What is Variable Cost? How to Calculate and Simple Examples

Variable cost is one of the fundamental concepts in corporate financial management, but not everyone understands how to calculate and apply it correctly in practice. This article will guide readers from the concept of what variable cost is, how to distinguish it from fixed cost, to the calculation formula and specific examples for easier visualization.

Mục lục

- 1. What is variable cost?

- 2. Differentiating between variable cost and fixed cost

- 3. The High-Low Method for Variable Costs

- 4. Benefits businesses gain from identifying variable costs

- 5. Factors affecting variable costs

- 6. Classification of variable costs in a business

- 7. Optimize Financial Management Efficiency in Your Business with 1Office Software

1. What is variable cost?

Variable costs are expenses that change in proportion to market conditions or are affected by the volume of goods or services a business produces. These costs increase or decrease depending on the company’s production output—they rise when production increases and fall when production decreases.

-

Example:

Some common variable costs in a business are the cost of raw materials and packaging for a manufacturing company, or credit card transaction fees for a retail company, or shipping costs, which increase or decrease with sales volume.

-

Some common types in business

-

- Direct materials

- Direct labor costs

- Transaction fees

- Product commissions

- Utility costs

2. Differentiating between variable cost and fixed cost

Follow the table below to see the differences between these two types of costs.

In business, variable costs are often referred to as the cost of goods sold, while fixed costs are not included in this category. It can be affirmed that these costs are only affected by sales and production volume if and only if factors such as sales commissions are included in the production cost per unit. Meanwhile, fixed costs are expenses that must be paid even if production slows down significantly.

In reality: In general, companies with a high proportion of variable costs are considered less volatile, as their profits are more dependent on the success of their sales.

After getting a general overview of fixed and variable costs, in the next section, we will learn how to calculate and differentiate between these two types of costs.

| Read more: 6 Product Costing Methods for Businesses [Formulas + Application] |

3. The High-Low Method for Variable Costs

After understanding the concept and classification of variable costs, businesses need to know how to determine them accurately. One of the most common and easiest methods to apply today is the High-Low method.

3.1. Definition and Purpose

The High-Low method is a technique designed to separate fixed and variable costs when a business has limited data. Typically, the costs a business incurs over a specific period are mixed costs, making it very difficult for accountants to identify and create internal reports. Therefore, the high-low method was developed to help businesses identify and allocate these two types of costs more specifically and easily.

In practice:

- The high-low method is a simple way to separate variable and fixed costs with minimal information.

- The simplicity of this method assumes that variable and fixed costs are constant, which does not reflect reality.

3.2. How the High-Low Method Works

-

How to Calculate Variable Cost Per Unit

Highest Activity Cost: The highest cost in a given period (e.g., highest monthly revenue)

Lowest Activity Cost: The lowest cost in a given period (e.g., lowest monthly revenue)

Highest Activity Unit: e.g., The highest number of products created in a month

Lowest Activity Unit: e.g., The lowest number of products created in a month

-

Formula for Calculating Variable Cost

-

Formula for Calculating Fixed Cost

A business’s fixed cost can be calculated using one of the two formulas below:

-

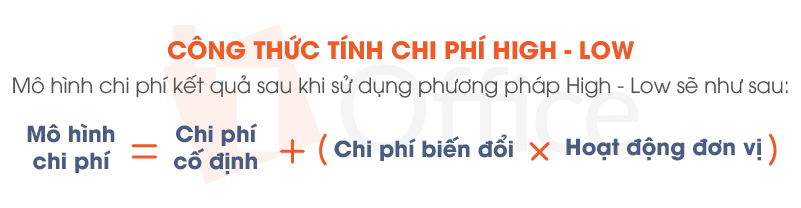

Formula for Calculating High-Low Cost

The resulting cost model after using the high-low method will be as follows:

Above, we have provided the formulas to calculate and determine the two common types of costs in a business. In the next section, we will look at a practical example to better understand this method.

