How to Calculate Product Cost: Formula, Examples, and Application Methods

How to calculate product cost is a crucial basis that helps businesses determine selling prices, control costs, and evaluate production efficiency. If the product cost is calculated incorrectly, businesses may set inaccurate prices, reduce profit margins, or find it difficult to control incurred costs. This article will guide you on how to calculate product cost, provide illustrative examples, and discuss common application methods.

Mục lục

- 1. What is product cost?

- 2. Classifications of product cost

- 3. Why is it necessary to calculate product cost accurately?

- 4. Detailed steps for calculating product cost

- 5. Methods for calculating product cost

- 5.1 Calculating product cost using the simple (direct) method

- 5.2 Calculating product cost using the coefficient method

- 5.3 Calculating product cost using the proportional method

- 5.4. Job Order Costing Method

- 5.5. Costing by the By-Product Exclusion Method

- 5.6. Costing using the joint method

- 5.7 Example of Product Costing and Service Costing

- 6. What are the common difficulties in product costing?

- 6.1 Difficulty in gathering and classifying costs

- 6.2 Complexity in allocating manufacturing overhead

- 6.3 Inaccurate valuation of work in progress

- 6.4 Handling spoiled and low-quality products

- 6.5 Lack of synchronization between accounting and production departments

- 6.6 Impact of Cost of Goods Sold on Profit

- 7. Manage, track, and calculate product costs accurately with 1Office

- 8. Frequently Asked Questions

1. What is product cost?

Product cost is the total expense to produce one unit of a product, including raw material costs, labor costs, and general production costs. It reflects the actual value of the product before it is sold on the market and is a crucial factor for setting selling prices and evaluating profitability.

1.1 Factors that constitute product cost

In essence, product cost is formed from two main groups of factors: production cost and service costs (non-production costs).

Factor 1 – Production Cost

Production cost is the core expense incurred directly in the process of creating a product. It is the most important foundation that constitutes the product cost.

Production cost includes:

- Direct material costs: This is the total cost of main raw materials and auxiliary materials that directly make up the finished product. For example: input materials, semi-finished goods, and packaging attached to the product.

- Direct labor costs: This includes wages, allowances, and payroll deductions payable to employees directly involved in the product manufacturing process.

- General production costs: These are indirect costs that serve production activities, such as: salaries of workshop management staff, depreciation of machinery and equipment, factory rent, production utilities (electricity, water), tools and supplies, machinery repair costs, etc.

All these costs are aggregated to determine the production cost, reflecting the actual expense of creating the product during the period.

Factor 2 – Service Costs (Non-Production Costs)

After the product is completed, the business continues to incur costs to bring the product to market and reach consumers. This is the second group of costs that constitutes the product cost.

Service costs include:

- Sales and marketing personnel costs: This is the cost for the team of sales, marketing, and communications staff—those who directly introduce, consult, and bring the product to customers.

- Advertising and marketing costs: This includes advertising costs on channels such as social media, websites, newspapers, flyers, events, promotions, etc. Choosing the right promotional channels significantly impacts sales efficiency and product cost.

- Other related incurred costs: In some cases, the product cost also includes export taxes, import taxes, shipping costs, warehousing, storage, or other costs incurred during the product distribution process.

Production costs can be classified by:

- Cost behavior: Fixed (depreciation) and variable (raw materials).

- Relationship to the product: Direct and indirect.

Aggregating production costs is a crucial step in the cost calculation process, which involves gathering from accounts 621, 622, and 627 at the end of the period to transfer to Account 154 (Work in Progress).

| Read more: How to calculate product percentage discount – 3 factors businesses need to consider when determining discounts |

2. Classifications of product cost

2.1 Classification by calculation time

With this classification, product cost is divided into 3 types

- Planned cost: This is the cost calculated at the planning stage, so all expenses are planned expenses.

- Standard cost: This is the cost calculated for a specific period of the project.

- Actual cost: This is the actual cost after the product has been manufactured.

2.2 Classification by scope of incurred costs

With this classification, we have 2 types of product cost

- Production cost: Includes all costs that make up the product, such as raw materials, labor costs, and other incurred expenses.

- Cost of goods sold: A broader definition that, in addition to the direct costs of creating the product, also includes general costs such as corporate management expenses, advertising costs, and costs of bringing the product to consumers.

Calculating product cost correctly plays a very important role in the business and development of a company. Correctly calculated product cost provides a basis for determining the selling price of the product.

3. Why is it necessary to calculate product cost accurately?

Here are the reasons why accurate product cost calculation plays a key role in production management and business efficiency:

- Competitive product pricing: Cost is the core basis for a business to set a selling price that is appropriate for the market. Accurate cost calculation helps businesses avoid pricing too high, which loses competitive advantage, or pricing too low, which leads to losses.

