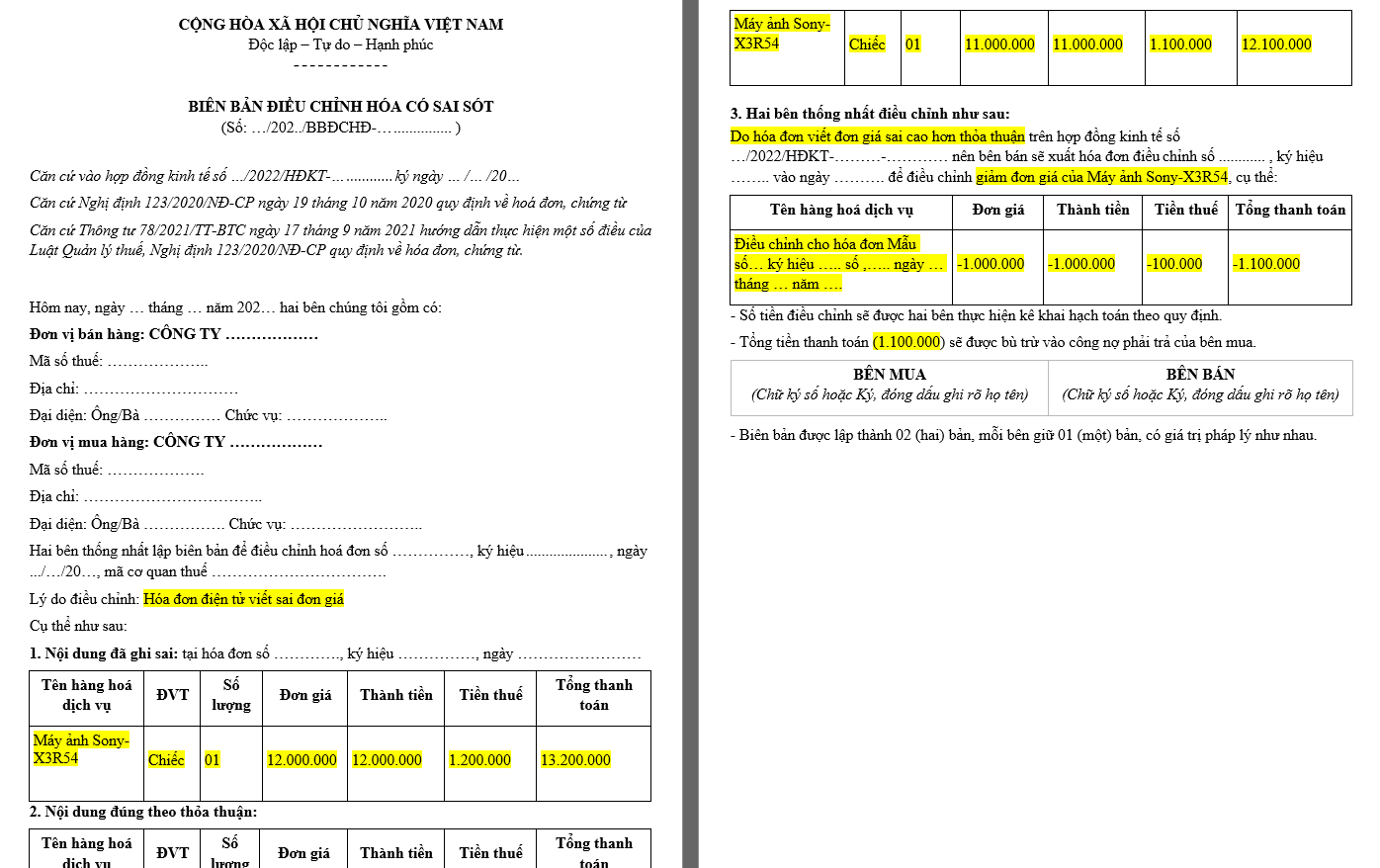

2. Adjustment Record Template for Incorrect Unit Price

Errors in unit price are one of the most common mistakes when issuing invoices. The template below helps businesses handle cases where the unit price on the invoice does not match the actual transaction, affecting the total amount and the tax payable.

