What is ROA? ROA Formula and Detailed Analysis Example

ROA (Return on Assets) is an important financial metric that helps evaluate a company’s efficiency in using its assets. Through ROA, managers and investors can clearly understand the profitability from existing resources. In this article, 1Office will help you understand what ROA is, its calculation formula, and how to analyze it with easy-to-understand practical examples.

Mục lục

- What is the ROA metric?

- The Significance of the ROA Metric

- How is the ROA metric calculated?

- How to analyze the ROA metric on financial statements

- How is ROA applied in business analysis?

- Points to note when calculating ROA in practice

- ROA ratio by industry

- ROA and Related Financial Ratios

- 5 Ways to Improve ROA in a Business (Detailed & Practical)

- Frequently Asked Questions

- Conclusion

What is the ROA metric?

ROA, short for Return On Assets, is the rate of return on assets. This is a comprehensive financial metric that reflects a company’s ability to generate profit relative to its total assets. This ratio shows how efficiently a company operates by comparing its after-tax profit with the capital invested in assets. The higher the ROA, the more effectively and productively the company is managing and utilizing its economic resources.

Learn more:

The Significance of the ROA Metric

The ROA (Return on Assets) metric is significant in evaluating a company’s operational efficiency, especially how it uses assets to generate profit. Specifically, ROA indicates:

- Asset utilization efficiency: ROA measures the level of profit a company can generate from each dollar of assets it owns. The higher this metric, the more efficiently the company is using its assets to generate profit.

- Company comparison: ROA is a useful tool for comparing the performance of companies within the same industry. A company with a higher ROA is generally considered to be operating more efficiently than its industry peers.

- Asset management: ROA helps managers and investors assess a company’s ability to manage its assets. A stable and high ROA often indicates that the company has a reasonable and effective asset utilization strategy.

- Investment decisions: For investors, ROA is a crucial metric to consider when deciding to invest in a company. A high ROA is often a sign of a company with good profit potential, while also reducing investment risk.

How is the ROA metric calculated?

To calculate ROA, we take net profit (Net Profit) and divide it by total assets (Total Assets), then multiply by 100 to convert it into a percentage. The ROA metric indicates what percentage of profit a company generates from the total assets it owns.

Where:

- Net profit is the remaining profit after all costs and taxes have been deducted.

- Average total assets is calculated by adding the total assets at the end of the current period to the total assets at the end of the previous period, then dividing by 2.

How to analyze the ROA metric on financial statements

Return on Assets (ROA) should be a positive number, and the higher the value, the better. Comparing the ROA of companies in the same industry or with the industry average helps evaluate a company’s profitability.

- If a company’s ROA is high, it indicates that the company can generate greater profits relative to its initial capital investment, meaning it uses its assets effectively. However, a high ROA can also attract new competitors to enter the market more easily, as it does not require a large capital investment in assets.

- Conversely, a low ROA indicates that the company is not using its assets efficiently to generate profits or is not fully competitive when compared to other companies in the same industry.

For example, if Company A’s ROA in 2024 is 12%, it means the company earns 120 million VND in profit for every 1 billion VND in assets during the year. The higher the ROA, the more effectively the company is shown to be using its assets.

How is ROA applied in business analysis?

What constitutes a good enough ROA for a business depends on the following factors:

What industry is the company operating in?

Each business sector has its own unique asset structure. For example, capital-intensive industries like manufacturing and infrastructure often have lower ROA because they require significant investment in fixed assets. Conversely, service industries may achieve higher ROA due to lower capital requirements.

Therefore, you cannot say that “an ROA higher than X% is good, and lower is bad”—there is no fixed number to judge good or bad. It is important to consider the company’s business model and the sector in which it operates when evaluating ROA.

Compare with the industry average

An effective way to use ROA in stock analysis is to compare a company’s ROA with the industry average. This helps you determine whether the company is performing better or worse than its competitors in the same industry, especially in terms of its ability to use assets to generate profits.

