Guide to Accounting for Sales Returns According to Circular 200 & 133: How-to and Examples

Sales returns are a common transaction when customers return goods due to incorrect specifications, quality defects, wrong delivery, or not as agreed. If not accounted for correctly, a business may incorrectly record revenue, liabilities, inventory, and related VAT. The article below will guide you on how to account for sales returns, the accounts to use, and provide journal entry examples for accountants to easily apply in practice.

Mục lục

1. What are sales returns?

For the seller

Sales returns refer to the quantity of products that a business has distributed or sold to the market, but are later returned by customers for reasons such as:

- The product does not meet quality standards.

- The product has incorrect specifications, type, or does not match the characteristics ordered by the customer.

- The customer did not receive the goods due to other objective reasons.

In addition to trade discounts and sales allowances, sales returns are considered one of the deductions from sales revenue. The value of sales returns affects the actual sales revenue for the business period, and consequently impacts the company’s net revenue.

For the buyer

Returning goods to the seller does not create any revenue deductions or losses for the buyer. However, this process requires a time investment from the business. Additionally, the accounting department needs to make appropriate journal entries to accurately record the purchase return process in the accounting system.

- If the buyer is a business that has an invoice, returning the goods requires issuing a return invoice with a price equivalent to the price on the original purchase invoice.

- If the buyer is an individual without an invoice, the return process requires creating a signed record with the seller to document the quantity and value of the returned goods.

2. How to account for sales returns

The process of accounting for return invoices is not just about making separate journal entries for the buyer and seller; it also depends on the differences in the company’s accounting regulations, based on the application of relevant circulars such as Circular 200/2014/TT-BTC and Circular 133/2016/TT-BTC.

2.1 Accounting for sales returns according to Circular 200

Circular 200/2014/TT-BTC regulates the use of account 5212 – “Sales Returns” to reflect the revenue of goods returned by customers during the accounting period. Account 5212 has the following structure:

- Debit side: Used to record the revenue from returned goods, for which a refund has been completed for the customer or deducted from the previously recorded accounts receivable for the returned goods.

- Credit side: Used to transfer the revenue from sales returns to account 511 – “Revenue from Sales and Service Provision” to determine net revenue at the end of the period.

The accounting method for sales returns according to Circular 200 is as follows:

Seller

When the business makes a sale, the accountant makes journal entries to record the sales revenue and the cost of goods sold as follows

* Recording revenue:

- Debit accounts 1111, 1121, 131

- Credit account 5111

- Credit account 33311 (if any)

* Recording cost of goods sold:

- Debit account 632

- <span style="font-weight* Record the decrease in cost of goods sold:

- Debit account 156

- Credit account 632

Next, the accountant performs year-end closing entries, including the entry to close the revenue deduction amount recorded for sales returns during the period as follows:

- Debit account 511

- Credit account 5212

Additionally, the accountant also needs to identify and record any costs incurred related to the returned goods (if any) through the following accounting entries:

- Debit account 641

- Credit accounts 111, 112,…

Buyer’s side

When the business purchases goods, the accountant makes an entry to record the receipt of goods into the warehouse as follows:

* Record the increase in the value of purchased goods:

- Debit accounts 156, 152, 153, 211

- If any, debit account 1331

- Credit accounts 1111, 1121, 331

When returning purchased goods to the seller, the accountant records the decrease in the value of the purchased goods as follows:

* Record the decrease in the value of purchased goods:

- Debit accounts 1111, 1121, 331

- Credit accounts 156, 152, 153, 211

- Credit account 1331

Example of accounting for sales returns according to Circular 200

Company XYZ sells a shipment of goods worth 600,000,000 VND, including 10% VAT, with a cost of goods sold of 540,000,000 VND. However, they have not yet received payment from the customer. Later, the customer decides to return 50% of the contract value.