- Cost control and profit optimization: By understanding the cost structure, businesses can easily identify unreasonable expenses, thereby taking measures to control and cut waste, and sustainably improve profit margins.

- Support for production and business decisions: The cost reflects the actual efficiency of each product and each stage. Based on this, businesses can decide whether to continue production, expand, or scale down, or even discontinue inefficient products.

- Basis for financial planning and forecasting: Accurate cost data helps in creating realistic budget plans, cost estimates, and profit forecasts, reducing the risk of discrepancies in financial management.

- Evaluating business performance: Comparing costs between periods, products, or departments allows businesses to assess the efficiency of their production organization, thereby adjusting their operational and management strategies more appropriately.

4. Detailed steps for calculating product cost

Below is the standard process for calculating product cost used in businesses:

Notes:

(1) Aggregate production costs include: Work-in-progress cost at the beginning of the period, production costs incurred during the period, work-in-progress cost at the end of the period)

(2) The output for allocation is calculated by the formula: Beginning Qty + Produced Qty = Completed Qty + Ending Qty

(3) Select a cost calculation method

(4) Create a product cost sheet

5. Methods for calculating product cost

5.1 Calculating product cost using the simple (direct) method

- Application conditions: The direct product costing method is often applied to businesses with simple production processes, few product types, and large production volumes. A characteristic of these businesses is a short production cycle.

- Applicable industries: Power plants, water treatment plants, compressed air facilities, coal mines, etc.

- The object for cost calculation is the final product.

- Formula for simple product cost calculation

- Practical application

Assumption: A manufacturing company has the following aggregated accounting cost items in August 2022: (unit: 1,000 VND)

Given that in August 2022, the company completed and warehoused 5,000 products, with 1,290 products as work-in-progress.

With the data above, we can calculate the cost of completed products in August 2022 using the simple method as follows:

")

*Number of completed products = 5,000

See more: The process of building a sales plan and common issues encountered

5.2 Calculating product cost using the coefficient method

- Applicable conditions: The coefficient method of cost calculation is applied in businesses that use the same amount of raw materials and labor to simultaneously produce multiple types of products. This method does not separate costs for each product type but aggregates them throughout the entire production process.

- Objects of cost calculation: each product type within the group.

- Formula

Step 1. Calculate the total production cost of all product types

Step 2.

-

- Convert the actual output of each product type into the standard product output based on the conversion coefficient of each type.

-

- Calculate the total number of standard products by summing up the standard product quantity of each type.

Step 3. Calculate the unit cost of the standard product using the formula

Step 4. Calculate the unit cost of each product type using the formula

Step 5. Calculate the total cost of each product type

- Practical application

Assumption: A manufacturing company uses the same type of raw material on the same production line to produce various types of finished goods. In August 2022, the company warehoused completed finished goods with the following quantities:

At the end of the accounting period, the aggregated costs and inventory data for work-in-progress products are shown in the table below:

To calculate the production cost using the coefficient method, we follow the steps in the formula as follows

- Select a standard product and establish conversion coefficients

Assume the company chooses Finished Product A as the standard product with a conversion coefficient of 1 and establishes conversion coefficients based on the selling price. Thus, we have:

-

- Conversion coefficient for Finished Product A = 1

- Conversion coefficient for Finished Product B = 250,000 / 200,000 = 1.25

- Conversion coefficient for Finished Product C = 300,000 / 200,000 VND = 1.5.

- Calculate the cost:

- Calculate the total production cost of all product types = 165,000 + 1,815,000 – 330,000 = 1,650,000 VND.

- Convert the actual output of each product type to the standard product output as follows

- Calculate the unit cost of the standard product – Finished Product A = 1,650,000 / 11,750 = 140.42553 VND

We have the following table for calculating the unit cost and total cost for each product type:

5.3 Calculating product cost using the proportional method

- Application conditions: Businesses that apply the proportional method to calculate product cost are typically those that produce products using the same type of raw material but with different specifications and qualities, where coefficients cannot be used to convert these product types.

- Applicable industries: Manufacturing businesses such as textiles and garments, footwear production, and production of water pipes with different specifications, etc.

- Objects for cost calculation: Each product specification within the group.

- Formula for calculating product cost using the proportional method:

Step 1. Select the criterion for cost allocation. This criterion can be the planned cost, standard cost, etc.

-

- Planned cost is calculated based on planned production costs and planned output. The planned cost is determined before the production or manufacturing of the product begins.

- Standard cost is determined based on the current cost norms at a specific time within the period for one unit of product. The standard cost is also determined before the production process.

Step 2. Calculate the total actual cost for the group of products completed during the period using the formula:

Step 3. Calculate the overall cost ratio for the product group based on the selected allocation criterion:

*The total allocation criterion is the total planned cost or total standard cost of the product group selected based on the criterion.