A company with a ratio higher than the industry average is often considered more efficient at generating profits from its assets, while a company with a lower ratio may be judged as less efficient.

Trend analysis

Another evaluation method is to analyze the company’s trend over time. If a company’s ROA has been consistently increasing for several years, it could be a sign that the business is using its assets more effectively than before. Conversely, if it gradually decreases over time, this may indicate that the company is struggling to generate profits from its assets.

Consider future growth prospects

Although a higher ROA is generally considered better because it indicates that the company is using its assets effectively to generate profits, when evaluating a stock, you also need to consider the company’s future growth prospects.

A company with a high ROA over the past few years may find it difficult to maintain that level if it operates in a mature industry with few opportunities for expansion or innovation. Conversely, a company with a currently low ratio but operating in a growing industry with high demand and many expansion opportunities may have greater growth potential in the future.

Points to note when calculating ROA in practice

ROA is a crucial indicator that helps businesses evaluate the efficiency of using assets to generate profits. However, in practice, calculating ROA is not as simple as using the formula “net income / total assets.” There are many factors to consider, such as the timing of data recording, asset fluctuations during the period, and how to exclude unusual items to accurately reflect business performance. Understanding these points will help managers and investors get a more accurate view of a company’s operational efficiency.

Calculation period for return on assets

Depending on the reporting period—monthly, quarterly, or annually—analysts can calculate ROA for each period as required. When comparing ROA across different periods, it is important to ensure the comparison is consistent and accurate.

Net return on assets

Many studies have shown that there is no specific number for return on assets (ROA) that is considered “good,” as this ratio depends on the size and industry of the business. A single year’s ROA is not enough to prove a company’s future operational efficiency; therefore, investors often track this ratio over a longer period—3-5 years for a medium-term assessment, and potentially up to a decade to observe changes and the impact of long-term business factors.

Additionally, this ratio is also evaluated based on the company’s stability. If it increases gradually over the years, it indicates that the business is operating stably and has good after-tax profits. Conversely, if it fluctuates erratically or decreases over time, the business may be judged as unstable or having declining operational efficiency.