Download the free adjustment record template for incorrect unit price

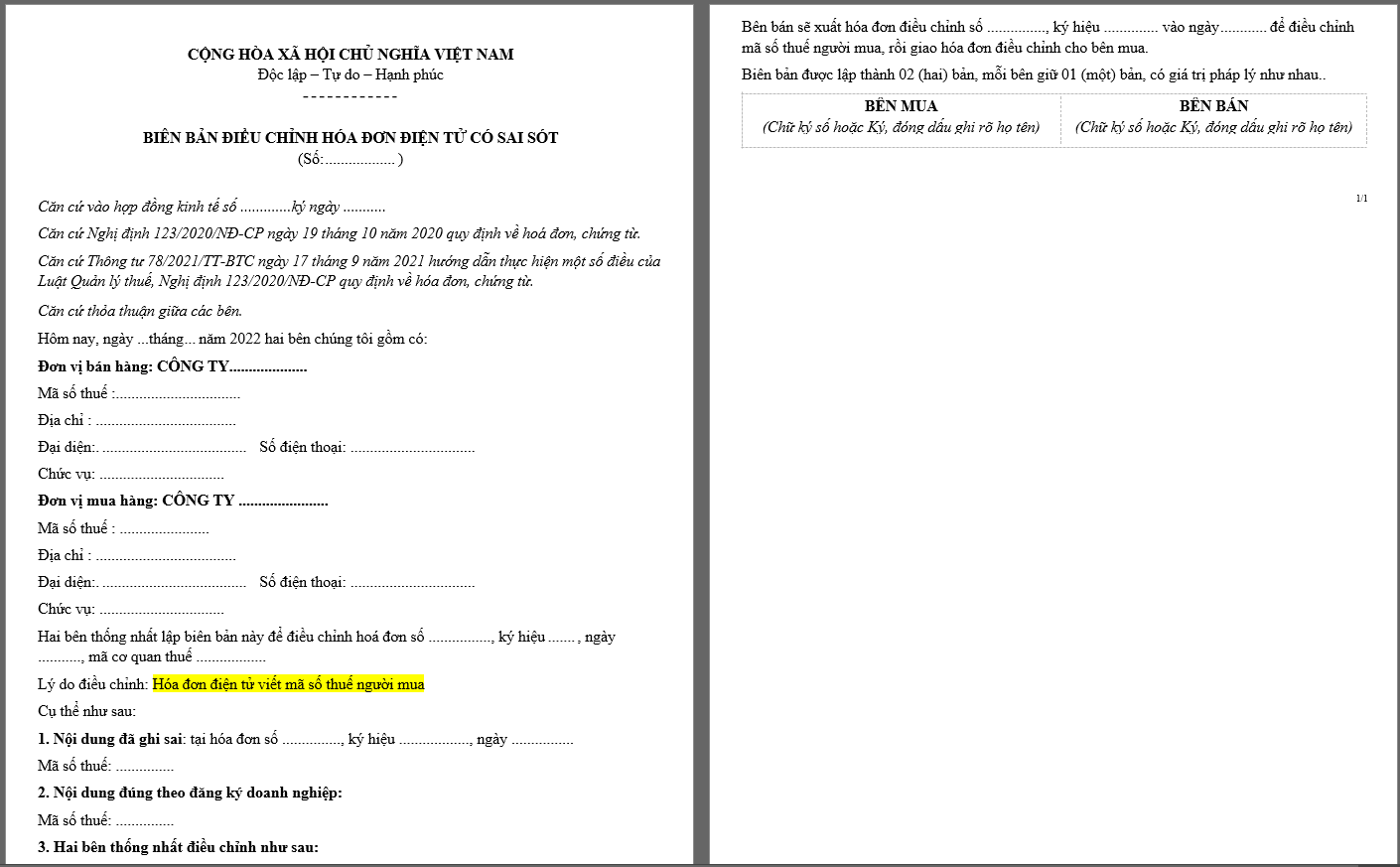

3. Adjustment Record Template for Incorrect Tax Code

The tax code is crucial information on an invoice, and errors in the tax code can make it difficult for the buyer to declare and deduct VAT. The following adjustment record applies to cases where the buyer’s tax code is recorded incorrectly.