| Learn more: The process of building a sales plan and common issues |

3.3. Example of Using the High-Low Method for Cost Calculation

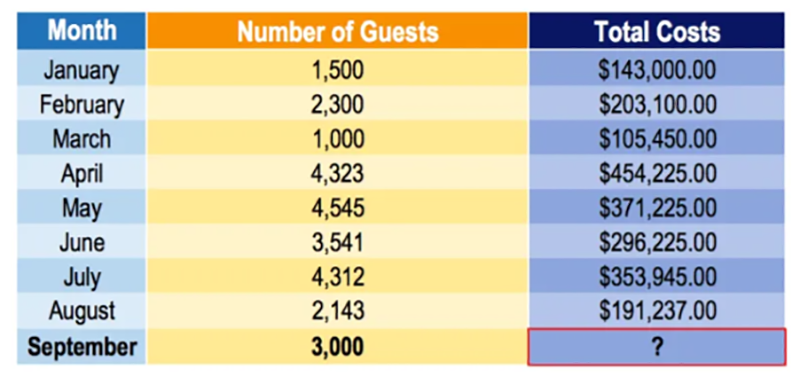

A hotel manager wants to develop a cost model to predict the hotel’s future operating costs. Unfortunately, the only available data is the number of guests in a given month and the total costs incurred each month. Your task is to clearly identify the Fixed Costs and Variable Costs based on only these two metrics.

He predicts the number of guests in September will be 3,000. Using the dataset below, develop a cost model and predict the costs that will be incurred in September.

Note: It is important to select the high-low values from the units (i.e., number of guests) and not the total costs. The number of units drives the total costs.

The highest total cost is $454,255, corresponding to 4,323 guests. However, the correct high-low values are from the independent variable (the cost driver). In this case, the high and low levels would be 4,545 guests in May with a total cost of $371,225 and 1,500 guests in January with a total cost of $143,000.

- We have the formula for calculating the variable cost per guest unit:

- Now we can determine our fixed costs:

Using the high activity level:

Fixed Cost = $371,225 – ($74.97 x 4,545) = $30,486.35

Using the low activity level:

Fixed Cost = $105,450 – ($74.97 x 1,000) = $30,480

The difference between the two fixed cost calculations is negligible.

| Learn more: What is an Internal Report? The Best Standard Templates for 2022 |

4. Benefits businesses gain from identifying variable costs

Once variable costs are clearly identified, a business will see their impact on operational efficiency. Here are the specific benefits that managing and analyzing variable costs can bring.

4.1. Measuring variable cost trends and their impact on business Revenue and Profit

In most cases, increasing production volume makes the cost per unit more favorable. This is because fixed costs are spread over a larger number of product units.

For example: If a business that produces 500,000 products per year spends $50,000 per year on rent, the rent cost allocated to each unit is $0.10 per product. If production doubles, the rent is now allocated at only $0.05 per unit, leaving more profit on each sale.

Therefore, as revenue increases, the cost of goods sold will also increase, but at a slower rate (because the variable cost per unit remains constant and the fixed cost per unit decreases).

4.2. Risk assessment

By comparing the percentage of variable costs to fixed costs for a product unit, you can determine the weight of each cost type. As an outside investor, you can use this information to predict potential profit risks.

If a company primarily incurs variable costs in production, it may have a more stable cost per unit. This will lead to a more stable profit stream, assuming sales are steady. This is true for large retailers like Walmart and Costco. Their fixed costs are relatively low compared to their variable costs, which account for a large proportion of the cost associated with each sale.

During periods of declining sales, a company that relies mainly on variable costs can more easily scale down production and maintain profitability, whereas a company with predominantly fixed costs will have to find ways to deal with much higher fixed costs.

| Learn more: What is Financial Risk? Prevention and Management Solutions |

4.3. Comparison with competitors in the market

To compare with competitors in the market, you can calculate the variable cost per unit and the total variable cost for a specific company. Then, find data on the average cost for that company’s industry. Doing so will provide you with a benchmark to evaluate the first company.

- A higher variable cost per unit may indicate that a company is less efficient than others.

- A lower variable cost per unit may represent a competitive advantage.