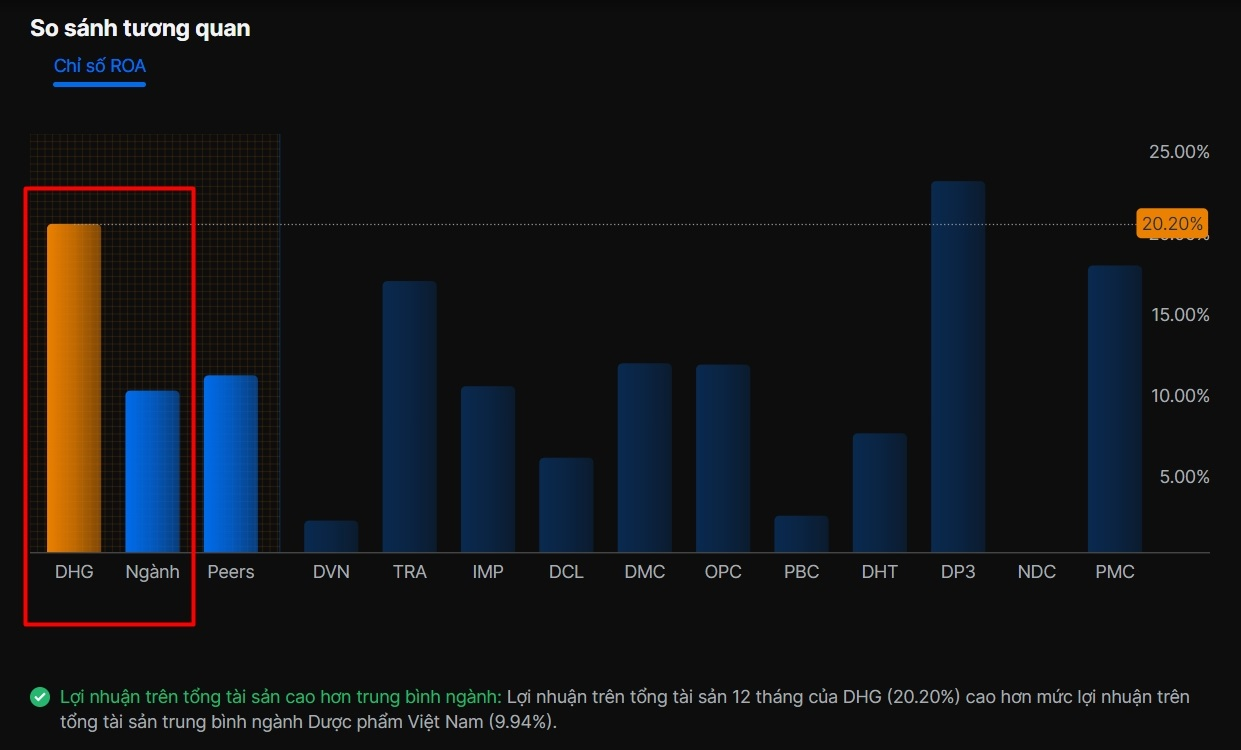

ROA ratio by industry

One of the common mistakes when evaluating ROA is directly comparing this ratio between businesses in different industries. In reality, each industry has a different asset structure, initial capital investment, and business cycle, leading to significantly different average ROA levels.