Company XYZ applies the accounting system according to Circular 200. Based on the guidelines, the accountant of Company XYZ performs the following entries:

* Reflect the selling price:

- Debit account 131: 660,000,000 VND

- Credit account 511: 600,000,000 VND

- Credit account 3331: 60,000,000 VND

* Reflect the cost of goods sold:

- Debit account 632: 540,000,000 VND

- Credit account 156: 540,000,000 VND

When the customer returns a portion of the goods, the accountant records:

* Record a 1/2 reduction in revenue:

- Debit account 5212: 330,000,000 VND

- If any, debit account 3331: 33,000,000 VND

- Credit account 131: 363,000,000 VND

* Record the decrease in cost of goods sold and simultaneously receive the goods back into inventory:

- Debit account 156: 270,000,000 VND

- Credit account 632: 270,000,000 VND

* At the end of the period, the accountant performs a closing entry to record the revenue deduction:

- Debit account 511: 330,000,000 VND

- Credit account 5212: 330,000,000 VND

2.2 Accounting for sales returns according to Circular 133

Accounting for sales returns according to Circular 133 Circular 133/2016/TT-BTC does not use account 5212. Therefore, sales returns are no longer reflected in a separate account. Instead, they are recorded directly in account 511 – “Revenue from sales and service provision” by reducing revenue (a debit entry).

Seller’s side

When a customer returns goods, the accountant records a decrease in revenue and cost of goods sold as follows:

* Record the decrease in revenue:

- Debit account 511

- If any, debit account 3331

- Credit accounts 131, 111, 112

* Record the decrease in the cost of goods sold:

- Debit Account 156

- Credit Account 632

Buyer

Since the buyer only records an increase in the value of purchased goods upon purchase and a decrease upon return, the accounting entry will be similar to the instructions in the “Buyer” section for businesses applying the accounting regime under Circular 200/2014/TT-BTC.

3. Guide to Handling Sales Returns

In the event of a sales return, both the seller and the buyer need to make accounting entries to ensure the accuracy of accounting information. Therefore, the buyer returning the goods must issue an invoice to provide a basis for the accounting entries.

If the customer returning the goods is able to issue an invoice, the process is as follows:

* Issue a return invoice to the selling company:

- The unit price on the return invoice must be equivalent to the unit price on the original purchase invoice.

- The invoice must clearly state the reason for the return.

* Then, the accountant adjusts the VAT for the returned goods invoice:

- Seller: adjusts sales revenue and output VAT.

- Buyer: adjusts purchase value and input VAT.

In cases where the customer returning the goods cannot issue an invoice, the process follows the guidance in Appendix 4 of Circular 39/2014/TT-BTC (Guiding the implementation of Decree 51/2010/ND-CP and Decree 04/2014/ND-CP of the Government on invoices for the sale of goods and provision of services).

4. Special Situations & Important Notes for Accounting

When accounting for sales returns, businesses may encounter special situations that require careful handling to avoid errors and ensure compliance with accounting regulations. Below are some common cases with specific guidance:

4.1. Sales Returns with Associated Costs

When goods are returned, the selling business often incurs additional related costs such as transportation costs, loading/unloading, quality inspection, or repairs (if the goods are defective due to a manufacturing fault). These costs are not recorded as part of the cost of goods sold but must be accounted for separately as selling expenses or general and administrative expenses.

Accounting principle:

- These costs do not change the revenue or cost of goods sold for the returned items.

- The accountant records them as selling expenses or general and administrative expenses, depending on their nature.

Reference entry:

- Debit Account 641 / 642

- Credit Account 111, 112, 331, etc.

Example: If the return shipping cost is 5,000,000 VND, the entry would be: Debit Account 641: 5,000,000 VND / Credit Account 111: 5,000,000 VND. This helps to accurately reflect the actual costs incurred and avoid distorting the gross profit.

4.2. Sales Returns Occurring in a Subsequent Accounting Period

If goods are returned after the accounting period has ended (e.g., sold in Q4 but returned in Q1 of the following year), the business needs to make a retrospective adjustment according to the consistency principle in accounting. According to Circular 200 and 133, it should not be recorded in the current period but must be adjusted in the original period of occurrence if it has a material effect.