Step 4. Calculate the actual cost for each product specification

- Practical application

Assumption: A manufacturing company uses the same type of raw material to produce product type A in two different sizes, A1 and A2. The company chooses planned cost as the cost allocation criterion with the following information:

Given that in August 2022, the company completed and warehoused 2,000 units of product A1 and 1,500 units of product A2.

The accounting cost items gathered in August 2022 are as follows: (unit: 1,000 VND)

To calculate the production cost using the proportional method, we follow the steps according to the formula as follows

Step 1. Select the cost allocation criterion: planned cost

Step 2. Calculate the total actual cost for product type A completed during the period

The quantity of product A completed in the month is: 2,000 + 1,500 = 3,500 units

Step 3.

- First, calculate the total planned cost based on the actual output:

- Calculate the cost ratio for product group A:

Step 4. Calculate the actual cost for each product type A1 and A2

- Product A1

- Product A2

5.4. Job Order Costing Method

- Conditions for use: The job order costing method is used by businesses that manufacture products based on specific orders.

- Applicable fields: Businesses that produce single items or custom orders, such as manufacturing office desks and chairs for a company, producing furniture, etc.

- Objects of cost calculation: For single-item production processes: each individual order. For mass production processes (multiple orders): allocate overhead costs to each specific order.

- Formula

- Practical application

Assumption: A manufacturing company receives 2 orders, A and B, in August 2022. The cost items collected by the accounting department during the month are as follows

By the end of August 2022, 100 finished products for order A are put into inventory, while order B is not yet complete.

The business needs to calculate the cost for the completed order (A) and the value of work-in-progress for the incomplete order (B).

To calculate the cost, follow these steps:

- First, allocate overhead costs to each order:

- Overhead costs allocated to order A = (28,000,000 / 70,000,000) x 30,000,000 = 12,000,000

- Overhead costs allocated to order B = (28,000,000 / 70,000,000) x 40,000,000 = 16,000,000

- Total cost of order A = 30,000,000 + 10,000,000 + 12,000,000 = 52,000,000

- Unit cost of product for order A = 52,000,000 / 100 products = 520,000/product

- Value of work-in-progress for order B = 40,000,000 + 15,000,000 + 16,000,000 = 71,000,000

5.5. Costing by the By-Product Exclusion Method

- Conditions for use: The by-product exclusion method is applied in businesses where a single production process yields both main products and by-products.

- Applicable fields: Businesses processing instant noodles, beer, alcohol, sugar, etc.

- Object of cost calculation is the Main Product

- Formula

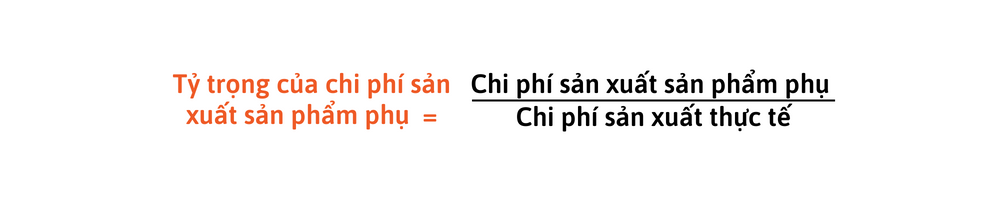

Step 1. Determine the cost of the by-product and the proportion of the by-product’s production cost relative to the main product:

Step 2. Calculate the cost of the main product:

- Practical application

Assumption: A sugar manufacturing company in August 2022 has the following cost items collected by the accounting department

By the end of August 2022, the manufacturing company puts 400 tons of sugar product into inventory, and also obtains 10 tons of molasses with a cost of 200/ton.

From the data above, we can calculate the cost as follows:

- Production cost of by-product = 10 x 200 = 2,000

- Actual production cost = 20,000 + (160,000 + 30,000 + 20,000) – 30,000 = 200,000

- Proportion of by-product production cost = (2,000 / 200,000) * 100% = 1%

- Cost of the main product:

5.6. Costing using the joint method

- Conditions for use: Businesses that use the joint method are often those with special technological processes and products, requiring a combination of different methods for costing.

- Applicable fields: Garment, footwear, chemical production, and knitting businesses.

- Formula

The joint method is a combination of the methods presented above, depending on the actual data and situations, for example, combining the coefficient method with the by-product value exclusion method.

5.7 Example of Product Costing and Service Costing

Example of product costing (wooden table production):

- Direct material costs: 50 million.

- Direct labor: 20 million.

- Manufacturing overhead: 10 million.

- Work in progress at the beginning of the period: 5 million, at the end of the period: 3 million. → Cost of goods manufactured = 5 + (50+20+10) – 3 = 82 million (for 100 tables) → Unit cost = 820,000 VND/table.