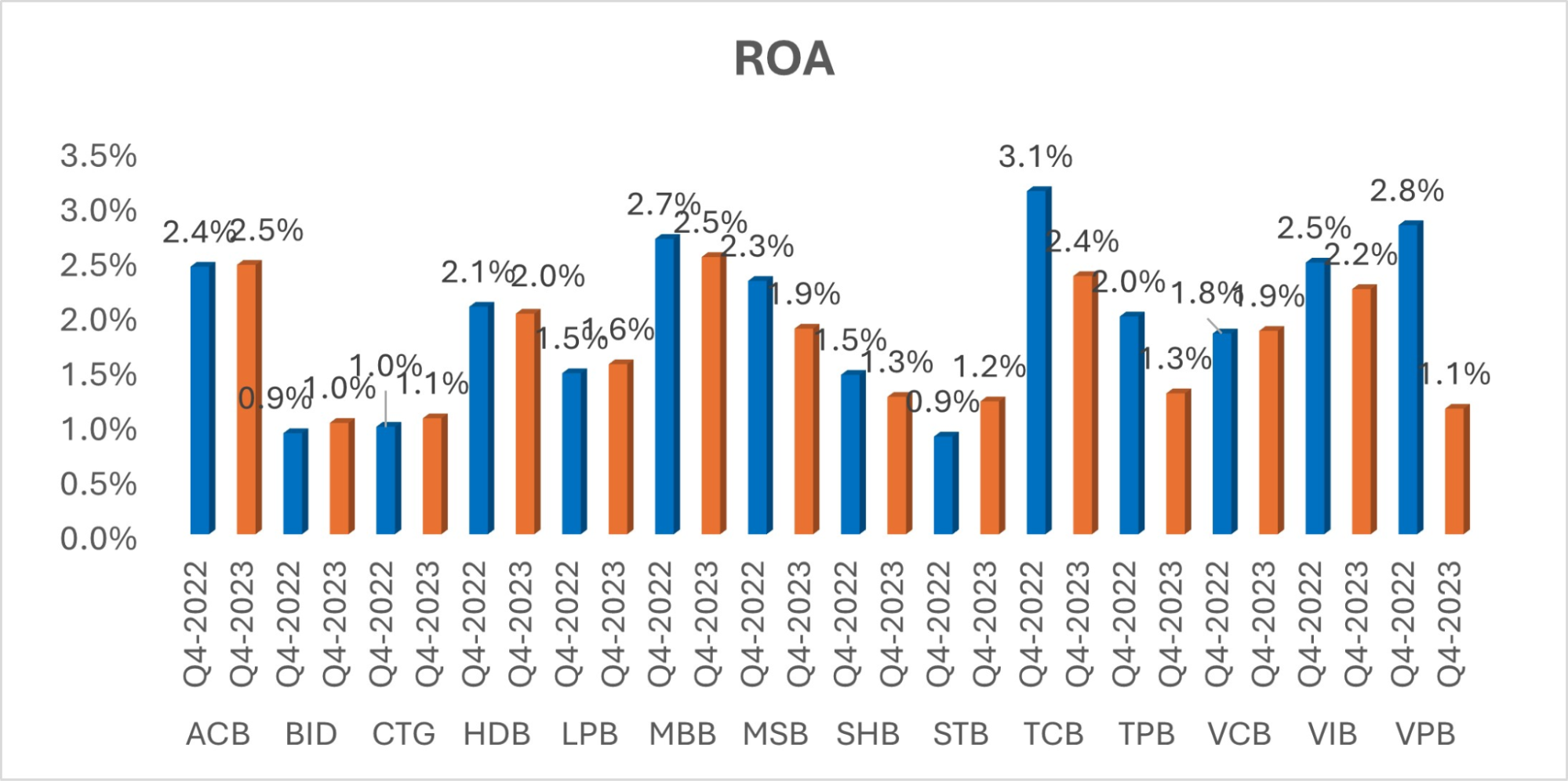

For example, the software technology industry often has a very high ROA (10–15%) due to its “asset-light” business model: most of the value comes from intellectual capital, brand, and software, not from factories or machinery. Meanwhile, banks have an ROA of only around 0.8–1% but are still considered efficient, because the assets on their balance sheets are mainly loans and securities—very large numbers that “drag down” the denominator of the ROA.

Below are the average ROA figures for some industries (based on global statistics and references from the Vietnamese market):

-

Information technology: ~12%

-

Personal & maintenance services (spa, fitness, private healthcare services): ~9.5%

-

Apparel retail industry: ~2.7%

-

Regional banks: ~0.9%

As you can see, a technology company with a 10% ROA is only considered “fair,” while a bank with a 1% ROA is considered “good” compared to the industry standard.

To make the comparison more intuitive and accurate, businesses or investors should:

- Use bar charts or benchmark tables: set the average industry ROA as the “benchmark,” then compare it with the target company.

- Analyze by detailed industry groups: instead of just saying “retail industry,” it should be broken down into food retail, apparel retail, electronics retail, etc., due to different asset characteristics.

- Track changes over time: not only compare with the industry but also compare the company’s ROA over 3–5 years to see improvement or decline trends.

For example:

-

Vinamilk (food – FMCG) typically has an ROA of around 17–20%, much higher than the standard for the manufacturing and processing industry, indicating a superior ability to utilize assets.

-

The Gioi Di Dong (MWG) in the mobile phone and electronics retail sector has an ROA of about 6–7%, higher than the benchmark for apparel retail (2.7%) but lower than FMCG, reflecting a model that requires significant working capital and inventory.

-

Vietcombank has an ROA of ~1%, on par with the banking industry standard, demonstrating efficiency similar to the general market level.

In summary, ROA is only truly meaningful when placed in the context of its industry. Instead of looking at the absolute number, businesses and investors should ask: “Is our ROA high or low compared to the industry standard?” – only then can they accurately assess the efficiency of asset utilization.

Why does ROA differ between industries?

The difference in ROA stems from asset structure and business models:

-

Asset-intensive industries (like manufacturing, transportation, utilities): require large investments in machinery and factories, leading to a low ROA.

-

Service/technology industries: have few tangible assets, relying mainly on intellectual capital and brand → ROA is usually high.

-

Finance/banking industries: have high leverage ratios and large assets (loans, securities) → ROA is low, but ROE is high.