Download the free adjustment record template for incorrect tax code

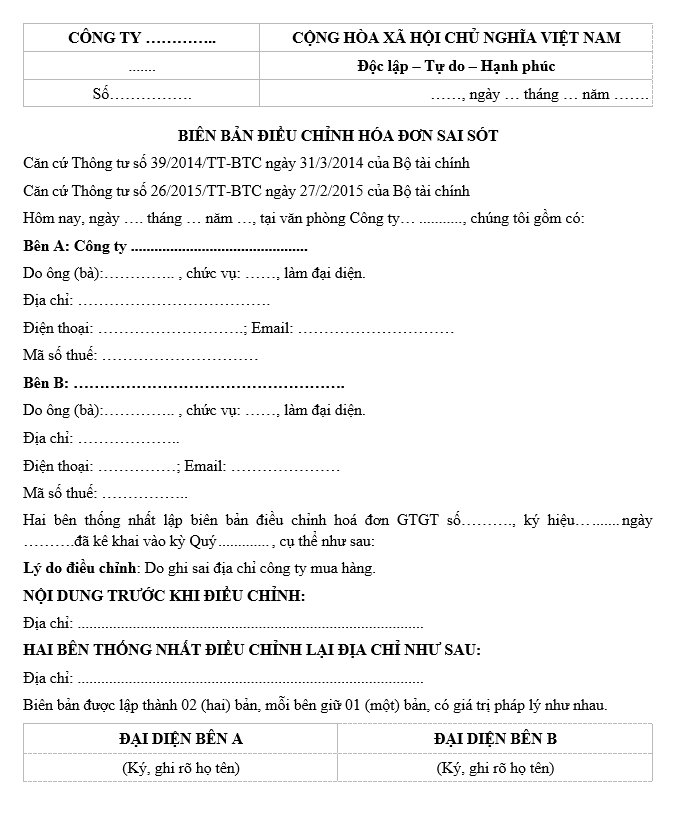

4. Adjustment Record Template for Incorrect Company Name or Address

The correct company name and address on the invoice are essential to ensure the document’s legal validity. If an error in this information is discovered, businesses can use the following adjustment record template to correct it without issuing a new invoice.

Download the free adjustment record template for incorrect name or address

5. Adjustment Record Template for Post-Invoice Discounts

In business operations, giving customers a discount after an invoice has been issued is a common scenario (e.g., volume discounts, promotional programs…). The template below applies to this situation and serves as the basis for issuing an adjusted invoice with a reduced value:

Download the adjustment record template for post-invoice discounts.doc

Notes on using the above template:

- Must have handwritten signatures + seals from both parties (or valid electronic signatures).

- The record must be created before the adjusted invoice is issued.

- The seller must issue the downward adjustment invoice within 7 days of the record’s creation date (delays may result in penalties).

- Clearly state the reason for the adjustment (promotion, trade discount, returned goods…).

- The buyer uses the record + the adjusted invoice to declare valid input tax.

Guide to Filling Out the Invoice Adjustment Record

To ensure the invoice adjustment record is created accurately and meets the requirements of Circular 78, you should note the following points when filling it out:

1. General Information Section

- Date of record: Enter the full day, month, and year the record was created in day/month/year format.

- Seller and buyer information: Fill in the full and correct business name, tax code, address, representative, and title. For information that needs correction (e.g., incorrect name or address), clearly state the correct information in this section.

2. Original Invoice Information Section

- Invoice number: Enter the correct number of the invoice to be adjusted.

- Series: Enter the correct series of the original invoice.

- Date of issue: Enter the correct day, month, and year the original invoice was issued.

3. Adjustment Content Section

- Specify the incorrect information on the original invoice: Detail the information that was incorrectly recorded on the original invoice.

- Correct adjusted information: Clearly state the correct information for the adjustment.

- Accurately calculate related amounts (if any):

- Pre-tax amount

- VAT amount

- Total payment amount

- Any differences (if adjusting the value)

4. Reason for adjustment

- Clearly state the reason for the invoice adjustment, for example:

- Due to data entry error

- Due to returned goods

- Due to a discount agreement after the invoice was issued

- Due to an adjustment in the quantity of goods/services

5. Method of resolution

- In case of information adjustment: Clearly state “Both parties agree to use this adjustment record along with the original invoice as a basis for accounting and tax declaration, without issuing an adjusted e-invoice.”

- In case of value adjustment: Clearly state “The seller will issue an adjusted invoice for the difference incurred” and detail the adjusted amount.

6. Confirmation signature section

- Ensure full signatures from representatives of both the seller and the buyer.

- Include the company seal (if an organization).

- Clearly state the full name of the signatory.

Creating an e-invoice adjustment record according to Circular 78 is an important process that helps businesses handle invoice errors legally. By adhering to the correct procedures and using standard record templates, businesses not only ensure accuracy in their accounting but also avoid legal risks that may arise during tax inspections and audits.