Service costing: Usually only includes labor and overhead costs (e.g., consulting services – costs are mainly expert salaries and office expenses).

6. What are the common difficulties in product costing?

In practice, product costing is not just a technical accounting problem but is also heavily influenced by operational processes and coordination between departments. Below are the common challenges businesses often face and appropriate solutions:

6.1 Difficulty in gathering and classifying costs

One of the common issues is that incurred costs are not fully recorded, or are recorded under the wrong category (confusing production costs with administrative and selling expenses). This makes the cost figures inaccurate from the very beginning.

Solution:

Businesses need to systematize input documents, build a clear accounting process for each type of cost, and use cost codes and process codes for classification. Standardization from the recording stage helps accountants easily aggregate and control incurred costs.

6.2 Complexity in allocating manufacturing overhead

Manufacturing overhead is often indirect and cannot be immediately assigned to individual products, leading to difficulties in allocation. If an inappropriate allocation basis is chosen, the product cost can be significantly distorted.

Solution:

Accountants need to choose an allocation basis that suits the production characteristics, such as machine hours, labor hours, output, or standard costs. At the same time, the effectiveness of the allocation should be periodically evaluated to make timely adjustments when the production model changes.

6.3 Inaccurate valuation of work in progress

Incorrectly determining the value of ending work in progress will distort the cost of finished goods, directly affecting the business results for the period.

Solution:

Businesses should conduct periodic physical counts of work in progress and apply a valuation method suitable for their production characteristics, such as the equivalent units method, direct material cost method, or standard cost method.

6.4 Handling spoiled and low-quality products

Spoilage during production is unavoidable; however, if not handled and accounted for correctly, the incurred costs will inflate the product cost or incorrectly reflect production efficiency.

Solution:

It is necessary to clearly classify spoilage as normal or abnormal. The cost of normal spoilage is included in the product cost, while the cost of abnormal spoilage should be accounted for separately, and the cause should be identified to implement control measures and prevent recurrence.

6.5 Lack of synchronization between accounting and production departments

Untimely or inaccurate information from the production department (output, standards, wastage) will make it difficult for accountants to calculate the actual cost of production.

Solution:

Businesses need to enhance coordination between the accounting and production departments, agreeing on data recording methods and reporting times. Using integrated management software systems (ERP, accounting-production software) will help synchronize data, reduce errors, and improve the accuracy of product costing.

6.6 Impact of Cost of Goods Sold on Profit

A low cost of goods sold helps increase the gross profit margin and improve net profit. Conversely, a high cost due to waste will reduce profit and affect competitiveness.

7. Manage, track, and calculate product costs accurately with 1Office

1Office is one of the pioneering software solutions for digital transformation in sales management for businesses in Vietnam. The CRM software provides optimal efficiency for businesses in managing revenue and expenditures in a synchronized and unified manner, helping to save time and costs in work processing.

Key features of 1Office CRM software:

- Continuously update quotes for customers.

- Automatically create new quotes based on old ones to send to customers.

- Filter by quote status to devise appropriate customer care plans.

- Professional and user-friendly interface for managing product quotes.

- Users can draft product quote contracts directly on the software with professional quote templates.

8. Frequently Asked Questions

What costs are included in the product cost?

Product cost typically includes direct material costs, direct labor costs, and manufacturing overhead. These are the 3 main cost groups that make up the cost of completing a product.

When should a business recalculate product cost?

A business should recalculate when raw material prices change, production costs increase, the production process changes, or profit margins begin to decrease. If not updated in time, the selling price can easily become unsuitable.

How does incorrect cost calculation affect profit?

Incorrect cost calculation can lead to incorrect pricing, phantom profits, or decreasing profits with increased sales. This is an error that directly affects business performance. To effectively manage quotes, revenue, and expenses in the business process, businesses can refer to 1Office’s revenue and expense management CRM software.

How do product cost and selling price differ?

Product cost is the expense to make a product, while the selling price is the level the business sets for the market to sell to customers. Simply put, product cost is the internal part, while the selling price is the external final price.

What costs are included in the product cost?

Product cost typically includes raw materials, labor, and general manufacturing overhead. Depending on the business, each cost group will be collected and allocated differently.

Our article above has provided basic information on product costing methods and how to apply them in business practice, helping to manage corporate finances effectively. It also presents a financial management solution with 1Office that helps managers thoroughly solve the problem of managing cash flow, revenue, and expenses effectively.

Contact us:

- Hotline: 083 483 8888

- Fanpage 1Office: https://www.facebook.com/1officevn

- Youtube Channel: https://www.youtube.com/c/1OfficeNềntảngquảnlýtổngthểDoanhNghiệp