Therefore, businesses should compare ROA within the same industry instead of against other sectors to avoid incorrect conclusions.

ROA is an important financial ratio with a clear meaning. However, managers and investors often evaluate it in a specific context and alongside many other financial ratios.

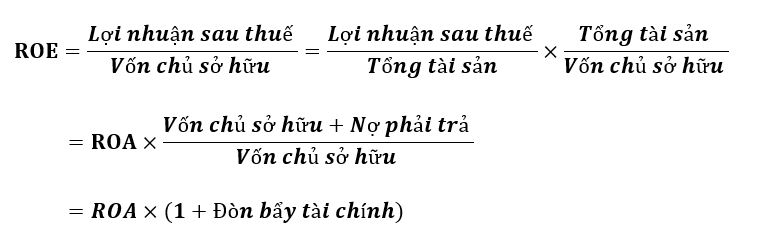

A ratio often considered alongside ROA is Return on Equity (ROE). The relationship between ROA and ROE is often analyzed through the financial leverage ratio.

When evaluating operational efficiency, ROA should be analyzed in parallel with other ratios.

-

ROE (Return on Equity): If a company has a high ROE but a low ROA, it indicates they are using significant financial leverage, meaning they rely heavily on debt to generate profits. This can be both an opportunity (leveraging debt for rapid growth) and a risk if the market fluctuates.

-

ROCE (Return on Capital Employed): This ratio is calculated on both debt and equity, making it suitable for analyzing companies that use a lot of debt, such as real estate, banking, or energy. ROCE helps provide a more comprehensive assessment of capital management efficiency than looking at ROA alone.

-

BEP (Basic Earning Power): Calculated as EBIT/Total Assets, BEP measures the ability to generate profit from assets before being affected by taxes and interest expenses. This is a “clean” ratio for comparing the core operational efficiency of companies in different financial environments.

Combining ROA, ROE, ROCE, and BEP will help investors and managers get a more comprehensive view: ROA shows asset utilization efficiency, ROE reflects shareholder benefits, ROCE balances debt and equity, and BEP isolates the true earning power of business operations.

>>> See more: What is the ROE ratio? Role, formula, and limitations of ROE

This formula helps business managers and investors accurately assess the ability to use resources effectively in the company’s business operations.

5 Ways to Improve ROA in a Business (Detailed & Practical)

In the corporate financial landscape, ROA (Return on Assets) is one of the key indicators that best reflects the efficiency of using assets to generate profit. However, many businesses experience low ROA despite growing revenue. The cause often lies in underutilized assets, high operating costs, or capital being “tied up” in non-core investments.

To improve ROA, businesses not only need to optimize costs or increase revenue, but more importantly, they need to know how to make every dollar of assets generate more value. Below are 5 detailed solutions, from effective asset management and improving net profit to restructuring capital and applying financial analysis, to help businesses sustainably increase their ROA.

5 ways to improve the ROA ratio

5 ways to improve the ROA ratio

1. Increase the efficiency of existing assets

One of the common “traps” leading to low ROA is when a business owns too many assets but doesn’t utilize them to their full capacity. For example: a factory operating at 50% capacity, vacant rental office space, or large but hard-to-sell inventory.

-

Detailed steps:

-

Conduct regular asset audits: Create a list of all assets → classify them into direct cash-flow generating assets, supporting assets, and assets with no remaining value.

-

Liquidate/lease out: If the business has empty warehouses or idle machinery → list them for rent (e.g., renting out factory space through industrial real estate platforms).

-

Repurpose assets: Some businesses move from large offices to co-working spaces, which both saves costs and reduces fixed assets.

For example: FPT once sold its old headquarters and switched to renting office space to focus capital on its software division – its ROA improved significantly thanks to asset optimization.

-

2. Increase net profit by optimizing costs

ROA = Net Profit / Total Assets → if you can’t increase revenue, increase profit by optimizing costs.