Handling: Review the financial statements of the previous period and make an adjusting entry (if necessary), while also making a note in the notes to the financial statements.

Example: Reduce the previous period’s revenue via Account 511 and adjust the cost of goods sold via Account 632. Businesses should consult with an auditor to avoid violating the going concern principle.

In the case of returned promotional items or goods sold with a special offer, the business reduces the corresponding revenue (Account 521) and records the return of cost of goods sold if accounting conditions are met; any promotional costs already incurred are not adjusted and continue to be tracked in Account 641/642.

If the promotional item is determined to have an independent value, it is handled similarly to regular sales; for trade discounts, the accountant adjusts the net revenue directly. All return transactions must have complete records and adjusted VAT invoices to ensure tax compliance.

Special situations and important notes for accounting 5. Detailed Guide on Journal Entries and Handling Sales Returns in Accounting

In business operations, sales returns are a common situation where customers return products due to defects, not meeting requirements, or other reasons. The accounting process for sales returns must comply with regulations to ensure accurate bookkeeping, correctly affecting revenue, costs, and taxes. We will provide a comprehensive guide on the process for handling sales returns, how to record sales returns, and examples of accounting entries for sales returns.

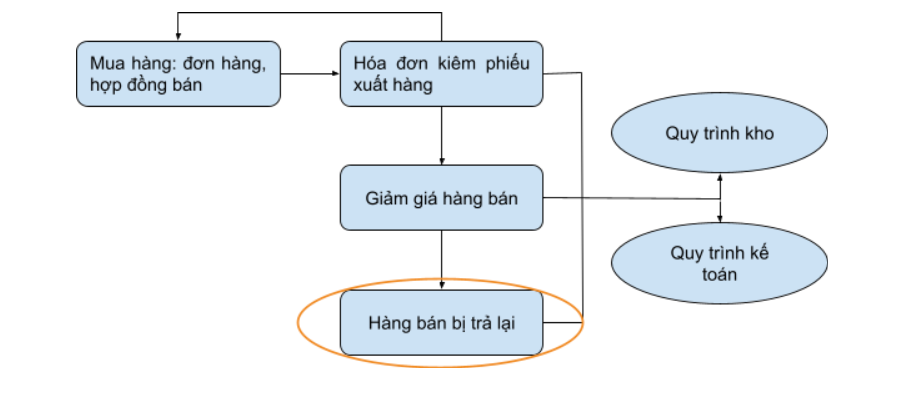

1. Process for Handling Sales Returns

The process typically includes the following steps:

- The customer notifies and sends back the returned goods with a reason.

- The business inspects the goods (handling defective returned goods or intact goods).

- Create a goods receipt note for sales returns to receive the goods into inventory.

- Issue an adjustment invoice for sales returns (credit note) as stipulated in Circular 39/2014/TT-BTC and Circular 26/2015/TT-BTC.

- Reduce revenue for sales returns and adjust VAT.

When should sales returns be recorded? They are usually recorded as soon as all supporting documents are available: goods return record, goods receipt note, and adjustment invoice (or an adjustment record if a new invoice is not issued).

2. How to Record and Account for Sales Returns

- Revenue Reduction: Use account 521 – Sales Returns to record the revenue reduction.

- VAT on Sales Returns: Simultaneously, adjust the output VAT downwards.

- Accounting for sales returns with tax includes the cost of goods sold (if the goods are returned to inventory).

Accounting for sales returns in a business typically involves two scenarios:

- Intact goods: Return to inventory and reduce revenue.

- Defective goods: Can be recorded as an expense or handled separately.

3. Example of Accounting for Sales Returns

Suppose on December 15, 2025, company A sells 100 products to customer B for a pre-tax price of 10 million VND, with 10% VAT (1 million VND), for a total of 11 million VND. On December 20, 2025, the customer returns 20 products due to a technical defect (pre-tax price of 2 million VND, VAT of 200,000 VND).