- A higher-than-average cost per unit suggests that a company uses a larger quantity of or spends more on resources (labor, raw materials, utilities) to produce goods compared to its competitors.

5. Factors affecting variable costs

Variable costs are not fixed; they constantly change with production volume, raw material prices, labor productivity, and market conditions. To effectively control this expense, businesses need to clearly understand the main influencing factors:

5.1 Fluctuations in raw material prices

The price of input raw materials is a factor that directly affects variable costs. When the prices of steel, gasoline, packaging, or raw materials increase, the production cost per product also increases accordingly.

For example, a beverage factory will be significantly affected if the price of sugar or bottle shells rises sharply, increasing the cost per unit.

5.2 Labor productivity and efficiency

Direct labor for production is a variable cost that changes with output. If labor productivity decreases due to a lack of skills or outdated equipment, the labor cost per product will increase. Conversely, when a business applies automation technology or improves processes, increased productivity helps reduce the average variable cost.

5.3 Commission and sales bonus policies

For commercial or service businesses, commission and bonus costs are often calculated as a percentage of revenue. When sales increase, this cost also increases. This is a type of variable cost that depends on actual business performance.

5.4 Seasonal operating costs

Many industries such as tourism, retail, or seasonal foods often have significant cost fluctuations at different times. During peak season, businesses may have to spend more on temporary labor, transportation, warehousing, or advertising, which increases total variable costs.

5.5 Changes in production scale or market demand

When expanding the scale of production, the variable cost per unit may decrease due to economies of scale. However, when market demand decreases, this cost tends to increase due to lower output, leading to a higher allocated cost per unit.

Tracking and analyzing these factors helps businesses predict cost trends and adjust production, pricing, and profit plans more flexibly and proactively.

6. Classification of variable costs in a business

Variable costs are not just production materials but also include many different items depending on the specific operations of the business. Variable costs can be divided into three main groups:

6.1 Variable costs by production volume

These are costs that change in direct proportion to the number of products produced. Includes:

-

Direct raw materials such as wood, fabric, plastic, metal.

-

Direct labor involved in production.

-

Energy, electricity, water, fuel used in the production line.

For example: when a garment factory produces an additional 1,000 shirts, the amount of fabric and thread also increases accordingly.

6.2 Variable costs by sales volume

Occur mainly in commercial and service businesses. These are costs that change with revenue or the number of products sold, including:

-

Commissions and bonuses for sales staff.

-

Trade discounts for agents.

-

Shipping and delivery fees.

-

Performance-based advertising budgets, e-commerce platform fees.

For example: when revenue doubles, the total commission cost also doubles.

6.3 Mixed Variable Costs

These are costs that have both a fixed component and a variable component based on usage.

For example: electricity bills have a fixed monthly minimum fee, with the remainder changing based on consumption.

Another example is warehouse rental costs – the business pays a basic fixed fee and incurs additional costs if the allowed storage capacity is exceeded.

Classifying variable costs helps businesses establish a detailed accounting system, making it easy to track and control cost fluctuations, thereby optimizing production plans, selling prices, and profits for each period.

7. Optimize Financial Management Efficiency in Your Business with 1Office Software

With the all-in-one business management software 1Office in general, and the CRM module in particular, you will no longer need to create reports in Excel. Instead, you can generate financial management reports directly on the software, simplifying procedures and making the process easier.

<iframe title="

Some report templates that will be automatically generated on the 1Office system include:

- HR reports

- Work/project progress reports

- Internal reports

- Business administration reports

- Sales reports

- …

Additionally, using the 1Office CRM module will help your business operate more simply and smoothly than ever because:

- Standardize all business processes

- Easier monitoring of implementation progress

- Be more proactive in your work

- Revenues and expenditures are stored on the system for easy consolidation

- Customer information and data are available 24/7

Through the article above, we hope that the information 1Office has provided is valuable to our readers. If you have any further questions that need answering, please contact us for a free consultation.

- Hotline: 083 483 8888

- Fanpage: https://www.facebook.com/1officevn/

- Youtube: https://www.youtube.com/channel/UCeTIRNqxaTwk0_kcTw6SxmA