-

Detailed steps:

-

Review OPEX (operating expenses): cut unnecessary administrative costs (e.g., extravagant seminars, excess office space).

-

Automation: Implement ERP, CRM, and HRM systems to reduce personnel and paperwork costs.

-

Negotiate with the supply chain: Many retail businesses increase ROA by asking suppliers to share marketing costs or negotiating for better purchase discounts.

-

Taxes & Finance: Take advantage of tax incentives (for high-tech parks, innovative enterprises) to reduce fixed costs.

For example: The Gioi Di Dong (MWG) once reduced a series of store expenses (electricity, rent) by renegotiating with landlords → net profit increased, and ROA improved.

-

3. Accelerate asset turnover

If asset turnover is slow (long inventory holding periods, prolonged receivables), ROA will be low even if profits are decent.

-

Detailed steps:

-

Manage inventory using JIT (Just-in-Time): only order goods when there is demand. This helps reduce inventory and save working capital.

-

Apply demand forecasting: use AI/Big Data to predict sales trends → avoid overstocking.

-

Manage receivables: create a discount policy for early customer payments while tightening credit limits.

-

Increase machinery turnover: invest in a predictive maintenance system to prevent machine downtime → generate more output.

For example: Vinamilk optimizes its raw milk inventory turnover by forecasting market demand based on seasons → working capital is reduced, and ROA increases.

-

4. Restructure the investment portfolio & capital strategy

A business might take on too many non-core projects, causing total assets to swell while profits fail to keep up. This lowers the ROA.

-

Detailed instructions:

-

Divest from non-core projects: sell off inefficient investment segments (real estate, financial investments).

-

Reallocate loan capital: instead of borrowing to purchase inefficient fixed assets, invest in technology or high-profit segments.

-

Focus on core industries: direct capital to segments that generate sustainable profits (e.g., FPT focuses on software instead of real estate).

-

Compare the Internal Rate of Return (IRR) of each project to prioritize investments.

Example: Masan Group divested from its beer segment to focus on retail & food, thereby improving its ROA and ROE ratios.

-

5. Apply Dupont analysis to find the root cause

Many businesses see a low ROA but don’t know why. This is when you need to “dissect” it using Dupont Analysis:

-

Formula:

ROA = (Net Profit / Revenue) × (Revenue / Total Assets). -

If the profit margin is low → focus on reducing costs and increasing product value to raise the selling price.

-

If asset turnover is low → focus on reducing inventory, collecting debts, or selling off assets.

-

Analyze by industry: for example, a low ROA is normal in the banking industry (1%), but an ROA below 5% in the technology industry is a warning sign.

Example: A retail company has a low ROA due to slow asset turnover → the solution is not to cut costs, but to manage inventory and receivables better.

Frequently Asked Questions

Why does ROA decrease even when revenue increases?

Because an increase in revenue does not necessarily come with a corresponding increase in profit. If assets grow faster, costs are higher, or asset utilization is not efficient, ROA can still decrease.

What does ROA reflect about business efficiency?

ROA reflects a company’s ability to use its assets to generate profit. The higher this ratio, the more efficiently the company is typically utilizing its assets.

What factors affect ROA the most?

ROA is primarily affected by net profit and average total assets. When either of these two factors fluctuates significantly, ROA also changes accordingly.

Does ROA help evaluate the efficiency of asset utilization?

Yes. It is one of the most common ratios used to see how efficiently a company is using its assets to generate profit.

When should a business use software to track ROA?

A business should use software when it needs to track profit, assets, and other financial ratios simultaneously, quickly, and accurately. If you want to manage financial data centrally and support managers in making more effective decisions, you can refer to 1Office’s revenue and expenditure management software.

Conclusion

By analyzing ROA along with other financial metrics, you can gain a deeper insight into the company’s financial situation and make smarter investment decisions. We hope the information in this article helps business owners better understand the ROA ratio and apply ROA analysis effectively in assessing their company’s financial health.