Journal entry when the customer returns goods:

Debit Acct 521 – Sales Returns: 2,000,000 Debit Acct 3331 – VAT Payable: 200,000 Credit Acct 131 – Accounts Receivable: 2,200,000 (To adjust for the reduction in revenue and VAT as per the adjustment invoice for sales returns)

Simultaneously, record the return of goods to inventory (cost of goods sold 1,200,000 VND):

Debit Acct 156 – Merchandise Inventory: 1,200,000 Credit Acct 632 – Cost of Goods Sold: 1,200,000 (To record the reduction in cost of goods sold)

If the defective goods are not returned to inventory but are scrapped or repaired, a separate expense is recorded.

4. Impact of Sales Returns on Profit and Accounting Records

- Impact of sales returns on profit: Reduces net revenue and cost of goods sold → gross profit decreases accordingly (if returned to inventory). If not handled correctly, it can cause a discrepancy in sales returns between the books and reality.

- Accounting records for sales returns: Account 521 is only used for deductions and is closed to Account 511 at the end of the period to determine net revenue.

- How to adjust revenue for sales returns: Always issue an adjustment invoice or an adjustment record, and file a supplementary tax declaration if necessary.

Important Notes

- VAT on sales returns: Must be adjusted downwards on the VAT declaration for the period in which it occurs.

- Handling defective returned goods: If the goods are severely damaged, they can be recorded as a loss or warranty expense.

- Adhere to the document matching principle: goods receipt note for sales returns + adjustment invoice + inspection record.

Correctly recording journal entries for sales returns will help the business accurately reflect its business results and avoid errors during tax finalization. If your business frequently encounters this situation, you should establish a clear internal process to ensure timeliness and accuracy in accounting.

6. Optimizing the Sales Return Process for Businesses

To mitigate accounting risks, reduce incurred costs, and ensure financial data accurately reflects the business’s operational status, businesses need to proactively standardize and optimize the entire sales return process, not just the accounting stage, specifically:

6.1. Establish a Clear and Transparent Return Policy

Businesses should issue a unified and public return policy from the outset, which clearly states:

- Conditions and time limits for permissible returns

- Responsibilities of each party when a return occurs

- Methods of handling refunds, offsetting <a href="https://1office.vn/congMost sales returns are due to quality defects, incorrect specifications, or unclear product information. Therefore, businesses need to:

- Strictly control the production, packaging, and shipping stages

- Synchronize product information between the sales and warehouse departments

- Review promotion policies and product descriptions to avoid misunderstandings

Reducing the return rate not only helps stabilize revenue but also reduces the pressure of adjusting accounting books.

6.3. Use accounting software to automate operations

Processing sales returns simultaneously involves sales, warehouse, receivables, taxes, and general accounting. Therefore, using accounting software or an integrated management system helps:

- Automatically record return transactions to the correct accounts

- Synchronize data between invoices, inventory, and customer receivables

- Minimize errors from manual data entry and missing documents

The 1Office business management platform supports end-to-end control from sales to accounting, helping businesses process sales returns quickly, accurately, and consistently.

6.4. Train and enhance staff capabilities

Besides the system, the human factor still plays a decisive role. Businesses need to regularly:

- Train the accounting department to master the regulations in Circular 200 and 133

- Guide the sales and warehouse departments to coordinate correctly according to the return process

- Update on changes regarding invoices, VAT, and related documents

A staff that clearly understands processes and responsibilities will help the business reduce the risk of errors, ensure legal compliance, and improve financial management efficiency.

The above is a detailed guide on how to account for sales returns according to Circular 200 and 133. We hope this article provides you with useful information and makes your accounting work more convenient.

To not miss out on knowledge, gifts, and templates that support businesses in management and operations, click Follow 1Office’s Zalo OA today!